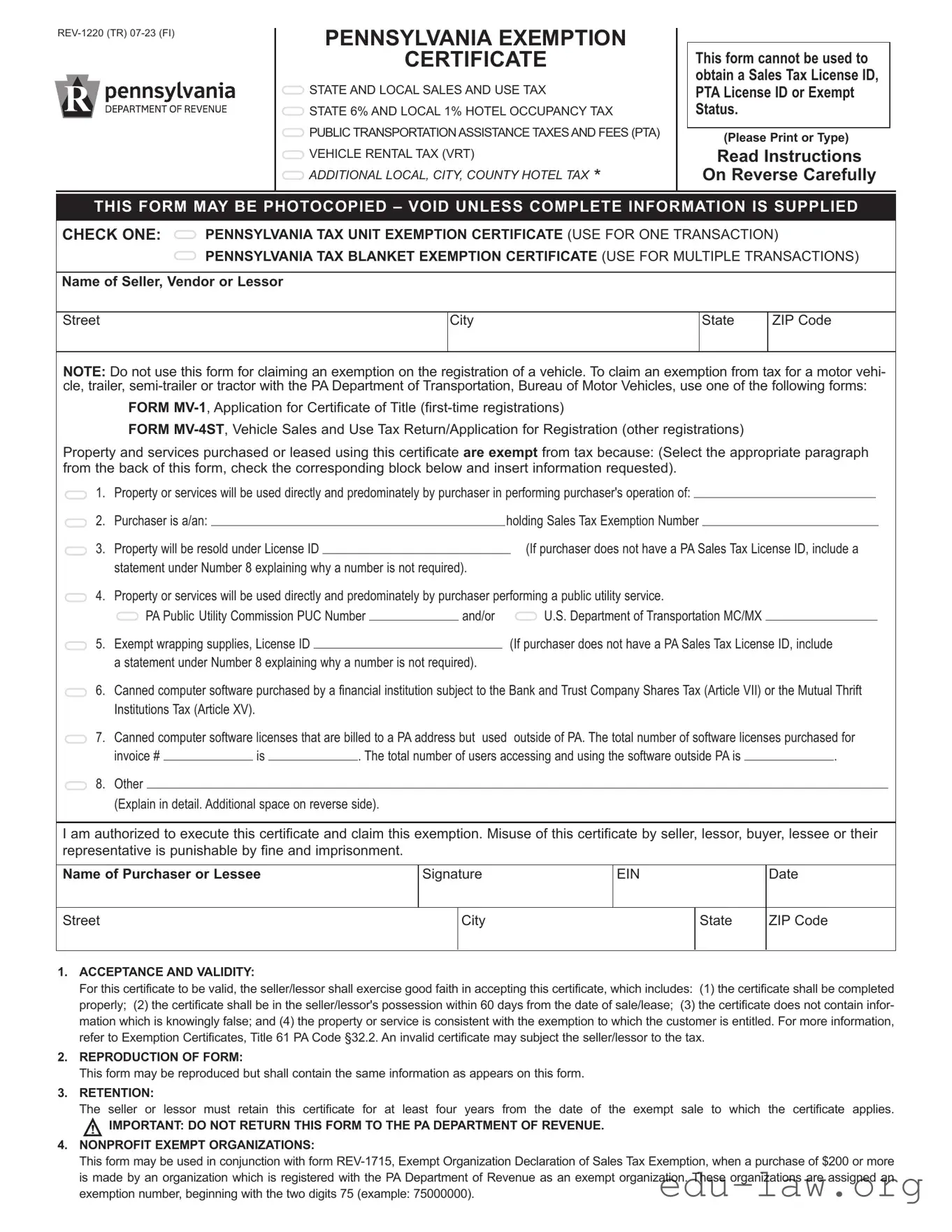

The Pennsylvania Exemption Certificate, officially designated as form REV-1220, serves as a crucial document for individuals and organizations seeking to claim exemptions from various state and local taxes. This form is specifically designed for use in transactions involving state and local sales and use tax, hotel occupancy tax, public transportation assistance taxes, and vehicle rental tax. It is important to note that this certificate cannot be utilized to obtain a Sales Tax Account ID or Exempt Status. Two primary options exist for users: the Pennsylvania Tax Unit Exemption Certificate, which is applicable for a single transaction, and the Pennsylvania Tax Blanket Exemption Certificate, intended for multiple transactions. To ensure proper use, the form requires detailed information about the seller, vendor, or lessor, as well as the purchaser or lessee. The certificate must be filled out completely and accurately, as incomplete forms are considered void. Validity hinges on the seller's good faith in accepting the certificate, which includes retaining it for at least four years and ensuring that the information provided is truthful and relevant to the exemption being claimed. Various exemptions are available, including those for nonprofit organizations, public utilities, and specific industries like manufacturing and agriculture. Understanding the nuances of this form is essential for both purchasers and sellers to navigate the complexities of Pennsylvania tax regulations effectively.

PENNSYLVANIA EXEMPTION

CERTIFICATE

STATE AND LOCAL SALES AND USE TAX

STATE 6% AND LOCAL 1% HOTEL OCCUPANCY TAX

PUBLIC TRANSPORTATION ASSISTANCE TAXES AND FEES (PTA)

VEHICLE RENTAL TAX (VRT)

ADDITIONAL LOCAL, CITY, COUNTY HOTEL TAX *

This form cannot be used to obtain a Sales Tax License ID, PTA License ID or Exempt Status.

(Please Print or Type)

Read Instructions

On Reverse Carefully

THIS FORM MAY BE PHOTOCOPIED – VOID UNLESS COMPLETE INFORMATION IS SUPPLIED

CHECK ONE: PENNSYLVANIA TAX UNIT EXEMPTION CERTIFICATE (USE FOR ONE TRANSACTION) PENNSYLVANIA TAX BLANKET EXEMPTION CERTIFICATE (USE FOR MULTIPLE TRANSACTIONS)

Name of Seller, Vendor or Lessor

Street

City

State

ZIP Code

NOTE: Do not use this form for claiming an exemption on the registration of a vehicle. To claim an exemption from tax for a motor vehi- cle, trailer,

FORM

FORM

Property and services purchased or leased using this certificate are exempt from tax because: (Select the appropriate paragraph from the back of this form, check the corresponding block below and insert information requested).

1. |

Property or services will be used directly and predominately by purchaser in performing purchaser's operation of: |

|

|

|

|

|

|||||||||||||||

2. |

Purchaser is a/an: |

|

|

|

|

|

|

|

|

|

|

holding Sales Tax Exemption Number |

|

|

|

|

|||||

3. |

Property will be resold under License ID |

|

|

|

|

|

|

(If purchaser does not have a PA Sales Tax License ID, include a |

|||||||||||||

|

statement under Number 8 explaining why a number is not required). |

|

|

|

|

|

|

|

|

|

|||||||||||

4. |

Property or services will be used directly and predominately by purchaser performing a public utility service. |

|

|

||||||||||||||||||

|

PA Public Utility Commission PUC Number |

|

and/or |

|

|

U.S. Department of Transportation MC/MX |

|

|

|

||||||||||||

5. |

Exempt wrapping supplies, License ID |

|

|

|

|

|

|

(If purchaser does not have a PA Sales Tax License ID, include |

|

|

|||||||||||

|

a statement under Number 8 explaining why a number is not required). |

|

|

|

|

|

|

|

|

|

|||||||||||

6. |

Canned computer software purchased by a financial institution subject to the Bank and Trust Company Shares Tax (Article VII) or the Mutual Thrift |

||||||||||||||||||||

|

Institutions Tax (Article XV). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

7. |

Canned computer software licenses that are billed to a PA address but used outside of PA. The total number of software licenses purchased for |

||||||||||||||||||||

|

invoice # |

|

|

is |

|

|

. The total number of users accessing and using the software outside PA is |

|

. |

|

|||||||||||

8. |

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Explain in detail. Additional space on reverse side).

I am authorized to execute this certificate and claim this exemption. Misuse of this certificate by seller, lessor, buyer, lessee or their representative is punishable by fine and imprisonment.

Name of Purchaser or Lessee |

Signature |

EIN |

Date |

|

|

|

|

Street

City

State

ZIP Code

1.ACCEPTANCE AND VALIDITY:

For this certificate to be valid, the seller/lessor shall exercise good faith in accepting this certificate, which includes: (1) the certificate shall be completed properly; (2) the certificate shall be in the seller/lessor's possession within 60 days from the date of sale/lease; (3) the certificate does not contain infor- mation which is knowingly false; and (4) the property or service is consistent with the exemption to which the customer is entitled. For more information, refer to Exemption Certificates, Title 61 PA Code §32.2. An invalid certificate may subject the seller/lessor to the tax.

2.REPRODUCTION OF FORM:

This form may be reproduced but shall contain the same information as appears on this form.

3.RETENTION:

The seller or lessor must retain this certificate for at least four years from the date of the exempt sale to which the certificate applies.

IMPORTANT: DO NOT RETURN THIS FORM TO THE PA DEPARTMENT OF REVENUE.

4.NONPROFIT EXEMPT ORGANIZATIONS:

This form may be used in conjunction with form

GENERAL INSTRUCTIONS

Those purchasers set forth below may use this form in connection with the claim for exemption for the following taxes:

a.State and local sales and use tax;

b.PTA rental fee or tax on leases of motor vehicles;

c.Hotel occupancy tax (state 6%, Philadelphia 1%, Allegheny 1%) if referenced with the symbol (●);

d.PTA fee on the purchase of tires if referenced with the symbol (+);

e.Vehicle rental tax (VRT).

EXEMPTION REASONS

1.) Property and/or services will be used directly and predominately by pur- chaser in performing purchaser's operation of:

A.Manufacturing

B.Mining

C.Dairying

D.Processing

E.Farming

F.Shipbuilding

G.Timbering

This exemption is not valid for property or services used in: (a) construct- ing, repairing or remodeling of real property, other than real property used directly in exempt operations; or (b) maintenance, managerial, administra- tive, supervisory, sales, delivery, warehousing or other nonoperational activities. This exemption is not valid for vehicles that are required to be registered under the Vehicle Code, as well as supplies and repair parts for such vehicles, the PTA tire fee, and certain taxable services.

2.) Purchaser is a/an:

+A. Instrumentality of the commonwealth (to include public schools and state universities).

+B. Political subdivision of the commonwealth (includes townships and boroughs).

+l C. Municipal authority created under the Municipality Authorities Acts.

+l D. Electric cooperative corporations created under the Electric Cooperative Law of 1990.

lE. Cooperative agricultural associations required to pay corpo- rate net income tax under the Cooperative Agricultural Association Corporate Net Income Tax Act (exemption not valid for registered vehicles).

+ l F. Credit unions organized under Federal Credit Union Act or Commonwealth Credit Union Act.

+l G. U.S. government, its agencies and instrumentalities.

l H. Federal employee on official business (exemption limited to hotel occupancy tax only. A copy of orders or statement from supervisor must be attached to this certificate).

I.School bus operator (This exemption certificate is limited to the purchase of parts, repairs or maintenance services upon vehicles licensed as school buses by the PA Department of Transportation).

J.Charter Schools and Community Colleges.

Renewable Entities beginning with “75”:

K.Religious Organization

L.Nonprofit Educational Institution

M.Charitable Organization

Permanent Exemptions beginning with the two numbers “75”:

N.Volunteer Fire Company

O.Relief Association

Special Exemptions

P.Direct Pay Permit Holder

Q.Individual Holding Diplomatic ID

R.Keystone Opportunity Zone (beginning with two digit 72 account number)

S.Tourist Promotion Agency

Exemptions for exempt organizations K through S are limited to purchases of tangible personal property or services for use and not for sale. Exempt organizations K - O above, shall have an sales tax exemption certificate number assigned by the PA Department of Revenue. Exempt organiza- tions

3.) Property and/or services will be resold or rented in the ordinary course of purchaser's business. If purchaser does not have a PA Sales Tax License ID (8 digit number assigned by the department), complete Number 8 explaining why such number is not required. This exemption is valid for property or services to be resold: (1) in original form; or (2) as an ingredient or component of other property.

4.) Property or services will be used directly and predominately by purchaser in the production, delivery or rendition of public utility services as defined by the PA Utility Code.

This exemption is not valid for property or services used for the following:

(1)construction, improvement, repair or maintenance of real property, other than real property used directly in rendering the public utility services; or (2) managerial, administrative, supervisor, sales or other nonopera- tional activities; or (3) vehicles, as well as supplies and repair parts for such vehicles, unless the predominant use is for providing a common car- rier service; or (4) tools and equipment used but not installed in mainte- nance of facilities or direct use equipment. Tools and equipment used to repair "direct use" property are exempt from tax.

5.) Vendor/seller purchasing wrapping supplies and nonreturnable containers used to wrap property which is sold to others.

6.) Canned computer software or services to canned computer software directly utilized in conducting the business of banking purchased by a financial institution subject to the Bank and Trust Company Shares Tax (Article VII) or the Mutual Thrift Institutions Tax (Article XV).

7.) Seller is required to collect tax on canned software accessed remotely when the user is located in PA. If the billing address is a PA address, the presumption is that all users are located in PA. Purchaser is responsible for apportioning and remitting the tax due to each taxing jurisdiction and must provide the total number of licenses purchased and the number of those licenses used outside PA on Line 8. Please note that any unused licenses will be considered to be allocated to PA.

8.) Other (Attach a separate sheet of paper if more space is required).

*Employees or representatives of the Commonwealth traveling on Commonwealth duty are exempt from any taxes on hotel stays or room rentals imposed by local governments that are in addition to the 6% state tax and the 1% Philadelphia and Allegheny County hotel occupancy tax.

| Fact Name | Description |

|---|---|

| Form Title | Pennsylvania Exemption Certificate for State and Local Sales and Use Tax. |

| Form Code | REV-1220 (TR) 05-20 (FI). |

| Tax Rates | State sales tax is 6%, with an additional local tax of 1% for hotel occupancy. |

| Usage | This form is used to claim exemptions for specific transactions, not for obtaining a Sales Tax Account ID. |

| Exemption Types | Includes exemptions for manufacturing, mining, and public utility services, among others. |

| Validity Conditions | The seller must accept the certificate in good faith and retain it for four years. |

| Nonprofit Use | Nonprofit organizations can use this form along with REV-1715 for purchases over $200. |

| Prohibited Uses | This form cannot be used for vehicle registrations or for claiming exemptions on certain services. |

| Legal Reference | Governing laws include Title 61 PA Code §32.2 regarding exemption certificates. |

| Signature Requirement | The purchaser or lessee must sign the form to claim the exemption. |

Completing the Pennsylvania Exemption Certificate (REV-1220) is a straightforward process. This form is essential for claiming exemptions from specific taxes related to purchases or leases. Follow the steps below to ensure accurate completion.

Once completed, the seller or lessor must keep this certificate on file for at least four years. Misuse of the certificate can lead to penalties, so ensure all information is accurate and truthful.

What is the PA Exemption Certificate (REV-1220) used for?

The PA Exemption Certificate is a document used in Pennsylvania to claim exemptions from certain state and local sales and use taxes. This includes exemptions for hotel occupancy taxes, public transportation assistance taxes, and vehicle rental taxes. It is important to note that this form cannot be used to obtain a Sales Tax Account ID or to claim exempt status. It is specifically designed for transactions where the purchaser qualifies for tax exemptions based on their operations or status.

Who can use the PA Exemption Certificate?

Various entities can use the PA Exemption Certificate, including nonprofit organizations, government agencies, and certain businesses. For instance, if a purchaser is a public school, a political subdivision, or a charitable organization, they may qualify for exemption. The form allows users to specify the reason for their exemption, such as using the purchased property or services directly in their operations or reselling them in the ordinary course of business.

How should the PA Exemption Certificate be completed?

To ensure the certificate is valid, it must be completed accurately. The seller or lessor should verify that the form includes all necessary information, such as the purchaser's name, address, and the specific reason for the exemption. Additionally, the seller must retain the certificate for at least four years from the date of the exempt sale. If the purchaser does not have a PA Sales Tax Account ID, they must provide an explanation as to why it is not required.

What happens if the PA Exemption Certificate is misused?

Misuse of the PA Exemption Certificate can lead to serious consequences. If the information on the certificate is found to be false or if it is not completed correctly, the seller or lessor may be held liable for the tax. Furthermore, penalties can include fines and imprisonment. Therefore, it is crucial for both the purchaser and seller to understand the terms and conditions surrounding the use of this certificate to avoid any legal issues.

Not Reading Instructions Thoroughly: Many individuals overlook the importance of reading the instructions on the back of the form. These instructions provide essential guidance on how to complete the form correctly, ensuring that all necessary information is included.

Failing to Select the Correct Exemption Type: The form offers options for either a one-time transaction or multiple transactions. Choosing the wrong type can lead to complications, as the exemption certificate must match the nature of the purchase.

Incomplete Information: Leaving sections of the form blank can render it invalid. Each field must be filled out completely, including the name, address, and exemption reason, to avoid delays or rejections.

Incorrectly Identifying the Exemption Reason: It is crucial to select the appropriate reason for the exemption. Misidentifying the exemption can lead to tax liabilities and potential penalties.

Not Providing a Sales Tax Account ID: If applicable, individuals must include their Sales Tax Account ID. Failing to do so without a valid explanation can cause issues with the exemption claim.

Neglecting to Sign the Form: A common oversight is forgetting to sign the form. The signature is a critical part of the document, indicating that the purchaser is authorized to claim the exemption.

When dealing with the Pennsylvania Exemption Certificate (REV-1220), several other forms and documents may be necessary to ensure compliance with state tax regulations. Each of these documents serves a specific purpose in the exemption process and can help clarify the eligibility for tax exemptions. Below is a list of commonly used forms that accompany the PA form.

Understanding these forms and their purposes is crucial for ensuring compliance with Pennsylvania tax laws. Proper documentation can facilitate smoother transactions and prevent potential issues with tax authorities.

The Pennsylvania Exemption Certificate (REV-1220) shares similarities with the IRS Form W-9, Request for Taxpayer Identification Number and Certification. Both forms are utilized to certify an entity's tax-exempt status or to provide necessary identification information for tax reporting purposes. The W-9 is primarily used by individuals and businesses to furnish their taxpayer identification number (TIN) to entities that will report payments made to them. Similarly, the PA Exemption Certificate allows purchasers to claim exemption from certain taxes, ensuring that sellers have the correct information to process transactions without tax implications.

Another document that resembles the PA Exemption Certificate is the IRS Form 990, Return of Organization Exempt from Income Tax. Nonprofit organizations use Form 990 to report their financial information to the IRS, demonstrating their compliance with tax-exempt regulations. Just like the PA Exemption Certificate, which helps organizations claim tax exemptions for purchases, Form 990 ensures that nonprofits maintain their tax-exempt status by providing transparency about their finances and activities.

The Certificate of Exempt Use (Form ST-5) from New York also parallels the PA Exemption Certificate. This form is used by purchasers to claim exemption from sales tax on items intended for resale or for specific exempt purposes. Both documents require users to provide detailed information about the nature of the purchase and the reason for the exemption, ensuring that sellers can validate the tax-exempt status of the buyer.

In addition, the Texas Sales and Use Tax Resale Certificate serves a similar purpose. This certificate allows buyers in Texas to purchase items tax-free if they intend to resell them. Like the PA Exemption Certificate, it requires the buyer to provide their sales tax permit number and details about the transaction. Both forms are essential for maintaining compliance with state tax laws and preventing tax liabilities for exempt purchases.

The Illinois Sales Tax Exemption Certificate is another comparable document. This certificate enables qualifying organizations to make tax-exempt purchases in Illinois. Both the Illinois and Pennsylvania forms require users to specify the reason for the exemption and to provide identifying information about the buyer and seller. This helps ensure that tax-exempt transactions are properly documented and justified.

Moreover, the California Resale Certificate serves a similar function. It allows businesses in California to buy goods without paying sales tax if those goods are intended for resale. Like the PA Exemption Certificate, it requires the buyer to furnish their seller’s permit number and details about the transaction. Both certificates are crucial for businesses to avoid unnecessary tax burdens when purchasing inventory.

The Florida Annual Resale Certificate for Sales Tax is another document that aligns with the PA Exemption Certificate. This form is used by retailers in Florida to purchase items tax-free for resale. Similar to the PA form, it requires detailed information about the seller and the nature of the transaction, ensuring compliance with state tax regulations and preventing tax liabilities on exempt purchases.

Additionally, the Massachusetts Sales Tax Exempt Use Certificate mirrors the PA Exemption Certificate. This document allows buyers in Massachusetts to claim exemption from sales tax on specific purchases. Both forms require users to provide a valid reason for the exemption and necessary identification details, ensuring that sellers can verify the tax-exempt status of their customers.

Finally, the New Jersey Resale Certificate is akin to the PA Exemption Certificate. This certificate allows businesses in New Jersey to purchase goods without paying sales tax if they plan to resell those goods. Both documents require the buyer to provide their tax identification number and details about the transaction, helping to maintain compliance with state tax laws and ensuring proper documentation of tax-exempt purchases.

When filling out the Pennsylvania Exemption Certificate (REV-1220), it's crucial to follow specific guidelines to ensure the form is completed accurately. Here’s a list of dos and don’ts to help you navigate the process effectively:

By adhering to these guidelines, you can ensure a smoother process when completing the Pennsylvania Exemption Certificate.

Misconceptions about the Pennsylvania Exemption Certificate (REV-1220) can lead to confusion regarding its proper use. Below are ten common misconceptions along with clarifications.

This is incorrect. The Pennsylvania Exemption Certificate cannot be used to obtain a Sales Tax Account ID, PTA Account ID, or Exempt Status.

Not all purchases qualify for tax exemption. The exemption applies only to specific transactions that meet the criteria outlined in the form.

This is false. To claim an exemption for vehicle registration, different forms such as FORM MV-1 or FORM MV-4ST must be used.

Sellers must exercise good faith in accepting the certificate, ensuring it is completed properly and in their possession within 60 days of the transaction.

The seller must retain the certificate for at least four years from the date of the exempt sale for it to remain valid.

Nonprofit organizations can use this form, but only in conjunction with form REV-1715 for purchases of $200 or more, and they must have a registered exemption number.

This is not true. Exemptions do not apply to services related to the construction, repair, or maintenance of real property, among other exclusions.

Misuse of the certificate can lead to penalties, including fines and imprisonment. The seller or purchaser can be held accountable for false claims.

Exemptions do not apply to vehicles required to be registered under the Vehicle Code, nor to supplies and repair parts for such vehicles.

This is misleading. Only specific types of organizations, such as those defined in the exemption categories, can utilize the form for tax exemption.

Key Takeaways for Filling Out and Using the PA Exemption Certificate (REV-1220)