When it comes to borrowing money in Oregon, a Promissory Note serves as a vital tool for both lenders and borrowers. This written agreement outlines the borrower's promise to repay a specific amount of money to the lender, typically with interest, within a designated timeframe. The form includes essential details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. Additionally, it may specify whether the loan is secured or unsecured, providing clarity on the borrower's obligations. Understanding the Oregon Promissory Note is crucial for anyone involved in lending or borrowing, as it lays the foundation for a clear and legally binding agreement. By utilizing this form, parties can ensure that their financial arrangements are documented properly, minimizing potential disputes down the line.

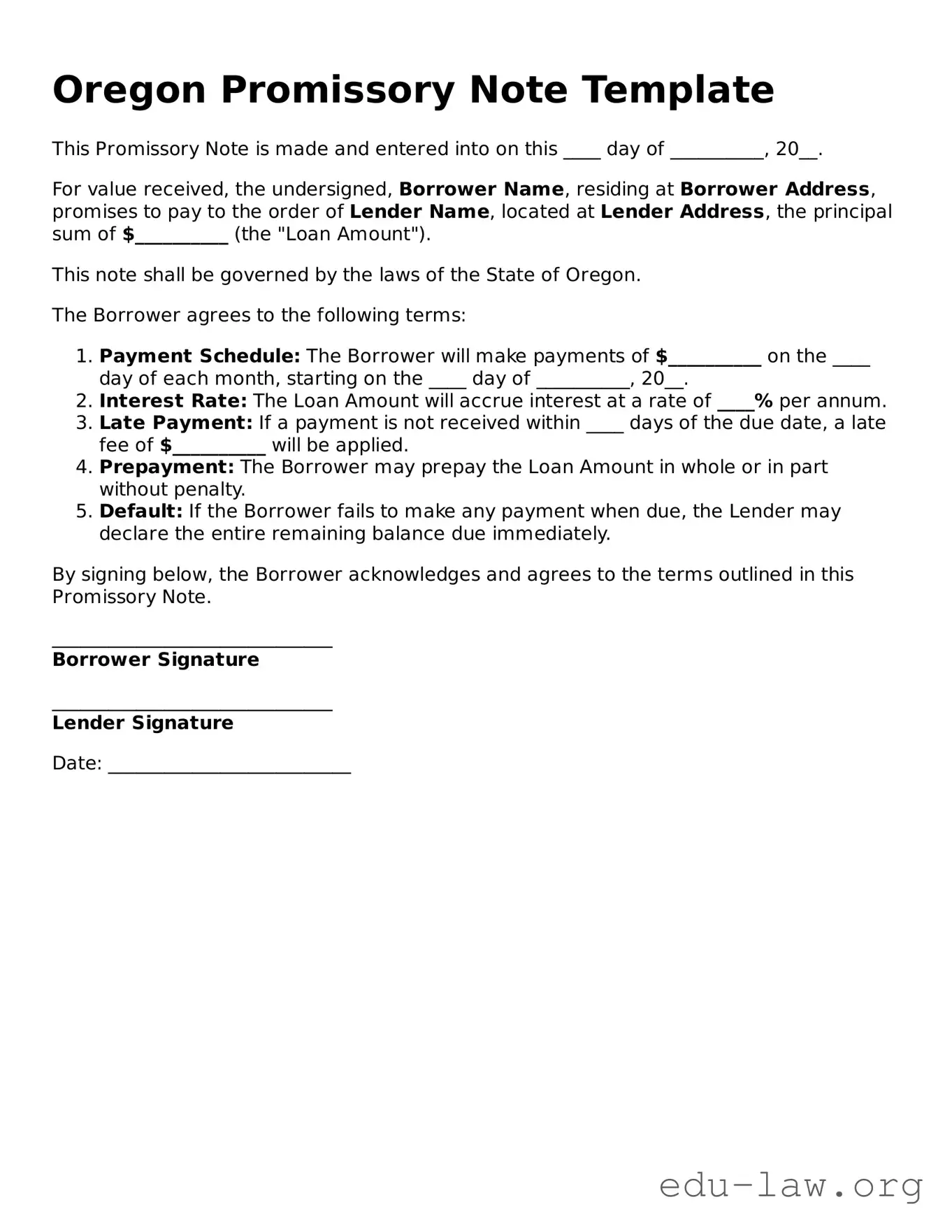

Oregon Promissory Note Template

This Promissory Note is made and entered into on this ____ day of __________, 20__.

For value received, the undersigned, Borrower Name, residing at Borrower Address, promises to pay to the order of Lender Name, located at Lender Address, the principal sum of $__________ (the "Loan Amount").

This note shall be governed by the laws of the State of Oregon.

The Borrower agrees to the following terms:

By signing below, the Borrower acknowledges and agrees to the terms outlined in this Promissory Note.

______________________________

Borrower Signature

______________________________

Lender Signature

Date: __________________________

| Fact Name | Details |

|---|---|

| Definition | An Oregon Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a specified time or on demand. |

| Governing Law | The Oregon Uniform Commercial Code (UCC) governs promissory notes in Oregon, specifically under ORS 73.0101 to 73.0610. |

| Essential Elements | The note must include the principal amount, interest rate, payment terms, and the signatures of the parties involved. |

| Enforceability | For the note to be enforceable, it must be in writing and signed by the borrower. Oral promises are not sufficient. |

After obtaining the Oregon Promissory Note form, you will need to complete it accurately to ensure its validity. Follow the steps outlined below to fill out the form correctly.

What is a promissory note in Oregon?

A promissory note in Oregon is a written agreement where one party promises to pay a specific amount of money to another party at a designated time or on demand. It outlines the terms of the loan, including the principal amount, interest rate, and repayment schedule. This document serves as a legal record of the debt and can be enforced in court if necessary.

Who can use the Oregon Promissory Note form?

Any individual or business can use the Oregon Promissory Note form. It is commonly utilized by lenders and borrowers in various situations, such as personal loans, business loans, or real estate transactions. Both parties should understand the terms before signing to ensure clarity and agreement.

What are the key components of an Oregon Promissory Note?

An effective Oregon Promissory Note typically includes the names and addresses of both the borrower and lender, the loan amount, the interest rate, the repayment schedule, and any late fees or penalties for missed payments. Additionally, it may outline conditions for default and the rights of both parties in such an event.

Is the Oregon Promissory Note form legally binding?

Yes, once signed by both parties, the Oregon Promissory Note is legally binding. This means that if the borrower fails to repay the loan as agreed, the lender has the right to take legal action to recover the owed amount. It is essential for both parties to understand their obligations under the note.

Do I need a witness or notarization for the Oregon Promissory Note?

While notarization is not strictly required for a promissory note in Oregon, having the document notarized can add an extra layer of authenticity and may help in legal proceedings if disputes arise. It is generally a good practice to have a witness or a notary present during the signing.

Can I modify the terms of an existing Oregon Promissory Note?

Yes, the terms of an existing Oregon Promissory Note can be modified, but both parties must agree to the changes. It’s advisable to document any modifications in writing and have both parties sign the amended note. This helps prevent misunderstandings in the future.

What happens if the borrower defaults on the Oregon Promissory Note?

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. They may pursue collection efforts, which could include contacting the borrower for payment, negotiating a new payment plan, or taking legal action to recover the debt. The specific rights and remedies will depend on the terms outlined in the note.

Can a promissory note be transferred or sold?

Yes, a promissory note can be transferred or sold to another party. This process is known as assignment. The original lender can assign their rights to receive payments under the note to another individual or entity. It’s important to notify the borrower of this change to ensure they know where to send future payments.

Where can I find a template for an Oregon Promissory Note?

Templates for Oregon Promissory Notes can be found online through legal websites, financial institutions, or local government resources. It’s crucial to choose a template that complies with Oregon law and meets the specific needs of your situation. Always review the template carefully before use.

What should I do if I have questions about my promissory note?

If you have questions about your promissory note, it’s advisable to consult with a legal professional or a financial advisor. They can provide guidance tailored to your specific situation and help ensure that your rights are protected. Understanding the terms and implications of your note is essential for both parties involved.

Inaccurate Borrower Information: One common mistake is failing to provide complete and accurate information about the borrower. This includes the borrower's full name, address, and contact details. Missing or incorrect information can lead to confusion and complications in the future.

Incorrect Loan Amount: Another frequent error involves stating the wrong loan amount. It's essential to double-check the figures to ensure they match the agreed-upon terms. An incorrect amount can create disputes later on.

Omitting Interest Rate: Some individuals forget to specify the interest rate on the loan. This omission can result in misunderstandings regarding repayment expectations. Always include the interest rate clearly.

Failure to Specify Payment Terms: Not detailing the payment schedule is a significant oversight. Clearly outline when payments are due, how much they will be, and the method of payment. This clarity helps avoid future disputes.

Not Including a Default Clause: A default clause protects the lender in case the borrower fails to make payments. Neglecting to include this clause can leave the lender without clear recourse if issues arise.

Not Signing the Document: It may seem obvious, but many people forget to sign the promissory note. Without a signature, the document is not legally binding, which can lead to complications down the road.

Ignoring Witnesses or Notarization: Depending on the situation, some promissory notes may require witnesses or notarization. Failing to include these elements when necessary can undermine the enforceability of the document.

When working with an Oregon Promissory Note, several other forms and documents may be necessary to ensure a complete and legally sound transaction. Each of these documents serves a specific purpose and helps clarify the terms of the agreement between the parties involved.

Using these documents in conjunction with the Oregon Promissory Note can help protect the interests of both parties and ensure that all aspects of the loan are clearly defined and understood. Proper documentation is key to a smooth lending process.

The Oregon Promissory Note form shares similarities with a Loan Agreement. Both documents outline the terms of a loan between a borrower and a lender. They specify the amount borrowed, the interest rate, and the repayment schedule. A Loan Agreement may also include additional clauses regarding default and remedies, while a Promissory Note focuses primarily on the promise to repay the loan. Both documents serve to protect the interests of the lender and provide clarity for the borrower.

Another document similar to the Oregon Promissory Note is the Mortgage. While a Promissory Note is a promise to pay back borrowed money, a Mortgage secures that promise with property. The borrower pledges their property as collateral for the loan. If the borrower fails to repay, the lender can foreclose on the property. Both documents work together, with the Promissory Note detailing the loan and the Mortgage providing security for the lender.

A Secured Note is also comparable to the Oregon Promissory Note. This document includes a promise to repay a loan, but it is backed by specific assets. In this case, if the borrower defaults, the lender has rights to the specified assets. Like a Promissory Note, a Secured Note outlines the loan amount, interest rate, and repayment terms. The key difference lies in the collateral that secures the loan.

The Demand Note is another document that resembles the Oregon Promissory Note. A Demand Note allows the lender to request repayment at any time. This contrasts with a traditional Promissory Note, which typically has a set repayment schedule. Both documents include the borrower's promise to repay, but the Demand Note offers more flexibility for the lender regarding when they can collect the debt.

The Installment Note is similar as well. This document details a loan that is repaid in regular installments over time. Like the Oregon Promissory Note, it outlines the principal amount, interest rate, and repayment terms. The primary distinction is that an Installment Note breaks down payments into smaller, manageable amounts, making it easier for borrowers to budget their finances.

A Balloon Note is another type of note that bears similarity to the Oregon Promissory Note. In this case, the borrower makes smaller payments over a period, with a large final payment due at the end of the term. This structure can make initial payments more affordable, but it requires the borrower to be prepared for a significant payment later on. Both documents serve to formalize the loan agreement and outline payment expectations.

The Simple Note is also akin to the Oregon Promissory Note. This document is straightforward and includes basic terms of the loan without extensive clauses or conditions. It states the amount borrowed, interest rate, and repayment terms, similar to a Promissory Note. The simplicity of a Simple Note can be appealing for both borrowers and lenders looking for a quick agreement.

Finally, the Personal Guarantee is similar in that it provides an assurance for the lender regarding repayment. While not a loan document itself, it often accompanies a Promissory Note when a third party agrees to be responsible for the loan if the borrower defaults. This adds an extra layer of security for the lender, ensuring that they have recourse if the primary borrower fails to meet their obligations.

When filling out the Oregon Promissory Note form, it is important to approach the process with care. Below are some guidelines to help ensure that the form is completed accurately.

By following these guidelines, you can help ensure that the Oregon Promissory Note form is completed correctly and effectively. Taking the time to be thorough can prevent misunderstandings and legal issues in the future.

Understanding the Oregon Promissory Note form is essential for both lenders and borrowers. However, several misconceptions can lead to confusion. Below are four common misconceptions and their clarifications.

In Oregon, a promissory note does not require notarization to be legally binding. While having a notary can provide an extra layer of verification, the absence of a notary does not invalidate the document.

Promissory notes can vary significantly in terms of terms and conditions. Each note should be tailored to the specific agreement between the lender and borrower, including details such as interest rates, repayment schedules, and consequences for default.

While verbal agreements can be legally binding, they are difficult to enforce. A written promissory note provides clear evidence of the terms agreed upon, which can protect both parties in case of disputes.

Promissory notes can be used for loans of any size. Whether the loan amount is large or small, having a written agreement ensures clarity and accountability for both the lender and the borrower.

When filling out and using the Oregon Promissory Note form, keep the following key takeaways in mind:

These steps will help ensure clarity and enforceability in your lending agreement.