The Profit and Loss form serves as a crucial financial document for businesses, providing a comprehensive overview of income and expenses over a specific period. It enables stakeholders to assess the company's profitability by detailing revenue streams, cost of goods sold, and operational expenses. By analyzing this form, one can identify trends in financial performance, evaluate operational efficiency, and make informed decisions regarding budgeting and resource allocation. Key components of the Profit and Loss form include gross profit, which is derived from subtracting the cost of goods sold from total revenue, and net profit, which accounts for all expenses, taxes, and interest. Additionally, this form often includes comparisons to previous periods, allowing for a clearer understanding of growth or decline. Ultimately, the Profit and Loss form is not merely a record of financial activity; it is an essential tool for strategic planning and financial analysis.

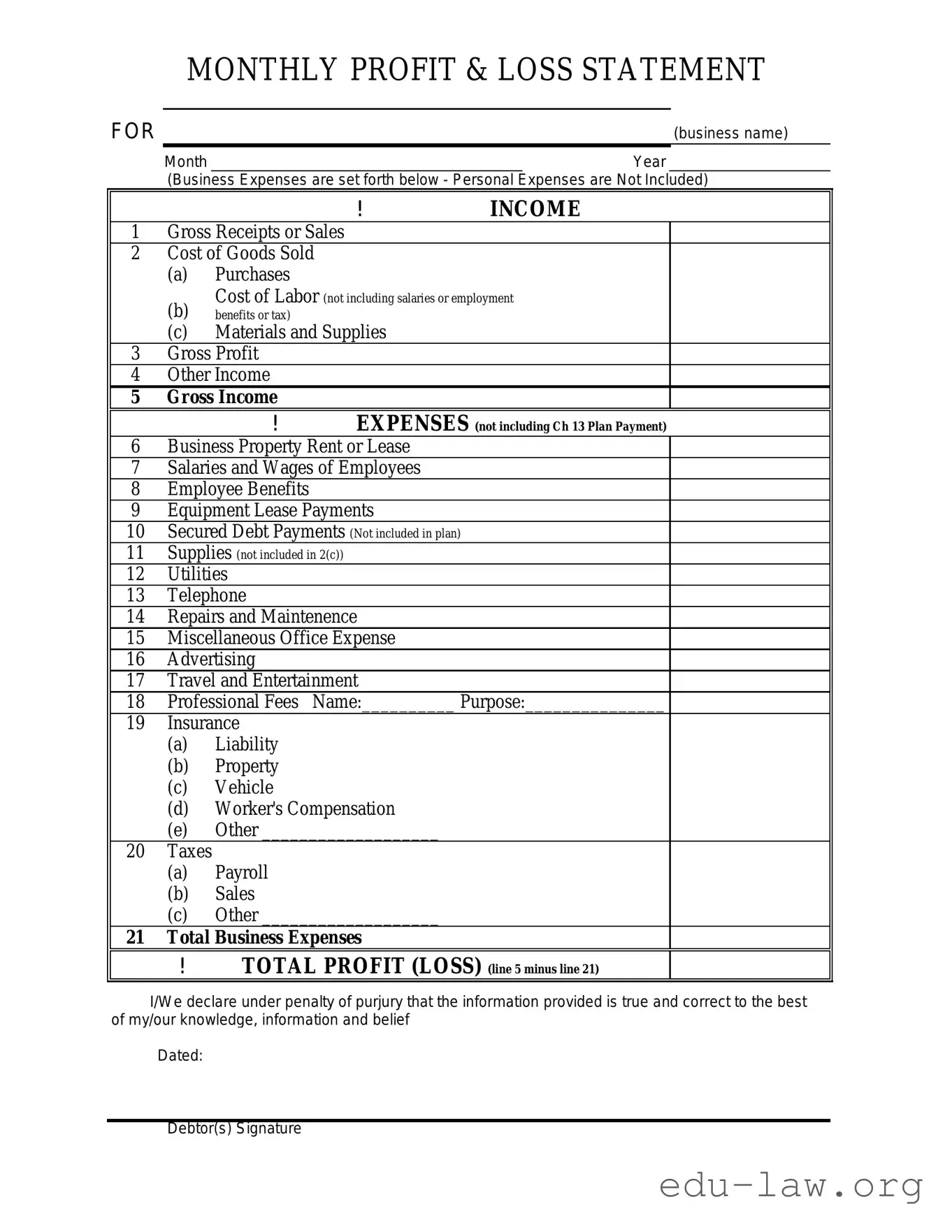

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Name | Description |

|---|---|

| Purpose | The Profit and Loss form is used to summarize income and expenses over a specific period, helping to determine net profit or loss. |

| Components | This form typically includes sections for revenue, cost of goods sold, operating expenses, and other income or expenses. |

| Frequency | Businesses often complete this form monthly, quarterly, or annually, depending on their reporting needs. |

| Tax Implications | Profit and Loss statements are crucial for tax reporting, as they provide necessary information for income tax calculations. |

| State-Specific Forms | Some states require specific formats for the Profit and Loss form. For example, California adheres to the California Revenue and Taxation Code. |

| Analysis Tool | Businesses use the Profit and Loss form to analyze financial performance, identify trends, and make informed decisions. |

| Record Keeping | Maintaining accurate Profit and Loss statements is essential for effective financial management and compliance with regulations. |

| Format | The form can be presented in various formats, including spreadsheets, accounting software, or printed documents. |

After gathering all necessary financial information, you are ready to fill out the Profit and Loss form. This document will help you summarize your income and expenses over a specific period. Follow the steps below to ensure accurate completion of the form.

What is a Profit and Loss form?

A Profit and Loss form, often referred to as an income statement, summarizes a company's revenues and expenses over a specific period. This document helps assess the financial performance of a business by showing how much money was made or lost during that time frame.

Why is the Profit and Loss form important?

The Profit and Loss form is crucial for understanding a business's profitability. It provides insights into revenue trends, cost management, and overall financial health. Stakeholders, including investors and management, use this information to make informed decisions regarding operations and strategy.

How often should a Profit and Loss form be prepared?

Typically, businesses prepare Profit and Loss forms on a monthly, quarterly, or annual basis. The frequency may depend on the size of the business and its reporting requirements. Regular updates allow for timely analysis and adjustments to financial strategies.

What information is included in a Profit and Loss form?

A Profit and Loss form generally includes total revenue, cost of goods sold, gross profit, operating expenses, and net profit or loss. Each section breaks down various categories, such as sales revenue, salaries, rent, and utilities, providing a clear picture of financial performance.

Who uses the Profit and Loss form?

Multiple parties utilize the Profit and Loss form. Business owners and managers review it to assess performance and plan budgets. Investors and creditors analyze it to evaluate the company’s financial stability and profitability. Accountants also rely on this document for tax preparation and financial reporting.

How can I improve my Profit and Loss statement?

Improving a Profit and Loss statement involves increasing revenues and reducing expenses. Businesses can enhance revenue by exploring new markets, improving sales strategies, or diversifying products. Cost control measures, such as negotiating better supplier contracts or reducing overhead, can also contribute to a healthier Profit and Loss statement.

What are common mistakes to avoid when preparing a Profit and Loss form?

Common mistakes include failing to categorize expenses correctly, not updating figures regularly, and overlooking non-operating income or expenses. Additionally, it's important to ensure that all revenue streams are accounted for to provide an accurate representation of financial performance.

When filling out a Profit and Loss form, it's easy to make mistakes that can lead to inaccurate financial reporting. Here are six common errors to watch out for:

Many people forget to include all sources of income. This can result in an underreporting of revenue, which may affect financial analysis and tax obligations.

Expenses should be categorized correctly. Misclassifying expenses can distort profitability and lead to issues during audits.

Some individuals fail to account for non-operating income, such as interest or investment income. This oversight can provide an incomplete picture of financial health.

Neglecting to account for depreciation can inflate profit figures. It's important to accurately reflect the cost of assets over time.

Many overlook the importance of comparing current figures with those from previous periods. This comparison can highlight trends and areas needing attention.

Without proper documentation, verifying figures becomes challenging. Keeping receipts and records helps ensure accuracy and provides a clear audit trail.

By being aware of these common mistakes, individuals can improve the accuracy of their Profit and Loss forms and gain better insights into their financial performance.

The Profit and Loss form is a crucial document for any business, providing a clear snapshot of financial performance over a specific period. However, several other forms and documents often accompany it, each serving a unique purpose that enhances the overall understanding of a company's financial health. Below is a list of five such documents.

Each of these documents plays a vital role in painting a comprehensive picture of a business's financial landscape. Together with the Profit and Loss form, they provide valuable insights that can inform strategic decisions and foster growth.

The Profit and Loss statement, often called an income statement, is similar to a balance sheet. Both documents provide a snapshot of a company’s financial health, but they focus on different aspects. While the Profit and Loss statement summarizes revenues and expenses over a specific period, the balance sheet presents assets, liabilities, and equity at a single point in time. Together, they give a comprehensive view of a company’s financial status.

Another document akin to the Profit and Loss statement is the cash flow statement. This report details how cash moves in and out of a business. It highlights operating, investing, and financing activities. Unlike the Profit and Loss statement, which records revenues and expenses, the cash flow statement focuses solely on cash transactions, providing insights into liquidity and cash management.

The statement of retained earnings is also similar to the Profit and Loss statement. This document shows how profits are retained in the business over time. It starts with the previous period's retained earnings, adds net income from the Profit and Loss statement, and subtracts dividends paid. This connection illustrates how profits impact the overall equity of the business.

Comparatively, the budget report shares similarities with the Profit and Loss statement. Both documents track financial performance, but the budget report projects future income and expenses based on estimates. It serves as a planning tool, while the Profit and Loss statement reflects actual financial results, allowing for comparisons between expected and actual performance.

The trial balance is another related document. It lists all accounts from the general ledger and their balances at a specific time. While it doesn’t summarize revenues and expenses, it ensures that total debits equal total credits, which is essential for accurate financial reporting. The Profit and Loss statement is derived from the trial balance, making it a crucial step in the accounting process.

The income tax return also parallels the Profit and Loss statement. This document reports a business's income, deductions, and tax liability to the IRS. It uses figures from the Profit and Loss statement to determine taxable income, demonstrating how profits translate into tax obligations. Both documents are essential for understanding a business's financial standing and obligations.

The sales report can be seen as similar to the Profit and Loss statement, especially in terms of revenue generation. It focuses specifically on sales figures, detailing the volume and value of products sold over a certain period. While the Profit and Loss statement encompasses all revenues and expenses, the sales report zeroes in on sales performance, providing valuable insights for revenue analysis.

The accounts receivable aging report shares a connection with the Profit and Loss statement. It tracks outstanding invoices and how long they have been unpaid. This document impacts the Profit and Loss statement by influencing cash flow and potential bad debt expenses. Understanding receivables is crucial for assessing a company's financial health and operational efficiency.

The financial forecast is another document that aligns with the Profit and Loss statement. It estimates future revenues and expenses based on historical data and market trends. While the Profit and Loss statement reflects past performance, the financial forecast helps in strategic planning, allowing businesses to anticipate future financial outcomes and make informed decisions.

Lastly, the departmental income statement is similar to the Profit and Loss statement but focuses on the performance of specific departments within a business. It breaks down revenues and expenses by department, providing insights into which areas are profitable and which may need improvement. This targeted approach complements the overall Profit and Loss statement by offering a more granular view of financial performance.

When filling out a Profit and Loss form, attention to detail is crucial. Here are some important do's and don'ts to keep in mind:

Understanding the Profit and Loss (P&L) form is crucial for anyone involved in business finances. However, several misconceptions can cloud this understanding. Here are six common misconceptions about the Profit and Loss form:

This is not true. The P&L form provides a comprehensive view of both revenues and expenses, showing how much profit or loss a business has generated over a specific period.

Every business, regardless of size, can benefit from a P&L statement. Small businesses use it to track performance and make informed financial decisions.

While both documents are essential for understanding a business's financial health, they serve different purposes. The P&L focuses on income and expenses, while the balance sheet provides a snapshot of assets, liabilities, and equity at a specific point in time.

This misconception overlooks the distinction between fixed and variable costs. Understanding these categories can help businesses manage their expenses more effectively.

While it is useful for tax preparation, the P&L form is also a vital tool for internal management. It helps businesses analyze performance, set budgets, and make strategic decisions.

While it’s possible to estimate profits and losses, the P&L form provides a structured and detailed account that enhances accuracy and accountability in financial reporting.

By dispelling these misconceptions, individuals and businesses can better appreciate the importance of the Profit and Loss form in financial management.

Filling out and utilizing a Profit and Loss form can seem daunting, but it’s an essential tool for understanding your business's financial health. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can make the most out of your Profit and Loss form and steer your business toward success.