In the face of financial distress, homeowners in Texas may find themselves navigating the challenging waters of foreclosure. Understanding the Texas Deed in Lieu of Foreclosure can be a crucial tool in this difficult situation. This legal document offers a potential lifeline, allowing homeowners to voluntarily transfer their property back to the lender as a means of satisfying the mortgage debt. Instead of enduring the lengthy and stressful foreclosure process, this option can often be faster and less damaging to one's credit. By executing this deed, the borrower seeks to avoid the public stigma of foreclosure, often enabling a smoother transition to alternative housing solutions. However, it’s essential for homeowners to grasp the terms, conditions, and potential consequences that come with choosing this path. The form typically includes vital information such as the names of the parties involved, property description, and information about existing liens. As homeowners weigh their options, understanding the nuances of this document becomes imperative for making informed decisions that affect their financial recovery and future stability.

Texas Deed in Lieu of Foreclosure Template

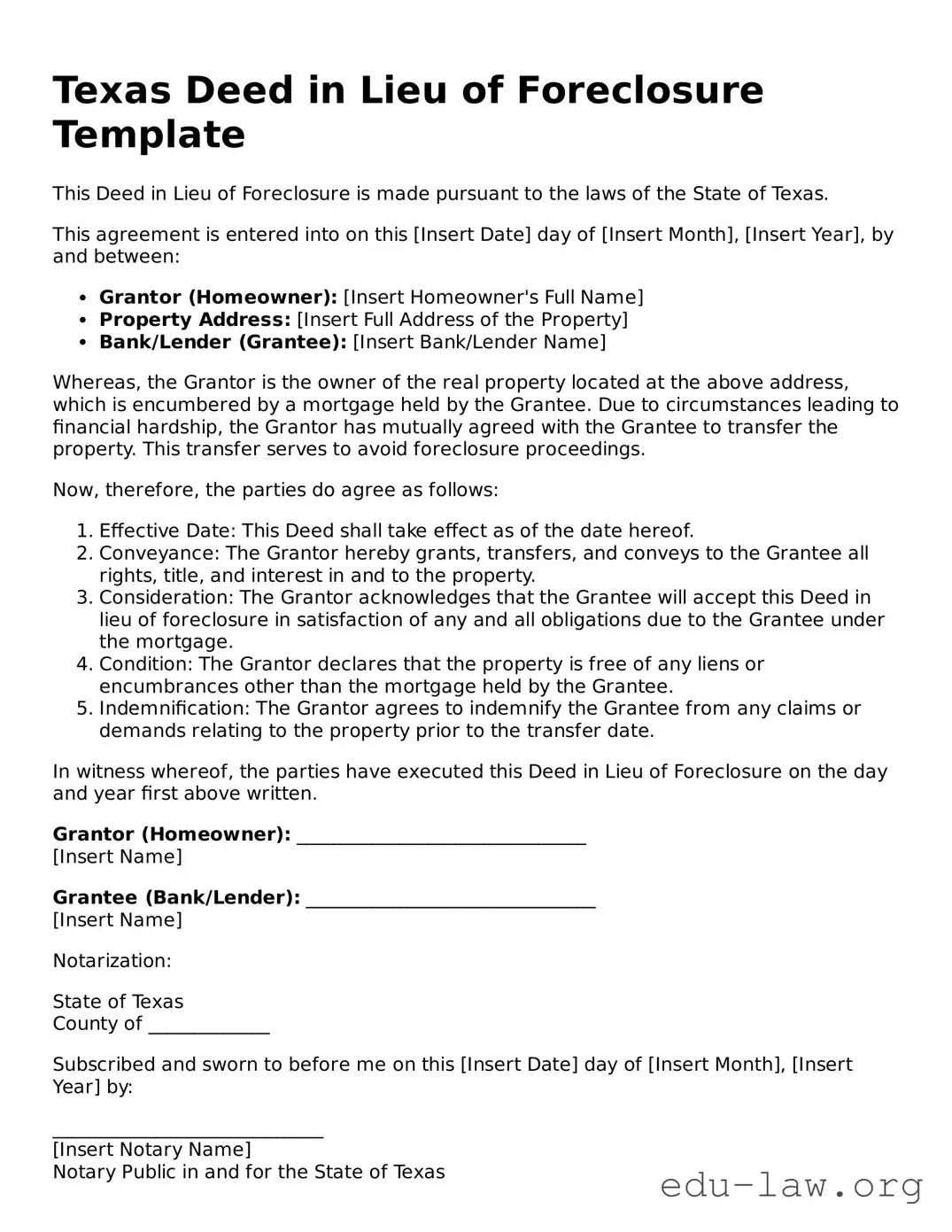

This Deed in Lieu of Foreclosure is made pursuant to the laws of the State of Texas.

This agreement is entered into on this [Insert Date] day of [Insert Month], [Insert Year], by and between:

Whereas, the Grantor is the owner of the real property located at the above address, which is encumbered by a mortgage held by the Grantee. Due to circumstances leading to financial hardship, the Grantor has mutually agreed with the Grantee to transfer the property. This transfer serves to avoid foreclosure proceedings.

Now, therefore, the parties do agree as follows:

In witness whereof, the parties have executed this Deed in Lieu of Foreclosure on the day and year first above written.

Grantor (Homeowner): _______________________________

[Insert Name]

Grantee (Bank/Lender): _______________________________

[Insert Name]

Notarization:

State of Texas

County of _____________

Subscribed and sworn to before me on this [Insert Date] day of [Insert Month], [Insert Year] by:

_____________________________

[Insert Notary Name]

Notary Public in and for the State of Texas

| Fact Name | Description |

|---|---|

| Definition | A Deed in Lieu of Foreclosure is a legal document where a borrower voluntarily transfers their property title to the lender to avoid foreclosure proceedings. |

| Purpose | The primary purpose is to provide a more amicable resolution for both parties, allowing the borrower to avoid the negative impacts of foreclosure. |

| State Law | Texas law governing deeds includes Texas Property Code Section 12.001, which outlines the requirements for property transfers. |

| Eligibility | Typically, only borrowers facing financial hardship and willing to relinquish their property ownership qualify for this option. |

| Benefits | Benefits for the borrower include the potential for less damage to their credit score compared to a foreclosure, as well as a quicker resolution. |

| Considerations | Borrowers should consider the tax implications and the potential deficiency judgments that may arise from the transaction. |

Completing the Texas Deed in Lieu of Foreclosure form is an important step for homeowners facing foreclosure. After filling out this form, your mortgage lender will review it to move forward with the next steps. Following this process can be both relieving and complex, and understanding what to do can help ease some of the stress.

Once your lender receives the completed form, they will process your request. You may then discuss any further steps or implications of this action. Staying in communication with your lender and possibly seeking professional advice can be beneficial during this time.

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal agreement between a borrower and a lender. Under this arrangement, the borrower voluntarily transfers the title of the property to the lender in order to avoid foreclosure. This option often becomes appealing when a homeowner is struggling to make mortgage payments and wishes to take proactive steps to resolve the situation. By transferring ownership, the borrower can settle their mortgage debt and potentially mitigate any further financial damage, such as a long-lasting negative impact on their credit score.

What are the benefits of using a Deed in Lieu of Foreclosure?

There are several benefits associated with a Deed in Lieu of Foreclosure. For one, it tends to be a faster process than a traditional foreclosure, allowing homeowners to move on more quickly. Additionally, this arrangement can minimize the emotional stress that often accompanies foreclosure proceedings. Homeowners may also find that it offers a greater level of dignity compared to losing a home through foreclosure. Importantly, if the lender agrees, borrowers might be relieved from some or all remaining mortgage debts, which can help them start fresh financially.

Are there any risks involved with a Deed in Lieu of Foreclosure?

Yes, there are risks that homeowners should consider. First and foremost, the lender's acceptance of the Deed in Lieu is not guaranteed; they must evaluate the property and the borrower’s overall financial situation. Also, some lenders may still hold the borrower responsible for any deficiencies—this occurs if the property’s market value is lower than the outstanding mortgage amount. It’s essential to understand whether the agreement includes any clauses regarding potential deficiency judgments. Furthermore, before proceeding, borrowers should consult with a financial advisor or attorney to completely understand their rights and any tax implications that may arise from transferring ownership of the property.

How does one initiate a Deed in Lieu of Foreclosure process in Texas?

Initiating a Deed in Lieu of Foreclosure process typically begins with reaching out to the lender. Homeowners should explain their situation and express their desire to avoid foreclosure. The lender will then assess whether this option is appropriate based on the homeowner’s circumstances and the value of the property. Once both parties agree, the next steps often involve preparing the Deed in Lieu document and related paperwork. It is crucial for homeowners to review these documents carefully, possibly with the help of a legal professional, to ensure that all terms and conditions are understood and acceptable. After signing, the deed should be recorded with the county to finalize the transfer of ownership, officially releasing the homeowner from the mortgage obligation.

Not Understanding the Process: Many individuals fail to fully grasp the implications of signing a deed in lieu of foreclosure. This mistake can lead to unexpected consequences, such as remaining liable for any deficiencies in the mortgage balance.

Incorrect Property Description: Providing an inaccurate or incomplete description of the property can create legal issues. It is important to ensure that the property details match what is recorded in public records.

Failure to Obtain Necessary Signatures: If all parties involved do not properly sign the document, it may not be legally binding. This includes obtaining signatures from any co-owners or spouses, if applicable.

Not Consulting a Professional: Skipping the advice of a real estate attorney or financial advisor can lead to mistakes. Professional guidance might help in understanding the full consequences and benefits of this action.

Ignoring Required Notices: Some individuals overlook the importance of providing required notices to the lender before signing the deed in lieu. This could affect the lender’s willingness to accept the deed.

Not Keeping Copies: After signing the deed in lieu, failing to keep copies of the document for personal records is a common mistake. It is vital to have documentation for future reference and any potential disputes.

When dealing with real estate matters, particularly in situations involving foreclosure, several documents may be needed alongside the Texas Deed in Lieu of Foreclosure form. Understanding these forms can help streamline the process and ensure all parties are properly informed and protected. Below is a list of commonly associated documents.

Utilizing these documents in conjunction with the Texas Deed in Lieu of Foreclosure form can create a smoother transition for both lenders and borrowers during difficult times. Each form serves a distinct purpose, helping ensure that the transaction is clear, fair, and legally binding.

The Texas Warranty Deed is similar to the Deed in Lieu of Foreclosure because both documents facilitate the transfer of property. A Warranty Deed provides a guarantee from the seller that they hold clear title to the property and can legally sell it. In essence, while a Deed in Lieu of Foreclosure transfers ownership to the lender to avoid foreclosure, a Warranty Deed assures the buyer that they will receive full rights to the property without any hidden claims against it.

The Quitclaim Deed also bears similarities to the Deed in Lieu of Foreclosure. With a Quitclaim Deed, a person transfers their interest in a property without making any warranties about the title. This type of deed is often used to resolve disputes or transfer property among family members. Like the Deed in Lieu of Foreclosure, it does not guarantee a clear title, making it a less formal method of conveying property rights.

Another similar document is the Deed of Trust. This document serves a different purpose, as it is used to secure a loan with real property. However, both documents involve the transfer of interest in real estate. When a borrower relinquishes property through a Deed in Lieu of Foreclosure, it is often a response to the difficulties presented by a mortgage secured by a Deed of Trust.

The Foreclosure Sale Deed represents a completion of the foreclosure process, transferring property ownership to the buyer at auction. While this document results from a forced sale and is typically less favorable for the borrower, it ultimately achieves the goal of transferring property. Both this deed and the Deed in Lieu of Foreclosure finalize the process of dealing with mortgage default, though they occur under different circumstances.

In addition, the Grant Deed enables property owners to transfer their title while implying some degree of warranty. This document ensures that the seller has not transferred the title to anyone else and that the property is free from undisclosed encumbrances. Similar to a Deed in Lieu of Foreclosure, it serves the need for a straightforward transfer of ownership while lending some level of assurance to the buyer.

Lastly, the Land Contract is relevant as a means of property transfer that does not change title until certain conditions are met, typically the payment of the agreed purchase price. While it operates differently, both documents address scenarios where ownership is effectively transferred or resolved without the typical processes of a sale. A Deed in Lieu of Foreclosure simplifies the situation for a distressed homeowner, while a Land Contract offers flexibility for buyers and sellers that may not involve immediate full ownership transfer.

Filling out the Texas Deed in Lieu of Foreclosure form requires careful attention to detail. Here’s a guide on what to do and what to avoid:

Misconception 1: A Deed in Lieu of Foreclosure is the same as a foreclosure.

This is not true. While both processes involve the transfer of property, a deed in lieu is a voluntary agreement where the homeowner willingly transfers the property to the lender to avoid the lengthy foreclosure process.

Misconception 2: Signing a Deed in Lieu means you are absolved of all debt immediately.

Actually, this depends on the terms of the agreement. It’s important to negotiate whether the lender will forgive any remaining mortgage debt after the deed is transferred.

Misconception 3: A Deed in Lieu of Foreclosure has no impact on credit scores.

This is misleading. While it may affect your credit score less severely than a foreclosure, it will still be viewed negatively and could impact your ability to secure future loans.

Misconception 4: Only a lender can initiate a Deed in Lieu of Foreclosure.

In reality, homeowners can also initiate the process. A homeowner can reach out to their lender to discuss this option as a way to avoid foreclosure and find a solution for their financial situation.

When considering the Texas Deed in Lieu of Foreclosure form, it is essential to understand its implications and requirements. Here are ten key takeaways to keep in mind:

Understanding these points can ease the transition and improve outcomes for those considering a deed in lieu in Texas.

California Pre-foreclosure Property Transfer - Knowing the potential consequences can help borrowers make informed decisions about this option.

Georgia Foreclosure Laws - Legal counsel can help navigate the various implications of a Deed in Lieu of Foreclosure.

Deed in Lieu of Foreclosure Template - This form can facilitate a fresh start for those who have faced challenging financial circumstances.