The Pennsylvania Promissory Note form serves as a vital financial instrument, facilitating the borrowing and lending process between individuals or entities. This legally binding document outlines the borrower's commitment to repay a specified sum of money to the lender within a predetermined timeframe. Key elements of the form include the principal amount, interest rate, payment schedule, and any applicable late fees. Additionally, it often specifies the consequences of default, ensuring both parties understand their rights and responsibilities. By clearly detailing the terms of the agreement, the Promissory Note helps to prevent misunderstandings and disputes, fostering a transparent relationship between the borrower and lender. Furthermore, it can be customized to suit various lending situations, making it a versatile tool in financial transactions across Pennsylvania.

Pennsylvania Promissory Note Template

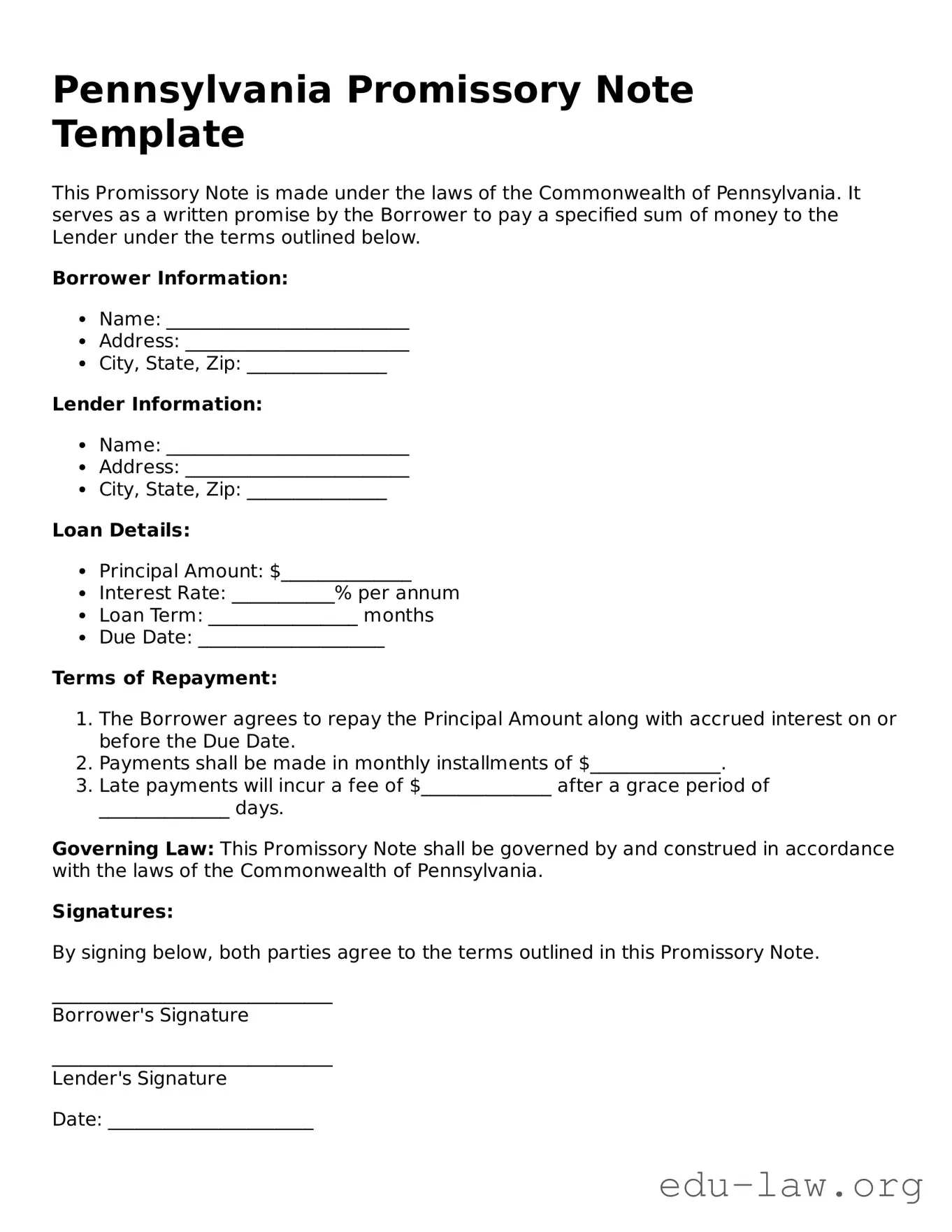

This Promissory Note is made under the laws of the Commonwealth of Pennsylvania. It serves as a written promise by the Borrower to pay a specified sum of money to the Lender under the terms outlined below.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

Governing Law: This Promissory Note shall be governed by and construed in accordance with the laws of the Commonwealth of Pennsylvania.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

______________________________

Borrower's Signature

______________________________

Lender's Signature

Date: ______________________

| Fact Name | Description |

|---|---|

| Definition | A Pennsylvania promissory note is a written promise to pay a specific amount of money to a designated person or entity at a defined time. |

| Governing Law | Promissory notes in Pennsylvania are governed by the Uniform Commercial Code (UCC), specifically Article 3, which covers negotiable instruments. |

| Basic Elements | To be valid, a promissory note must include the amount owed, the interest rate (if any), the due date, and the signatures of the parties involved. |

| Interest Rates | Pennsylvania law allows for the inclusion of interest rates in promissory notes, but they must comply with state usury laws, which limit the maximum rate that can be charged. |

| Enforceability | A properly executed promissory note is legally enforceable in Pennsylvania, meaning the lender can take legal action if the borrower defaults. |

| Transferability | Promissory notes can be transferred to third parties, making them negotiable instruments under Pennsylvania law, provided they meet certain criteria. |

After obtaining the Pennsylvania Promissory Note form, it's essential to complete it accurately to ensure that all necessary information is included. This will help both parties understand their obligations clearly and avoid potential disputes in the future.

What is a Pennsylvania Promissory Note?

A Pennsylvania Promissory Note is a written agreement in which one party (the borrower) promises to pay a specific sum of money to another party (the lender) at a predetermined time or on demand. This document outlines the terms of the loan, including the interest rate, payment schedule, and any penalties for late payments. It serves as a legal record of the transaction and can be enforced in court if necessary.

Who can use a Promissory Note in Pennsylvania?

Any individual or business can use a Promissory Note in Pennsylvania. It is commonly utilized by lenders and borrowers in personal loans, business loans, or real estate transactions. Both parties must be of legal age and have the capacity to enter into a contract. It is important that the terms are clear and agreed upon by both parties to avoid disputes later on.

What are the essential elements of a valid Promissory Note?

A valid Promissory Note must include several key elements. These include the names and addresses of both the borrower and lender, the principal amount borrowed, the interest rate, the repayment schedule, and the maturity date. Additionally, it should specify any late fees or penalties for missed payments. The document must be signed by the borrower to be enforceable.

Is it necessary to have a lawyer review a Promissory Note?

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. Any modifications should be documented in writing and signed by both the borrower and lender to ensure they are enforceable. This helps maintain clarity and prevents misunderstandings regarding the new terms.

Incorrect Names: Many individuals forget to write the full legal names of both the borrower and the lender. Abbreviations or nicknames can lead to confusion.

Missing Dates: Failing to include the date when the note is signed can create issues later. Always ensure that the date is clearly written.

Unclear Loan Amount: Some people write the loan amount incorrectly or omit it entirely. It is crucial to specify the exact amount in both numbers and words.

Payment Terms Not Specified: Not detailing the payment schedule or interest rate can lead to misunderstandings. Clearly outline how and when payments will be made.

Signature Issues: Sometimes, individuals forget to sign the document or do not have the necessary witnesses. Ensure that all required signatures are present to validate the note.

In Pennsylvania, a Promissory Note is often accompanied by other forms and documents that help clarify the terms of the agreement and protect the interests of both parties. Below are four common documents that may be used alongside a Promissory Note.

These documents collectively ensure that both parties have a clear understanding of their rights and responsibilities, thereby minimizing potential disputes in the future.

A loan agreement is a document that outlines the terms of a loan between a lender and a borrower. Like a Pennsylvania Promissory Note, it specifies the amount borrowed, the interest rate, and the repayment schedule. However, a loan agreement typically includes more detailed terms, such as collateral requirements and conditions for default. Both documents serve to formalize the borrowing process, ensuring that both parties understand their obligations.

A mortgage is another document that shares similarities with a promissory note. A mortgage secures a loan with real property as collateral. While a promissory note is a promise to repay the borrowed amount, the mortgage provides the lender with a legal claim to the property in case of default. Both documents are essential in real estate transactions, working together to protect the interests of the lender.

An IOU, or informal acknowledgment of debt, is a simpler document than a promissory note. It serves as a written reminder that one party owes money to another. While an IOU may not include detailed terms like interest rates or repayment schedules, it still establishes a debtor-creditor relationship. Both documents signify an obligation to repay, but an IOU lacks the formal structure and legal enforceability of a promissory note.

A personal guarantee is a document where an individual agrees to repay a loan if the primary borrower defaults. Similar to a promissory note, it creates a financial obligation. However, a personal guarantee often involves a third party who is not the original borrower. Both documents aim to provide security for the lender, but a personal guarantee adds an additional layer of accountability.

A conditional sales agreement is a contract where the buyer takes possession of an item while the seller retains ownership until the purchase price is fully paid. Like a promissory note, it outlines payment terms and obligations. However, a conditional sales agreement typically involves tangible goods rather than cash loans. Both documents help clarify the responsibilities of the parties involved in a financial transaction.

A lease agreement is a contract between a landlord and tenant that outlines the terms of renting property. While it is primarily focused on rental payments, it shares similarities with a promissory note in that it establishes a financial obligation. Both documents detail payment amounts and schedules, ensuring that both parties are clear on their commitments. However, a lease agreement also includes terms related to property use and maintenance.

A business loan agreement is specifically designed for loans taken out by businesses. It details the loan amount, interest rates, and repayment terms, much like a promissory note. However, it may also include clauses regarding the use of funds and business performance metrics. Both documents serve to formalize financial arrangements, providing a clear understanding of obligations for both lenders and borrowers.

A credit agreement outlines the terms under which a borrower can access credit from a lender. Similar to a promissory note, it specifies the amount of credit, interest rates, and repayment terms. However, a credit agreement often allows for ongoing borrowing and repayment, while a promissory note typically pertains to a single loan transaction. Both documents are vital for establishing the terms of borrowing and repayment.

A settlement agreement is a document that outlines the terms of resolving a dispute between parties, often involving a payment. Similar to a promissory note, it may include payment amounts and schedules. However, a settlement agreement usually addresses the resolution of a legal claim rather than a straightforward loan. Both documents create binding obligations, ensuring that the terms agreed upon are enforceable.

A forbearance agreement is a temporary arrangement between a lender and borrower to postpone or reduce payments on a loan. Like a promissory note, it involves a financial obligation but focuses on modifying the original terms due to financial hardship. Both documents are essential for managing repayment expectations, but a forbearance agreement provides flexibility during difficult financial times.

When filling out the Pennsylvania Promissory Note form, it's important to ensure accuracy and clarity. Here’s a helpful list of dos and don’ts to guide you through the process.

By following these guidelines, you can create a clear and enforceable Promissory Note that protects both parties involved.

When it comes to the Pennsylvania Promissory Note form, several misconceptions can lead to confusion. Here’s a breakdown of some common misunderstandings:

Understanding these misconceptions can help individuals navigate the process more confidently and ensure that they create effective and enforceable promissory notes.

When filling out and using the Pennsylvania Promissory Note form, it’s important to keep several key points in mind. Understanding these can help ensure that the document serves its intended purpose effectively.

By paying attention to these key takeaways, you can create a solid Promissory Note that meets the needs of both the borrower and the lender while complying with Pennsylvania regulations.