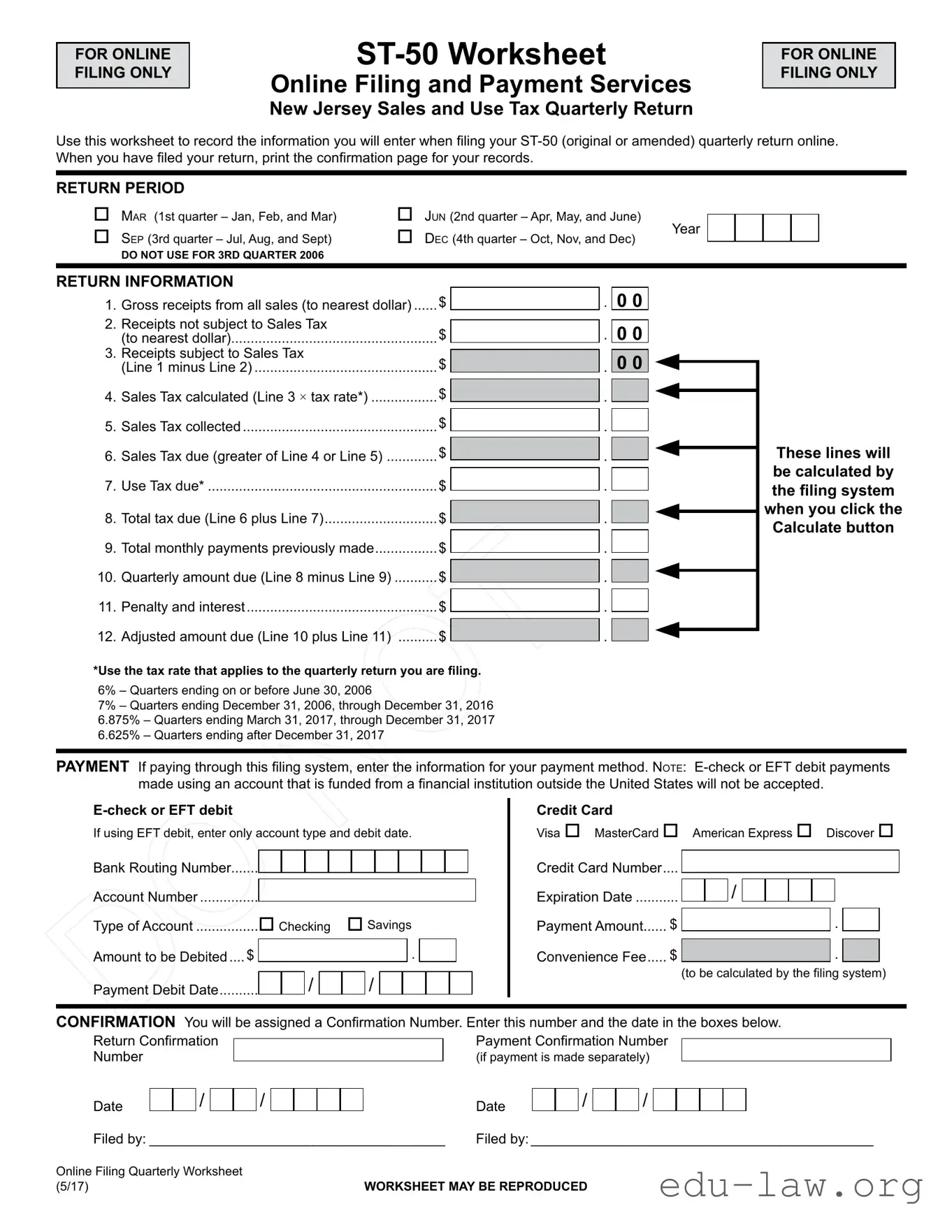

The New Jersey Sales Tax ST-50 form is essential for businesses to report their sales and use tax obligations on a quarterly basis. This form is specifically designed for online filing, streamlining the process for taxpayers. The ST-50 worksheet assists users in organizing their financial data, including gross receipts, taxable and non-taxable sales, and calculated sales tax. It also provides a section for reporting use tax due, if applicable. Taxpayers must indicate the return period, which can range from the first quarter of the year to the fourth. The form requires users to input various figures, such as total sales and tax collected, and it automatically calculates the total tax due and any penalties or interest that may apply. Additionally, payment options include electronic check and credit card, with clear instructions for entering payment information. After submission, a confirmation number is generated for record-keeping purposes, ensuring that businesses can easily track their filings.

FOR ONLINE FILING ONLY

Online Filing and Payment Services

New Jersey Sales and Use Tax Quarterly Return

FOR ONLINE FILING ONLY

Use this worksheet to record the information you will enter when filing your

RETURN PERIOD

|

Mar (1st quarter – Jan, Feb, and Mar) |

|

Sep (3rd quarter – Jul, Aug, and Sept) |

|

|

|

DO NOT USE FOR 3RD QUARTER 2006 |

|

Jun (2nd quarter – Apr, May, and June) |

Year |

|

Dec (4th quarter – Oct, Nov, and Dec) |

||

|

RETURN INFORMATION

1. |

Gross receipts from all sales (to nearest dollar) |

$ |

2. |

Receipts not subject to Sales Tax |

$ |

|

(to nearest dollar) |

|

3. |

Receipts subject to Sales Tax |

$ |

|

(Line 1 minus Line 2) |

|

4. |

Sales Tax calculated (Line 3 × tax rate*) |

$ |

5. |

Sales Tax collected |

$ |

6. |

Sales Tax due (greater of Line 4 or Line 5) |

$ |

7. |

Use Tax due* |

$ |

8. |

Total tax due (Line 6 plus Line 7) |

$ |

9. |

Total monthly payments previously made |

$ |

10. |

Quarterly amount due (Line 8 minus Line 9) |

$ |

11. |

Penalty and interest |

$ |

12. |

Adjusted amount due (Line 10 plus Line 11) |

$ |

. 0 0

. 0 0

. 0 0

.

.

.

.

.

.

.

.

.

These lines will be calculated by the filing system when you click the Calculate button

*Use the tax rate that applies to the quarterly return you are filing.

6% – Quarters ending on or before June 30, 2006

7% – Quarters ending December 31, 2006, through December 31, 2016 6.875% – Quarters ending March 31, 2017, through December 31, 2017 6.625% – Quarters ending after December 31, 2017

PAYMENT If paying through this filing system, enter the information for your payment method. Note:

If using EFT debit, enter only account type and debit date.

Bank Routing Number.......

Account Number................

Type of Account |

Checking |

Savings |

||||||||||||

Amount to be Debited..... $ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

Payment Debit Date |

|

/ |

|

|

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Credit Card

Visa MasterCard American Express Discover

Credit Card Number.... |

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

|

|

|

|

|

|

|

|

|

Expiration Date |

|

|

|

|

|

|

|

|

|

|

|

Payment Amount...... $ |

|

|

|

|

|||||||

|

. |

|

|

||||||||

Convenience Fee..... $ |

|

|

|

||||||||

|

|

|

|

|

|

|

. |

|

|

||

|

(to be calculated by the filing system) |

||||||||||

CONFIRMATION You will be assigned a Confirmation Number. Enter this number and the date in the boxes below.

Return Confirmation Number

Date/

/

Payment Confirmation Number

(if payment is made separately)

Date |

|

|

/ |

|

|

/ |

Filed by:_______________________________________ Filed by:_____________________________________________

Online Filing Quarterly Worksheet |

WORKSHEET MAY BE REPRODUCED |

(5/17) |

| Fact Name | Description |

|---|---|

| Purpose | The ST-50 form is designed for online filing of New Jersey's Sales and Use Tax quarterly return. |

| Filing Periods | It covers four quarterly periods: January-March, April-June, July-September, and October-December. |

| Tax Rates | The applicable sales tax rates vary by quarter: 6% for periods ending on or before June 30, 2006; 7% for periods ending December 31, 2006, through December 31, 2016; 6.875% for periods ending March 31, 2017, through December 31, 2017; and 6.625% for periods after December 31, 2017. |

| Payment Methods | Payments can be made via E-check, EFT debit, or credit card, but certain restrictions apply to international accounts. |

| Governing Law | This form is governed by New Jersey's Sales and Use Tax Act, N.J.S.A. 54:32B-1 et seq. |

Filling out the New Jersey Sales Tax ST-50 form is a straightforward process. This form is essential for reporting your sales and use tax obligations for a specific quarter. After completing the form, you will submit it online and receive a confirmation page to keep for your records.

What is the NJ Sales Tax ST-50 form?

The NJ Sales Tax ST-50 form is a quarterly return used by businesses in New Jersey to report and pay sales and use tax. This form is specifically designed for online filing, allowing businesses to conveniently submit their tax information electronically.

Who needs to file the ST-50 form?

Any business that sells taxable goods or services in New Jersey must file the ST-50 form. This includes retailers, wholesalers, and service providers. If your business collects sales tax from customers, you are required to file this form each quarter.

How often do I need to file the ST-50 form?

The ST-50 form must be filed quarterly. The filing periods are divided into four quarters: January to March, April to June, July to September, and October to December. Each quarter has its own deadline for submission.

What information do I need to complete the ST-50 form?

You will need to provide gross receipts from all sales, receipts not subject to sales tax, and receipts subject to sales tax. Additionally, you will calculate the sales tax due based on the applicable tax rate for the quarter you are filing. Other information includes previous payments made, penalties, and interest, if applicable.

How do I calculate the sales tax due on the ST-50 form?

To calculate the sales tax due, subtract the receipts not subject to sales tax from your gross receipts to find the taxable amount. Then, multiply this amount by the applicable tax rate for the quarter. The greater of the calculated tax or the tax collected should be reported as the sales tax due.

What payment methods are accepted for the ST-50 form?

You can pay online using either an e-check or a credit card. If using an e-check, ensure that your bank account is based in the United States, as international accounts are not accepted. Credit card payments can be made with major credit cards, including Visa, MasterCard, American Express, and Discover.

What happens if I file my ST-50 form late?

If you file your ST-50 form late, you may incur penalties and interest on the amount due. It is essential to file on time to avoid additional charges. The form includes lines to report any penalties and interest that may apply.

Can I amend my ST-50 form after filing?

Yes, you can amend your ST-50 form if you discover an error after submission. The online filing system allows you to file an amended return. Make sure to provide the correct information and any additional tax due, if applicable.

How can I confirm that my ST-50 form has been filed successfully?

After filing your ST-50 form online, you will receive a confirmation number. It is important to print or save this confirmation page for your records. This number serves as proof of your filing and can be used for any future inquiries regarding your submission.

Incorrect Selection of Return Period: Failing to select the correct quarter can lead to filing errors. Ensure you choose the appropriate option for the period you are reporting.

Inaccurate Gross Receipts: Reporting gross receipts without rounding to the nearest dollar can result in discrepancies. Always round figures correctly.

Omitting Non-Taxable Receipts: Neglecting to report receipts that are not subject to sales tax can inflate your taxable amount. Be thorough in distinguishing between taxable and non-taxable sales.

Incorrect Tax Rate Application: Using the wrong tax rate for the period can lead to underpayment or overpayment of taxes. Verify the applicable rate for your filing period.

Failure to Include All Tax Types: Not accounting for both sales tax and use tax can result in an incomplete return. Ensure both are calculated and reported.

Not Keeping Payment Records: Forgetting to document your confirmation number and payment details can complicate future inquiries. Always save this information for your records.

Ignoring Penalties and Interest: Overlooking potential penalties or interest on late payments can increase your total amount due. Be proactive in addressing any outstanding fees.

When filing the New Jersey Sales Tax ST-50 form, there are several other documents that may be necessary to ensure compliance and accuracy in reporting. Each of these forms serves a specific purpose and can help streamline the filing process. Below is a list of commonly used documents that accompany the ST-50 form.

Understanding these forms and how they relate to the ST-50 can help businesses maintain compliance and avoid potential penalties. Keeping thorough records and utilizing the appropriate documentation ensures a smoother filing experience and helps clarify tax obligations.

The New Jersey Sales Tax ST-50 form serves as a critical tool for businesses to report their sales tax obligations. A document that shares similarities with the ST-50 is the IRS Form 1040. While the ST-50 focuses on sales and use tax for businesses, Form 1040 is utilized by individuals to report their annual income tax. Both forms require detailed financial information, including gross receipts or income, and both ultimately determine the tax liability owed. The process of filing these forms is essential for compliance with tax laws, and both forms allow for online submission, making it easier for taxpayers to fulfill their obligations.

Another document comparable to the ST-50 is the New Jersey Corporation Business Tax (CBT) return. Similar to the ST-50, the CBT return requires businesses to report their financial activities over a specified period. Both forms calculate the amount of tax owed based on reported figures, such as gross receipts. Additionally, both documents can be filed online, streamlining the process for businesses. The CBT return, however, is specifically for corporations, while the ST-50 is for sales tax, reflecting the different types of tax responsibilities that businesses may encounter.

The New Jersey Gross Income Tax return is another document that bears resemblance to the ST-50. While the ST-50 pertains to sales tax, the Gross Income Tax return is focused on income earned by individuals and businesses. Both forms necessitate the reporting of financial data to determine tax liabilities. They also include provisions for calculating deductions or exemptions, which can affect the final tax owed. Just as with the ST-50, these forms can be filed online, ensuring that taxpayers can easily manage their tax responsibilities.

The New Jersey Employer Payroll Tax return also shares similarities with the ST-50. This document is used by employers to report wages paid to employees and the corresponding payroll taxes owed. Like the ST-50, the Employer Payroll Tax return requires accurate reporting of financial information to ensure compliance with tax laws. Both forms are essential for maintaining proper tax records and can be filed online, facilitating the process for businesses. Each form plays a vital role in the overall tax system, highlighting the various responsibilities businesses have regarding taxation.

The New Jersey Sales Tax Exempt Certificate is another relevant document. While the ST-50 is used to report sales tax collected, the Exempt Certificate is utilized by purchasers to claim exemption from sales tax on eligible purchases. Both documents are integral to the sales tax process in New Jersey. They require accurate information and can impact the amount of tax owed or collected. Understanding the relationship between these two forms is essential for businesses to navigate sales tax compliance effectively.

The IRS Form 941, which reports payroll taxes withheld from employee wages, is another document akin to the ST-50. Both forms require businesses to report financial information periodically. While the ST-50 focuses on sales tax, Form 941 addresses federal payroll taxes. Each form is crucial for ensuring compliance with tax regulations, and both can be filed electronically, making it easier for businesses to meet their obligations. Understanding the nuances of these forms helps businesses maintain compliance and avoid penalties.

The New Jersey Use Tax Return is also similar to the ST-50, as both pertain to tax obligations related to sales. The Use Tax Return is filed by individuals or businesses that purchase goods out-of-state and do not pay sales tax at the time of purchase. Both forms require detailed reporting of financial transactions and the calculation of tax owed. They serve to ensure that all sales-related tax obligations are met, reinforcing the importance of accurate record-keeping in tax compliance.

Lastly, the New Jersey Annual Report for Corporations resembles the ST-50 in that it requires businesses to disclose financial information periodically. While the ST-50 focuses on sales and use tax, the Annual Report provides a broader overview of a corporation's financial status. Both documents are essential for maintaining compliance with state regulations and can be filed online, reflecting the evolving nature of tax reporting in the digital age. Understanding the similarities and differences between these forms is crucial for businesses to navigate their tax responsibilities effectively.

When filling out the New Jersey Sales Tax ST-50 form, there are several important things to keep in mind. Here’s a helpful list of dos and don’ts to ensure a smooth filing process.

By following these guidelines, you can help ensure that your ST-50 form is filled out correctly and submitted without issues. Good luck with your filing!

Understanding the New Jersey Sales Tax ST-50 form is essential for accurate filing. However, several misconceptions exist about this form. Below is a list of common misunderstandings.

Addressing these misconceptions can help ensure that all parties understand their responsibilities and rights when it comes to filing the New Jersey Sales Tax ST-50 form.

When filling out the New Jersey Sales Tax ST-50 form, consider the following key takeaways: