The North Carolina Promissory Note form serves as a crucial financial instrument for individuals and businesses alike. This legally binding document outlines the terms under which one party agrees to pay a specified sum of money to another party at a defined future date or upon demand. Key elements of the form include the principal amount, interest rate, payment schedule, and any applicable fees or penalties for late payments. Additionally, it specifies the rights and obligations of both the borrower and the lender, ensuring that all parties are aware of their responsibilities. The form may also include provisions for default, allowing the lender to take appropriate actions if the borrower fails to meet the agreed-upon terms. By utilizing this form, parties can establish clear expectations and protect their interests in financial transactions.

North Carolina Promissory Note Template

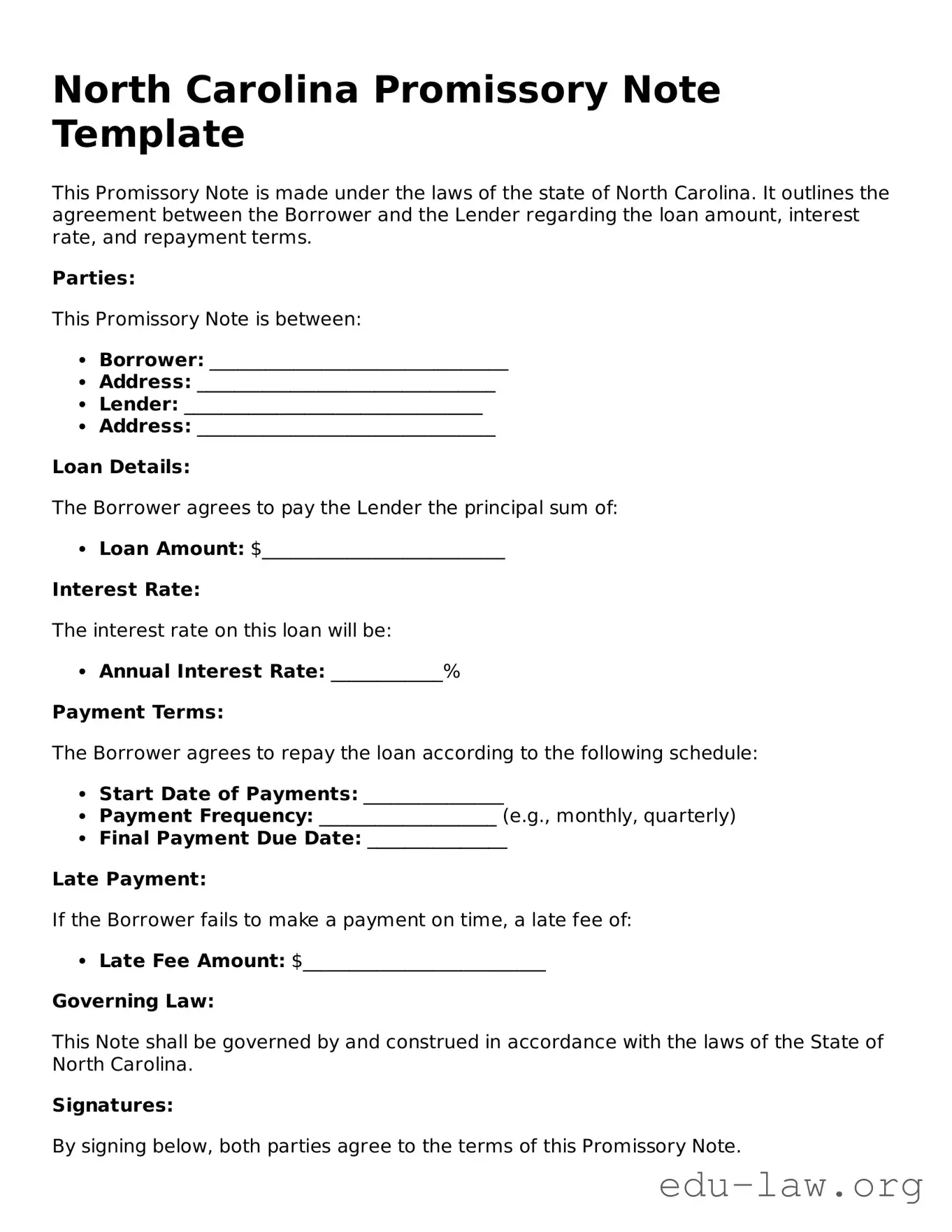

This Promissory Note is made under the laws of the state of North Carolina. It outlines the agreement between the Borrower and the Lender regarding the loan amount, interest rate, and repayment terms.

Parties:

This Promissory Note is between:

Loan Details:

The Borrower agrees to pay the Lender the principal sum of:

Interest Rate:

The interest rate on this loan will be:

Payment Terms:

The Borrower agrees to repay the loan according to the following schedule:

Late Payment:

If the Borrower fails to make a payment on time, a late fee of:

Governing Law:

This Note shall be governed by and construed in accordance with the laws of the State of North Carolina.

Signatures:

By signing below, both parties agree to the terms of this Promissory Note.

| Fact Name | Details |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a specific time. |

| Governing Law | The North Carolina Promissory Note is governed by the North Carolina General Statutes, specifically Chapter 25. |

| Parties Involved | Typically, there are two parties: the maker (borrower) and the payee (lender). |

| Interest Rate | The note may specify an interest rate, which must comply with North Carolina's usury laws. |

| Payment Terms | Payment terms, including due dates and installment amounts, should be clearly outlined in the note. |

| Default Provisions | Provisions regarding default and remedies available to the payee should be included to protect their interests. |

| Signatures | The document must be signed by the maker to be enforceable, and it is advisable for the payee to sign as well. |

After gathering the necessary information, you are ready to fill out the North Carolina Promissory Note form. This document will outline the terms of the loan agreement between the borrower and the lender. Make sure you have all relevant details handy to ensure a smooth process.

Once you have completed the form, review it carefully for accuracy. Both parties should keep a copy for their records. This will help ensure that everyone is clear on the terms of the agreement moving forward.

What is a North Carolina Promissory Note?

A North Carolina Promissory Note is a legal document that outlines a borrower's promise to repay a specific amount of money to a lender. This note includes details such as the loan amount, interest rate, repayment schedule, and any consequences for defaulting on the loan. It serves as a record of the transaction and can be enforced in court if necessary.

What are the key components of a Promissory Note?

Essential components of a Promissory Note include the names of the borrower and lender, the principal amount, the interest rate, the repayment terms, and any late fees or penalties. It’s also important to specify the date of the loan and the maturity date when the loan must be repaid in full. Clear terms help prevent misunderstandings between both parties.

Do I need to have the Promissory Note notarized?

While notarization is not strictly required for a Promissory Note in North Carolina, it is highly recommended. Having the document notarized adds an extra layer of authenticity and can help prove the validity of the agreement in case of disputes. It can also enhance the enforceability of the note in court.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended agreement. This helps maintain clarity and protects the interests of both the borrower and the lender.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has several options. They may choose to negotiate a new repayment plan or pursue legal action to recover the owed amount. The terms of the Promissory Note should outline the actions the lender can take in the event of default, including any fees or penalties that may apply. It's crucial for both parties to understand these terms before signing.

Failing to include the borrower's full name. It is crucial to provide the complete legal name to avoid confusion or disputes later.

Not specifying the loan amount clearly. Ensure that the amount is written both in numbers and words to eliminate any ambiguity.

Omitting the interest rate. If the loan involves interest, it must be explicitly stated. This detail is vital for understanding repayment obligations.

Ignoring the repayment schedule. Outline when payments are due and the total duration of the loan. This helps both parties stay on track.

Not signing the document. Both the borrower and lender must sign the note to make it legally binding. A missing signature can render the agreement unenforceable.

Failing to keep copies. After filling out the form, both parties should retain a signed copy for their records. This ensures that everyone has access to the terms agreed upon.

When dealing with a North Carolina Promissory Note, several other documents may come into play to ensure that the transaction is clear and legally binding. These forms help outline the terms, conditions, and responsibilities of the parties involved. Below is a list of commonly used documents alongside the Promissory Note.

Using these documents in conjunction with the North Carolina Promissory Note can help ensure a smooth lending process. They provide clarity and protection for both lenders and borrowers, making it easier to navigate the complexities of financial agreements.

A loan agreement is a document that outlines the terms of a loan between a lender and a borrower. Like a promissory note, it includes details such as the loan amount, interest rate, repayment schedule, and any collateral involved. Both documents serve to establish the borrower's obligation to repay the loan, though a loan agreement may contain more comprehensive terms and conditions, including default clauses and remedies available to the lender.

A mortgage is another document that shares similarities with a promissory note. It secures a loan used to purchase real estate. The promissory note represents the borrower's promise to repay the loan, while the mortgage serves as a legal claim against the property. Both documents work together to protect the lender's interests, ensuring that the borrower adheres to the repayment terms.

A secured note is akin to a promissory note but includes specific collateral to back the loan. If the borrower defaults, the lender can claim the collateral. This document provides additional security for the lender compared to an unsecured promissory note, which does not have collateral backing. Both documents detail the borrower's repayment obligations and the consequences of default.

An unsecured note is a type of promissory note that does not involve any collateral. While it still outlines the borrower's promise to repay the loan, it carries a higher risk for the lender. The lack of security means that if the borrower defaults, the lender may have limited options for recovery. Both unsecured notes and promissory notes emphasize the importance of repayment terms and conditions.

A personal guarantee is a document that can accompany a promissory note, especially in business loans. It involves a third party agreeing to take responsibility for the loan if the primary borrower defaults. While a promissory note focuses on the borrower's obligation, a personal guarantee adds an additional layer of security for the lender, similar to how a co-signer would function in a loan agreement.

An installment agreement is similar to a promissory note in that it outlines a repayment plan for a loan. It specifies the amount to be paid in regular intervals until the debt is fully repaid. Both documents detail the payment schedule, but an installment agreement may also include terms related to late payments and penalties, providing a more structured approach to repayment.

A lease agreement, particularly in the context of a lease-to-own arrangement, can resemble a promissory note. In such cases, the lease outlines payments made for the use of property, with the option to purchase at the end of the lease term. While the primary focus of a lease agreement is on the rental terms, it may incorporate elements similar to a promissory note, particularly regarding payment obligations and potential penalties for non-payment.

When filling out the North Carolina Promissory Note form, it’s important to follow certain guidelines to ensure accuracy and legality. Here’s a list of things you should and shouldn’t do:

Understanding the North Carolina Promissory Note form can be challenging. Here are five common misconceptions about this document, along with explanations to clarify them.

This is incorrect. A promissory note is a specific type of document that outlines a borrower's promise to repay a loan. A loan agreement, on the other hand, includes additional terms and conditions related to the loan, such as interest rates, repayment schedules, and collateral.

Notarization is not a requirement for a promissory note to be legally binding in North Carolina. While notarization can add an extra layer of authenticity, the note is valid as long as it is signed by the borrower and lender.

This is false. Individuals and businesses can also issue promissory notes. Anyone who lends money can create a promissory note to document the terms of the loan.

While it is possible to create a promissory note without a specified repayment schedule, it is not advisable. Clearly outlining when and how the loan will be repaid helps avoid confusion and disputes in the future.

This is incorrect. A properly executed promissory note is legally enforceable in court. If the borrower fails to repay the loan as agreed, the lender can take legal action to recover the owed amount.

When filling out and using the North Carolina Promissory Note form, consider the following key takeaways:

By following these key points, individuals can effectively navigate the process of creating and utilizing a promissory note in North Carolina.