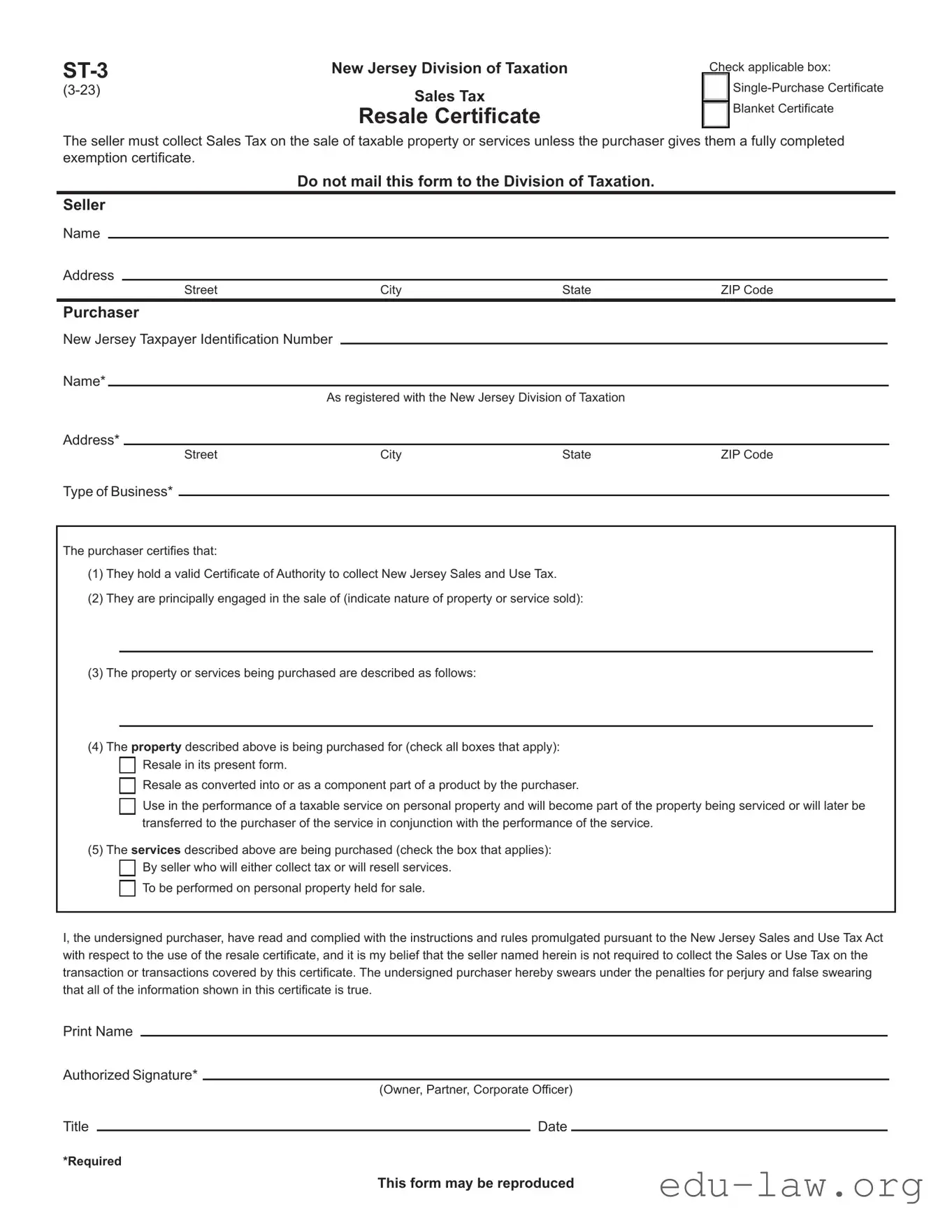

The ST-3 form, also known as the New Jersey Resale Certificate, plays a crucial role in the state's sales tax system. This form allows sellers to collect sales tax on transactions involving taxable property or services unless the buyer presents a properly completed exemption certificate. To utilize the ST-3 form, purchasers must provide their New Jersey Taxpayer Registration Number, along with details about their business and the nature of the merchandise or services being purchased. The form requires the purchaser to certify that they hold a valid Certificate of Authority and are engaged in the sale of specified goods or services. Additionally, it outlines the conditions under which the purchased items are intended for resale or use in taxable services. Sellers must retain this certificate for at least four years and ensure it is available for inspection. The ST-3 form not only serves as a legal document for tax exemption but also protects sellers from liability regarding the collection and payment of sales tax, provided they follow the guidelines set forth by the New Jersey Division of Taxation. Understanding the proper use of this form is essential for both buyers and sellers to navigate sales tax obligations effectively.

New Jersey Division of Taxation |

|

Sales Tax |

|

|

Resale Certificate |

Check applicable box:

Blanket Certificate

The seller must collect Sales Tax on the sale of taxable property or services unless the purchaser gives them a fully completed exemption certificate.

Do not mail this form to the Division of Taxation.

Seller

Name

Address

Street |

City |

State |

ZIP Code |

Purchaser

New Jersey Taxpayer Identification Number

Name*

As registered with the New Jersey Division of Taxation

Address*

Street |

City |

State |

ZIP Code |

Type of Business*

The purchaser certifies that:

(1)They hold a valid Certificate of Authority to collect New Jersey Sales and Use Tax.

(2)They are principally engaged in the sale of (indicate nature of property or service sold):

(3)The property or services being purchased are described as follows:

(4)The property described above is being purchased for (check all boxes that apply):

Resale in its present form.

Resale as converted into or as a component part of a product by the purchaser.

Use in the performance of a taxable service on personal property and will become part of the property being serviced or will later be transferred to the purchaser of the service in conjunction with the performance of the service.

(5)The services described above are being purchased (check the box that applies):

By seller who will either collect tax or will resell services.

To be performed on personal property held for sale.

I, the undersigned purchaser, have read and complied with the instructions and rules promulgated pursuant to the New Jersey Sales and Use Tax Act with respect to the use of the resale certificate, and it is my belief that the seller named herein is not required to collect the Sales or Use Tax on the transaction or transactions covered by this certificate. The undersigned purchaser hereby swears under the penalties for perjury and false swearing that all of the information shown in this certificate is true.

Print Name

Authorized Signature*

(Owner, Partner, Corporate Officer)

Title |

|

Date |

*Required

This form may be reproduced

Form

Completing the Certificate

To claim an exemption from Sales Tax on the purchase of taxable property or services, the purchaser must provide a fully completed exemption cer- tificate to the seller. Otherwise, the seller must collect the tax. The purchaser must provide the following information for the exemption certificate to be considered fully completed:

•• Name and address;

•• New Jersey taxpayer identification number;

•• Type of business;

•• Reason(s) for exemption;

•• Signature, if using a paper exemption certificate (including fax).

The seller’s name and address are not required for the exemption certificate to be considered fully completed.

Accepting the Certificate

A seller must be registered to accept an exemption certificate. The seller is relieved of liability for collecting Sales Tax on transaction(s) covered by the certificate as long as the certificate is fully completed and is received within 90 days of the date of sale. The seller is relieved of liability even if the pur- chaser improperly claimed the exemption, in which case the purchaser will be held liable for nonpayment of the tax.

Accepting the Certificate in an Audit Situation

If the seller either has not obtained an exemption certificate or has obtained an incomplete exemption certificate, the seller has at least 120 days after the Division’s request for substantiation of the claimed exemption to either:

1.Obtain a fully completed exemption certificate from the purchaser taken in good faith, which in an audit situation means the exemption:

•• Was statutorily available on the date of the transaction(s); and

•• Could apply to the property or service being purchased; and

•• Is reasonable for the purchaser’s type of business; or

2.Obtain other information establishing that the transaction(s) was not subject to tax.

If the seller obtains this information, the seller is relieved of any liability for the tax on the transaction unless it is discovered through the audit process that the seller had knowledge or had reason to know at the time the information was provided that the information relating to the exemption claimed was materially false or the seller otherwise knowingly participated in activity intended to purposefully evade the tax that is properly due on the transaction. The burden is on the Division to establish that the seller had knowledge or had reason to know at the time the information was provided that the informa- tion was materially false.

Blanket Certificates

A single exemption certificate may cover additional purchases of the same general type of property by the same purchaser with which the seller has a recurring business relationship. For purposes of this section, a recurring business relationship exists when a period of no more than 12 months elapses between sales transactions.

To use this form as a blanket certificate, check the applicable box at the top of the form. Each subsequent sales slip or purchase invoice based on the blanket certificate must be clearly marked with the purchaser’s name, address, and identification number.

Retention of Certificates

Certificates must be retained by the seller for four years from the date of the last sale covered by the certificate. Certificates must be in the physical possession of the seller and available for inspection. A seller that enters data elements from paper into an electronic format is not required to retain the paper exemption certificate.

Examples

Proper Use of Form

1.A retail appliance store owner issues a resale certificate when purchasing appliances from a supplier for resale.

2.A furniture manufacturer issues a resale certificate when purchasing lumber to be used in manufacturing furniture for sale.

3.A service station operator issues a resale certificate when purchasing auto parts to be used in repairing customers’ cars.

Improper Use of Form

In the examples below, the seller cannot accept a resale certificate and must collect Sales Tax.

1.A lumber dealer cannot accept a resale certificate from a tire dealer that is purchasing lumber for use in altering its premises.

2.A distributor cannot issue a resale certificate on purchases of cleaning supplies and other materials for its own office maintenance, even though it is in the business of distributing such supplies.

3.A retailer cannot issue a resale certificate on purchases of office equipment for its own use, even though it is in the business of selling office equipment.

4.A supplier cannot accept a resale certificate from a service station that purchases tools and testing equipment for use in its business.

5.A contractor cannot issue Form

For more information, see

| Fact Name | Description |

|---|---|

| Purpose | The ST-3 form serves as a Resale Certificate, allowing sellers to avoid collecting sales tax on certain transactions. |

| Seller's Responsibility | Sellers must collect sales tax unless they receive a fully completed ST-3 form from the purchaser. |

| Certificate of Authority | The purchaser must hold a valid Certificate of Authority to collect New Jersey Sales and Use Tax. |

| Retention Period | Sellers must retain the completed ST-3 form for a minimum of four years from the last sale date covered by the certificate. |

| Additional Purchases | The ST-3 form can cover additional purchases of the same type of property by the same purchaser, provided details are included on each invoice. |

| Improper Use Examples | Examples of improper use include using the ST-3 form for personal purchases or for items not intended for resale. |

| Governing Law | The ST-3 form is governed by the New Jersey Sales and Use Tax Act. |

Completing the ST-3 form is essential for ensuring that sales tax is properly handled in New Jersey transactions. The form acts as a resale certificate, allowing purchasers to claim an exemption from sales tax on qualifying purchases. Here’s a straightforward guide to filling out the form correctly.

Once completed, the ST-3 form should be given to the seller and retained for your records. This will help ensure compliance with New Jersey sales tax regulations and protect both parties in the transaction.

What is the purpose of the ST-3 New Jersey form?

The ST-3 form serves as a resale certificate that allows sellers to exempt certain sales from sales tax. When a purchaser provides a fully completed ST-3 form to the seller, it certifies that the items being purchased are intended for resale or for use in taxable services. This form is essential for ensuring compliance with New Jersey's sales tax regulations.

Who is required to complete the ST-3 form?

The purchaser is responsible for completing the ST-3 form. This includes providing necessary details such as their New Jersey Taxpayer Registration Number, type of business, and a description of the merchandise or services being purchased. The seller must retain this form to validate the exemption from sales tax.

What information must be included on the ST-3 form?

The ST-3 form requires several key pieces of information. This includes the purchaser's name and address, type of business, reason for the exemption, and the New Jersey tax identification number. If the purchaser is not registered in New Jersey, they should provide their Federal employer identification number or out-of-state registration number. Additionally, the form must be signed by the purchaser or an authorized representative.

How long must sellers retain the ST-3 form?

Sellers are required to retain the ST-3 form for a minimum of four years from the date of the last sale covered by the certificate. This retention is crucial for compliance and to provide documentation in case of an audit by the New Jersey Division of Taxation.

What happens if a purchaser improperly claims an exemption?

If it is determined that a purchaser improperly claimed an exemption using the ST-3 form, the purchaser will be held liable for the nonpayment of the tax. Sellers are relieved of liability as long as they have accepted a fully completed exemption certificate in good faith.

Can the ST-3 form be used for multiple purchases?

Yes, the ST-3 form can cover additional purchases by the same purchaser for the same general type of property. However, each subsequent sales slip or purchase invoice must still show the purchaser's name, address, and registration number for verification purposes.

Are there examples of proper and improper use of the ST-3 form?

Yes, proper use includes scenarios where a retail store purchases items for resale or a manufacturer buys materials to create products for sale. Conversely, improper use occurs when a business attempts to use the ST-3 form for items intended for personal use or for business maintenance, such as office supplies or equipment.

How can sellers ensure they are compliant when accepting the ST-3 form?

Sellers should ensure that the ST-3 form is fully completed and signed by the purchaser. They must also familiarize themselves with the guidelines provided by the New Jersey Division of Taxation regarding the acceptance of exemption certificates. Regular training and updates on sales tax regulations can further support compliance.

Where can I find more information about the ST-3 form?

For additional information, you can refer to publication S&U-6 (Sales Tax Exemption Administration) available on the New Jersey Division of Taxation's website. This publication provides comprehensive guidance on sales tax exemptions and the proper use of resale certificates.

Incomplete Information: Failing to provide all required details, such as the purchaser's name, address, and New Jersey tax identification number, can render the form invalid.

Incorrect Tax Identification Number: Using an incorrect or invalid New Jersey Taxpayer Registration Number can lead to complications during audits.

Missing Signature: Not signing the form can result in the seller being unable to accept the exemption certificate.

Improper Use of the Certificate: Using the certificate for items or services that do not qualify for resale can lead to tax liabilities.

Failure to Check Applicable Boxes: Not indicating the correct boxes for the type of purchase can create confusion and invalidate the certificate.

Not Retaining the Certificate: Sellers must keep the certificate for at least four years. Failing to do so can expose them to tax liabilities.

Ignoring Instructions: Not reading or following the instructions on the form can lead to mistakes that may affect tax exemption eligibility.

The ST-3 New Jersey form is an essential document for sellers and purchasers involved in taxable property or services. It serves as a resale certificate, allowing sellers to avoid collecting sales tax when a purchaser certifies their intent to resell the items. However, several other forms and documents are often used in conjunction with the ST-3 to ensure compliance with New Jersey tax regulations. Below is a list of these related documents.

Each of these forms plays a vital role in the sales tax process within New Jersey. They help ensure that both sellers and purchasers understand their responsibilities and rights under the law. Proper use and retention of these documents can prevent potential tax liabilities and ensure compliance with state regulations.

The ST-4 form in New Jersey serves as a Sales Tax Exempt Certificate, similar to the ST-3 Resale Certificate. Both documents allow purchasers to claim an exemption from sales tax when acquiring goods or services. The ST-4 is typically used by organizations that qualify for tax-exempt status, such as nonprofit entities or government agencies. Just like the ST-3, the ST-4 requires the purchaser to provide their tax identification number and details about the nature of the purchase. Both forms must be retained by the seller for record-keeping purposes to demonstrate compliance during audits.

The ST-5 form is another exemption certificate that applies to sales of tangible personal property and services in New Jersey. This form is used specifically for purchases by certain exempt organizations. Like the ST-3, the ST-5 requires the purchaser to declare their tax-exempt status and provide relevant identification numbers. Sellers must keep this form on file to validate the tax-exempt status of the transaction, ensuring they are not liable for uncollected sales tax.

The ST-6 form is the New Jersey Sales Tax Exempt Use Certificate. This document is utilized when a purchaser intends to use the item in a manner that does not require sales tax. Similar to the ST-3, the ST-6 necessitates the purchaser to provide their tax identification number and a description of the intended use. Both forms relieve the seller from the obligation to collect sales tax, provided the forms are properly completed and retained.

The ST-7 form is the New Jersey Exempt Use Certificate for manufacturing and industrial use. This document allows manufacturers to purchase materials tax-free when they will be incorporated into a product for resale. Like the ST-3, the ST-7 requires specific information about the purchaser and the nature of the purchase. Sellers must retain this certificate to avoid liability for sales tax on exempt transactions.

The ST-8 form is designated for purchases made by certain exempt entities, including educational institutions. This certificate functions similarly to the ST-3 in that it allows qualifying organizations to make tax-exempt purchases. The ST-8 requires the purchaser to provide their tax identification number and details about the items being purchased, ensuring that sellers can validate the exemption during audits.

The ST-9 form is a New Jersey Certificate of Exempt Sale for sales of property or services that are exempt from tax. This form is akin to the ST-3 as it allows sellers to accept tax-exempt transactions from eligible buyers. The ST-9 requires the purchaser to provide necessary identification and details about the transaction, similar to the requirements of the ST-3. Retaining this form is crucial for sellers to demonstrate compliance with tax regulations.

The ST-10 form serves as the New Jersey Exempt Purchaser Certificate, which is used for specific types of exempt purchases. Like the ST-3, this form allows eligible buyers to make tax-free purchases by certifying their exempt status. The information required is comparable to that of the ST-3, including the purchaser’s tax identification number and a description of the items being purchased. Sellers must keep this certificate on file to substantiate the exemption during any potential audits.

The ST-11 form is used for sales to certain governmental entities and is similar to the ST-3 in that it allows for tax-exempt purchases. This form requires the buyer to provide their governmental identification and details about the purchase. Just like the ST-3, the ST-11 protects the seller from liability for uncollected sales tax, provided the form is properly completed and retained. This ensures compliance with tax laws while facilitating transactions with government entities.

When filling out the ST-3 New Jersey form, it is essential to follow specific guidelines to ensure compliance with state tax regulations. Here are six important dos and don'ts:

Understanding the nuances of the ST-3 New Jersey form is crucial for both buyers and sellers engaged in taxable transactions. Unfortunately, several misconceptions persist regarding this resale certificate. Below is a list of common misunderstandings along with clarifications to help navigate the complexities of this form.

Awareness of these misconceptions is essential for compliance and to avoid potential penalties. Both buyers and sellers should take the time to understand the requirements and implications of using the ST-3 form in New Jersey.

Filling out and using the ST-3 New Jersey form, also known as the Resale Certificate, is essential for ensuring compliance with state sales tax regulations. Here are some key takeaways to consider:

Understanding these key points can help both buyers and sellers navigate the sales tax exemption process effectively.