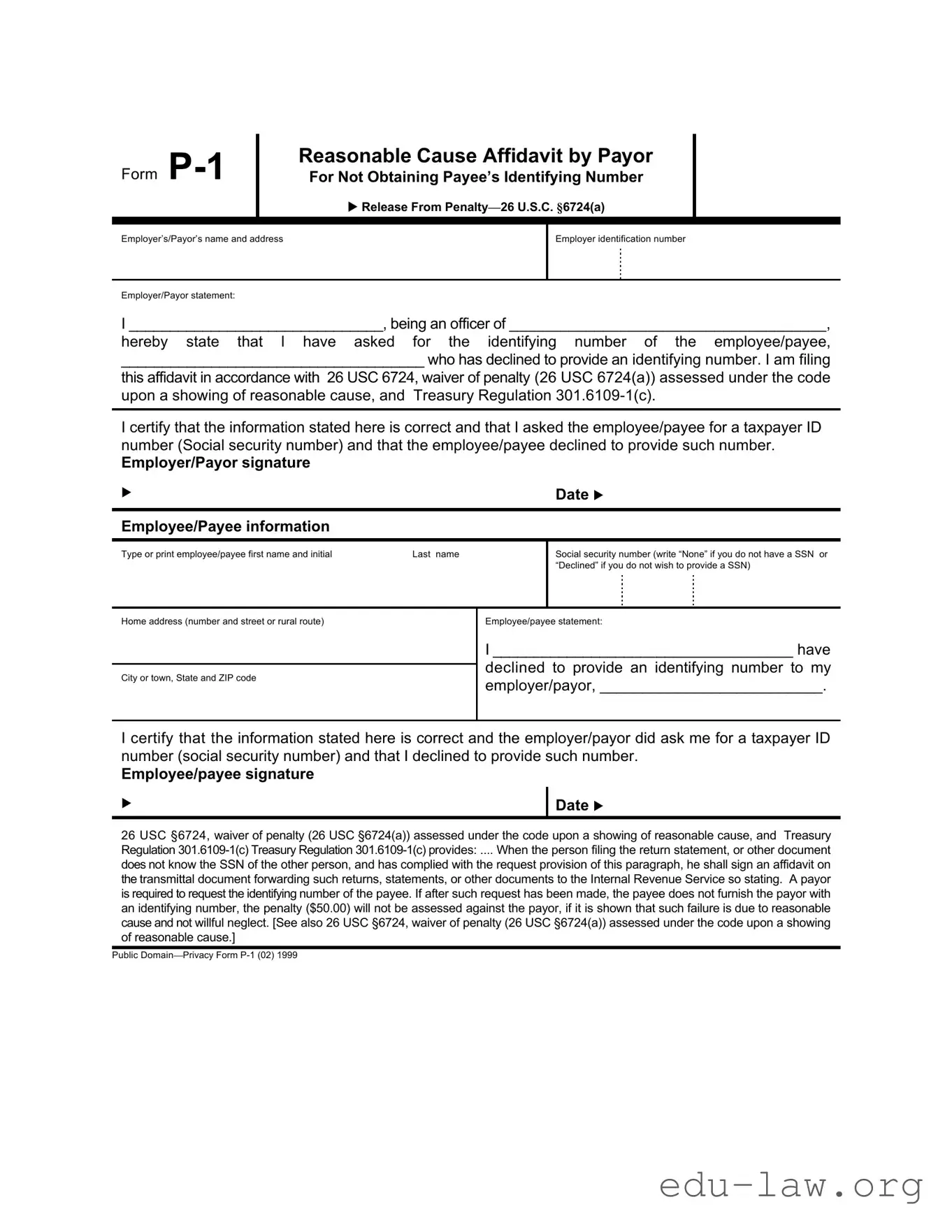

The P-1 form serves a critical role in the relationship between employers and payees regarding the provision of identifying numbers, specifically Social Security numbers. This form, officially titled the Reasonable Cause Affidavit by Payor for Not Obtaining Payee’s Identifying Number, is utilized when a payor has requested an identifying number from an employee or payee, but the payee has declined to provide it. By completing this affidavit, the payor can demonstrate compliance with IRS requirements under 26 U.S.C. §6724(a), which allows for a waiver of penalties associated with the failure to provide a taxpayer ID number. The form requires the payor to provide their name, address, and employer identification number, along with a statement affirming that they have made a request for the identifying number. The payee must also provide their information and confirm their refusal to disclose their taxpayer ID. This mutual certification is essential, as it establishes a record that the payor acted in good faith and attempted to obtain the necessary information, thereby protecting them from potential penalties for non-compliance.

Form

Reasonable Cause Affidavit by Payor

For Not Obtaining Payee’s Identifying Number

uRelease From

Employer’s/Payor’s name and address

Employer identification number

Employer/Payor statement:

I _______________________________, being an officer of _____________________________________,

hereby state that I have asked for the identifying number of the employee/payee,

_____________________________________ who has declined to provide an identifying number. I am filing

this affidavit in accordance with 26 USC 6724, waiver of penalty (26 USC 6724(a)) assessed under the code upon a showing of reasonable cause, and Treasury Regulation

I certify that the information stated here is correct and that I asked the employee/payee for a taxpayer ID number (Social security number) and that the employee/payee declined to provide such number.

Employer/Payor signature

u |

Date u |

|

Employee/Payee information

Type or print employee/payee first name and initial |

Last name |

Social security number (write “None” if you do not have a SSN or “Declined” if you do not wish to provide a SSN)

Home address (number and street or rural route)

City or town, State and ZIP code

Employee/payee statement:

I ____________________________________ have

declined to provide an identifying number to my employer/payor, __________________________.

I certify that the information stated here is correct and the employer/payor did ask me for a taxpayer ID number (social security number) and that I declined to provide such number.

Employee/payee signature

u

Date u

26 USC §6724, waiver of penalty (26 USC §6724(a)) assessed under the code upon a showing of reasonable cause, and Treasury Regulation

does not know the SSN of the other person, and has complied with the request provision of this paragraph, he shall sign an affidavit on the transmittal document forwarding such returns, statements, or other documents to the Internal Revenue Service so stating. A payor is required to request the identifying number of the payee. If after such request has been made, the payee does not furnish the payor with an identifying number, the penalty ($50.00) will not be assessed against the payor, if it is shown that such failure is due to reasonable cause and not willful neglect. [See also 26 USC §6724, waiver of penalty (26 USC §6724(a)) assessed under the code upon a showing of reasonable cause.]

Public

| Fact Name | Description |

|---|---|

| Form Purpose | The P-1 form is a Reasonable Cause Affidavit by Payor for not obtaining the payee’s identifying number. |

| Governing Law | This form is governed by 26 U.S.C. §6724(a) and Treasury Regulation 301.6109-1(c). |

| Employer Requirement | Employers must request the identifying number from their employees or payees. |

| Penalty Waiver | If the payee declines to provide their identifying number, the penalty may be waived upon showing reasonable cause. |

| Affidavit Certification | The payor must certify that they requested the identifying number and that the payee declined to provide it. |

| Employee/Payee Statement | The payee also certifies that they declined to provide their identifying number to the employer/payor. |

| Signature Requirement | Both the employer/payor and the employee/payee must sign the form to validate the affidavit. |

| Information Accuracy | All information provided on the form must be accurate and truthful to avoid penalties. |

| Submission | The completed form must be submitted to the Internal Revenue Service along with any required tax documents. |

Once the P 1 form is completed, it should be submitted to the appropriate tax authority. This form serves to document the payor's reasonable cause for not obtaining the payee's identifying number, thereby potentially waiving any penalties associated with this omission.

What is the purpose of the P-1 form?

The P-1 form serves as a reasonable cause affidavit for employers or payors who have requested a payee's identifying number, such as a Social Security Number, but have not received it. This form allows the payor to demonstrate to the IRS that they have made a good faith effort to obtain the necessary information and are seeking a waiver of any potential penalties for failing to provide that number.

Who needs to fill out the P-1 form?

Both the employer or payor and the employee or payee must complete parts of the P-1 form. The employer or payor must sign the affidavit indicating they requested the identifying number, while the payee must acknowledge their refusal to provide it. This mutual acknowledgment is crucial for the form to serve its intended purpose.

What happens if the payee does not provide their identifying number?

If the payee declines to provide their identifying number after a request from the payor, the payor can still avoid penalties. By submitting the P-1 form, the payor can show that their failure to report the identifying number was due to reasonable cause and not willful neglect. This is important for compliance with IRS regulations and for protecting the payor from financial penalties.

What information is required on the P-1 form?

The P-1 form requires specific information, including the names and addresses of both the payor and payee, the payor's identification number, and the payee's Social Security Number or an indication of their refusal to provide it. Additionally, both parties must sign and date the form to certify that the information is accurate and complete.

Where do I submit the P-1 form?

The completed P-1 form should be submitted along with any relevant tax documents to the Internal Revenue Service (IRS). It is important to keep a copy of the form for your records, as it serves as evidence of your compliance with the request for the payee's identifying number.

Incomplete Information: One of the most common mistakes is failing to provide all required details. Ensure that the employer's name, address, and identification number are fully filled out.

Missing Signatures: Both the employer/payor and the employee/payee must sign the form. Omitting a signature can lead to delays or rejection of the affidavit.

Incorrect Identification Number: Providing an incorrect or invalid employer identification number can create complications. Double-check this number for accuracy.

Improper Employee/Payee Information: Ensure that the employee/payee's name is correctly typed, including any initials. Errors in this section can lead to confusion or processing issues.

Not Following Instructions: Each section of the form has specific instructions. Ignoring these can result in incomplete submissions. Read the guidelines carefully before filling out the form.

Failing to State Reason for Declining: If the employee/payee declines to provide their identifying number, they must clearly state this in the designated section. Lack of clarity here can lead to misunderstandings.

The P-1 form is utilized by employers or payors to assert reasonable cause for not obtaining an employee or payee's identifying number. Several other documents may accompany the P-1 form to provide additional context or fulfill specific requirements. Below is a list of commonly used forms and documents related to the P-1 form.

These documents collectively support the compliance and reporting requirements related to payments made to individuals and entities. Properly completing and submitting these forms helps avoid penalties and ensures accurate tax reporting.

The P-1 form is similar to the W-9 form, which is used by individuals to provide their taxpayer identification number to businesses or payers. Like the P-1, the W-9 requires the individual to certify that the information provided is accurate. Both forms serve to document the request for identifying information and establish that the payee has declined to provide it. The main difference is that the W-9 is typically filled out by the payee, while the P-1 is completed by the payor to demonstrate compliance with tax regulations when the payee refuses to provide their information.

Another document that resembles the P-1 form is the 1099 form. The 1099 is used to report income received by a payee, and it requires the payor to include the payee's taxpayer identification number. If the payee does not provide this information, the payor may face penalties. The P-1 form acts as a safeguard for the payor, showing that they have made an effort to obtain the necessary information and that the payee has chosen not to provide it. Both forms address the issue of compliance with IRS regulations regarding reporting income and avoiding penalties.

The P-1 form also shares similarities with the IRS Form 4506-T, which is a request for a transcript of tax return information. While the P-1 focuses on the identification number of the payee, the 4506-T allows individuals to verify their tax information. Both forms require signatures and affirmations of the truthfulness of the information provided. They are used in different contexts but both aim to ensure accurate reporting and compliance with tax laws.

Lastly, the P-1 form is akin to the Form 941, which is the employer's quarterly federal tax return. This form reports wages paid and taxes withheld, and it also requires accurate employee identification information. If an employer cannot obtain the necessary identifying numbers from employees, they may face penalties, similar to the situation outlined in the P-1 form. Both documents emphasize the importance of accurate record-keeping and compliance with IRS requirements, highlighting the responsibilities of the payor in obtaining necessary information.

When filling out the P-1 form, it’s important to follow guidelines to ensure accuracy and compliance. Here are seven key dos and don’ts:

By adhering to these guidelines, you can help facilitate a smoother process and avoid potential penalties.

Misconceptions about the P-1 form can lead to confusion and mismanagement. Here are nine common misunderstandings clarified:

Understanding these misconceptions is crucial for both employers and payees to navigate the requirements surrounding the P-1 form effectively.

Filling out the P 1 form correctly is crucial for both employers and payees. Here are some key takeaways to keep in mind: