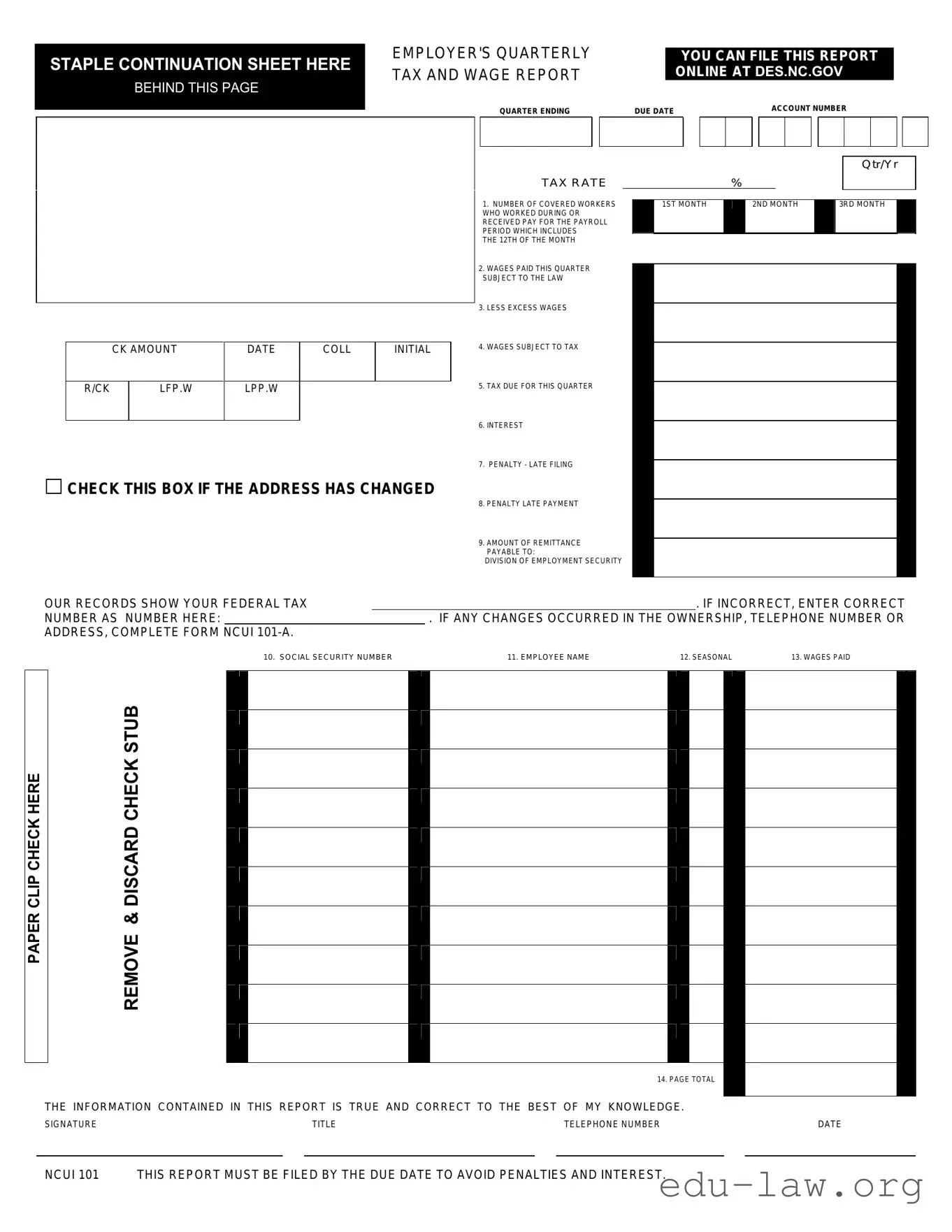

The NCUI 101 form is a crucial document for employers in North Carolina, serving as the Employer's Quarterly Tax and Wage Report. This form must be completed and submitted by the due date to avoid penalties and interest. It encompasses several key components that provide a comprehensive overview of an employer's payroll activities for the quarter. Employers must report the number of covered workers who received pay during the payroll period, as well as the total wages paid to all employees, including part-time and temporary staff. The form also requires details on excess wages, wages subject to tax, and the calculated tax due for the quarter. Additionally, it includes provisions for penalties related to late filing and payment, ensuring that employers are aware of their obligations. Accurate reporting is essential, as incorrect information can lead to complications with tax liabilities. The NCUI 101 form also allows for updates on ownership changes and provides space for reporting Social Security numbers and employee names. By adhering to the guidelines set forth in this form, employers can maintain compliance with state regulations while effectively managing their payroll responsibilities.

STAPLE CONTINUATION SHEET HERE

BEHIND THIS PAGE

EMPLOYER'S QUARTERLY TAX AND WAGE REPORT

QUARTER ENDING

TAX RATE

YOU CAN FILE THIS REPORT ONLINE AT DES.NC.GOV

DUE DATE |

|

|

|

ACCOUNT NUMBER |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Qtr/Yr

%

1. NUMBER OF COVERED WORKERS |

1ST MONTH |

2ND MONTH |

3RD MONTH |

WHO WORKED DURING OR |

|

|

|

RECEIVED PAY FOR THE PAYROLL |

|

|

|

PERIOD WHICH INCLUDES |

|

|

|

THE 12TH OF THE MONTH |

|

|

|

|

CK AMOUNT |

DATE |

COLL |

INITIAL |

R/CK |

LFP.W |

LPP.W |

|

|

CHECK THIS BOX IF THE ADDRESS HAS CHANGED

2.WAGES PAID THIS QUARTER SUBJECT TO THE LAW

3.LESS EXCESS WAGES

4.WAGES SUBJECT TO TAX

5.TAX DUE FOR THIS QUARTER

6.INTEREST

7.PENALTY - LATE FILING

8.PENALTY LATE PAYMENT

9.AMOUNT OF REMITTANCE PAYABLE TO:

DIVISION OF EMPLOYMENT SECURITY

OUR RECORDS SHOW YOUR FEDERAL TAX |

|

|

. IF INCORRECT, ENTER CORRECT |

|

NUMBER AS NUMBER HERE: |

|

. IF ANY CHANGES OCCURRED IN THE OWNERSHIP, TELEPHONE NUMBER OR |

||

ADDRESS, COMPLETE FORM |

NCUI |

|

|

|

CLIP CHECK HERE |

DISCARD CHECK STUB |

PAPER |

REMOVE & |

|

|

10. SOCIAL SECURITY NUMBER |

11. EMPLOYEE NAME |

12. SEASONAL |

13. WAGES PAID |

|

|

14. PAGE TOTAL |

|

THE INFORMATION CONTAINED IN THIS REPORT IS TRUE AND CORRECT TO THE BEST OF MY KNOWLEDGE.

SIGNATURE |

TITLE |

TELEPHONE NUMBER |

DATE |

NCUI 101 THIS REPORT MUST BE FILED BY THE DUE DATE TO AVOID PENALTIES AND INTEREST.

INSTRUCTIONS FOR COMPLETING FORM NCUI 101, EMPLOYER'S QUARTERLY TAX AND WAGE REPORT

ITEM 1: For each month in the calendar quarter, enter the number of all

ITEM 2: Enter all wages paid to all employees, including

(A)CORPORATION, the wages paid to all employees who performed services in North Carolina should be reported. Corporate officers are employees and their wages and/or draws are reportable.

(B)A PARTNERSHIP, the draws or payments made to general partners should not be reported.

(C)A PROPRIETORSHIP, the draws or payments made to the legal owner of the business (the proprietor) should not be reported. Wage paid to the children of the proprietor under the age of 21 years, as well as wages paid to the spouse or parents of the proprietor, should not be reported.

Special payments given in return for services performed, I.E., commissions, bonuses, fees, prizes, are wages and reportable under the Employment Security Law of North Carolina. These payments (or dollar value of the gifts/prizes) are to be included in the payroll of each employee by the employer for the calendar quarter(s) in which they are given.

If no wages were paid, enter NONE.

ITEM 3: Enter the amount of wages paid during this quarter that is in excess of the applicable North Carolina taxable wage base. This entry cannot be more than item 2.

Example: An employer using the 2012 taxable wage base of $20,400 and reporting one employee, John Doe, earning $6,000 per quarter.

1ST QTR 2ND QTR 3RD QTR 4TH QTR

ITEM 2: |

$6,000.00 |

$6,000.00 |

$6,000.00 |

$6,000.00 |

ITEM 3: |

$3,600.00 |

|||

ITEM 4: |

$6,000.00 |

$6,000.00 |

$6,000.00 |

$2,400.00 |

ITEM 4: Subtract Item 3 from Item 2. THE RESULTS CANNOT BE A NEGATIVE AMOUNT.

ITEM 5: Multiply Item 4 by the tax rate shown on the face of this report. (Example: .012% = .00012) If the tax due is less than $5.00, you do not have to

pay it, but you must file a report.

NOTE: ITEMS 6,7, AND 8 MUST BE COMPUTED ONLY IF THE REPORT IS NOT FILED (POSTMARKED) BY THE DUE DATE.

ITEM 6: Multiply the tax due (Item 5) by the current interest rate for each month, or fraction thereof, past the due date. The applicable interest rate may be obtained at des.nc.gov or by contacting the nearest Division of Employment Security Office.

ITEM 7: Multiply the tax due (Item 5) by 5% (.05) for each month, or fraction thereof, past the due date. The maximum late filing penalty is 25% (.25).

ITEM 8: Multiply the tax due (Item 5) by 10% (.1). The minimum late payment penalty is $5.00.

ITEM 9: Enter the sum of Items 5, 6, 7 and 8. Remittance should be made payable to the Division of Employment Security.

IF YOUR FEDERAL IDENTIFICATION NUMBER AS PRINTED ON THE REPORT IS INCORRECT, ENTER THE CORRECT NUMBER IN THE SPACE PROVIDED. STATE TAX CREDITS WILL BE REPORTED TO THE INTERNAL REVENUE SERVICE USING THIS NUMBER. IF YOUR FEDERAL IDENTIFICATION NUMBER IS NOT PREPRINTED; ENTER IT IN THIS SPACE.

ITEM 10: Enter the federal Social Security number of every worker whose wages are reported on this form.

ITEM 11: Enter the name of every worker whose wages are reported on his form. If the last name is listed first, it must be followed by a comma.

ITEM 12: Enter an 'S' in this space if the wages reported are seasonal, otherwise leave this space blank. To report seasonal wages you must have

been determined a seasonal pursuit by this agency.

ITEM 13: Wages are reportable in the quarter paid to the employee, regardless of when the wages were earned. Enter each worker's total quarterly

wages paid, whether or not the worker has exceeded the taxable wage base for this year. Do not show credit or minus amounts to adjust for

ITEM 14: Enter the sum of wages shown in Item 13 for this page only. The sum of the page totals of all pages must equal the amount shown in Item 2.

Additional information is available at: des.nc.gov

| Fact Name | Fact Details |

|---|---|

| Purpose | The NCUI 101 form is used for reporting employer's quarterly tax and wage information in North Carolina. |

| Filing Deadline | This report must be filed by the due date to avoid penalties and interest. |

| Applicable Law | The form is governed by the Employment Security Law of North Carolina. |

| Online Filing | Employers can file the NCUI 101 report online at des.nc.gov. |

Filling out the NCUI 101 form is an essential step for employers to report their quarterly tax and wage information accurately. Once completed, the form should be submitted by the due date to avoid any penalties or interest. Here’s a straightforward guide to help you fill out the form correctly.

What is the purpose of the NCUI 101 form?

The NCUI 101 form serves as the Employer's Quarterly Tax and Wage Report in North Carolina. Employers use this form to report wages paid to employees, the number of workers, and the taxes owed for unemployment insurance. Filing this report accurately and on time is crucial to avoid penalties and ensure compliance with state laws regarding employment security.

Who needs to file the NCUI 101 form?

Any employer who pays wages to employees in North Carolina must file the NCUI 101 form. This includes corporations, partnerships, and sole proprietorships. Even if no wages were paid during the quarter, a report must still be filed, indicating "NONE" for wages paid. Failure to file can result in penalties and interest charges.

How do I complete the NCUI 101 form correctly?

To fill out the NCUI 101 form, begin by entering the number of covered workers for each month of the quarter. Next, report all wages paid to employees, including part-time and temporary workers. Be mindful of specific rules regarding partnerships and sole proprietorships, as certain payments do not need to be reported. Calculate the wages subject to tax and the tax due, ensuring that no negative amounts are recorded. Lastly, include the necessary information about each employee, such as their Social Security number and total wages paid.

What are the consequences of late filing or payment?

Filing the NCUI 101 form after the due date can lead to penalties and interest charges. The penalties are calculated based on the amount of tax due and the duration of the delay. For example, a late filing incurs a penalty of 5% for each month late, capped at 25%. Additionally, late payment incurs a 10% penalty with a minimum charge of $5.00. Therefore, timely filing and payment are essential to avoid these additional costs.

Where can I find additional information or assistance regarding the NCUI 101 form?

For further guidance on completing the NCUI 101 form, employers can visit the North Carolina Division of Employment Security website at des.nc.gov. The site offers detailed instructions, updates on interest rates, and contact information for local offices where assistance can be obtained. It is advisable to seek help if there are any uncertainties in completing the form to ensure compliance and accuracy.

Incorrect Reporting of Workers: Individuals often fail to accurately count the number of workers who worked or received pay during the payroll period that includes the 12th of the month. This can lead to incorrect entries in Item 1.

Omitting Seasonal Designation: Some people neglect to indicate whether the wages reported are seasonal by not marking the 'S' in Item 12. This can result in misunderstandings about the nature of the employment.

Errors in Wage Reporting: It is common for individuals to misreport wages in Item 2. All wages paid to employees must be included, but some may mistakenly exclude certain payments or miscalculate totals.

Failure to Adjust for Excess Wages: In Item 3, individuals may not accurately report excess wages that exceed the taxable wage base. This can lead to discrepancies in the final tax calculations.

Neglecting to Include Penalties and Interest: Many people forget to calculate and include penalties and interest in Items 6, 7, and 8 if the report is not filed by the due date. This oversight can result in unexpected amounts due.

Incorrect Federal Identification Number: If the federal identification number is incorrect, individuals often fail to enter the correct number in the designated space. This can lead to issues with tax credits and reporting.

Inaccurate Employee Information: Individuals sometimes provide incorrect names or Social Security numbers for employees in Items 10 and 11. This can create complications in record-keeping and compliance.

The NCUI 101 form is an essential document for employers in North Carolina, specifically designed for reporting quarterly tax and wage information. When completing this form, several other documents may also be necessary to ensure compliance with state regulations. Below are four commonly used forms that complement the NCUI 101.

Utilizing these forms in conjunction with the NCUI 101 helps employers maintain compliance with both state and federal regulations. Proper documentation ensures accurate reporting of wages and taxes, minimizing the risk of penalties and interest due to errors or late filings.

The NCUI 101 form is similar to the IRS Form 941, which is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Both forms require employers to provide information about the number of employees and total wages paid during a specific period. While the NCUI 101 focuses on state unemployment tax and wages subject to North Carolina law, Form 941 addresses federal tax obligations. Employers must file both forms quarterly to ensure compliance with tax regulations, albeit for different jurisdictions.

Another document comparable to the NCUI 101 is the IRS Form 940. This form is the Employer’s Annual Federal Unemployment (FUTA) Tax Return. Like the NCUI 101, it requires employers to report wages paid to employees and calculate unemployment taxes owed. While the NCUI 101 is filed quarterly, Form 940 is submitted annually. Both forms serve the purpose of reporting unemployment tax, but they operate under different federal and state guidelines.

The NCUI 101 also resembles the state-specific Employer's Wage Report, which is used in various states to report employee wages for state unemployment insurance purposes. Similar to the NCUI 101, this report requires detailed information about employees, including wages paid and any changes in employment status. Both documents are essential for maintaining compliance with state unemployment laws, ensuring that the correct amount of tax is collected and reported.

Form 1099-MISC is another document that shares similarities with the NCUI 101. This form is used to report payments made to independent contractors and other non-employees. While the NCUI 101 focuses on employee wages and unemployment tax, both forms require accurate reporting of payments made during a specific timeframe. Employers must be diligent in filing both forms to avoid potential penalties, ensuring that all compensation is accurately reported.

The W-2 form is also comparable to the NCUI 101, as it reports wages paid to employees and the taxes withheld from their paychecks. Employers must file both forms to fulfill their reporting obligations. The W-2 provides a summary of an employee's annual earnings and withholdings, while the NCUI 101 focuses on quarterly reporting for state unemployment tax. Both documents are crucial for tax compliance and employee record-keeping.

Lastly, the NCUI 101 is similar to the Quarterly Contribution Report used in other states. This report serves to document employer contributions to state unemployment insurance programs. Like the NCUI 101, it requires employers to report the number of employees and total wages paid during the quarter. Both forms aim to ensure that employers meet their obligations to fund unemployment benefits for workers, although the specific requirements may vary by state.

When filling out the NCUI 101 form, it is crucial to follow specific guidelines to ensure accuracy and compliance. Here is a list of things you should and shouldn't do.

By adhering to these guidelines, you can help ensure a smooth filing process and avoid unnecessary complications. If you have any doubts, consider reaching out for assistance or consulting additional resources.

Understanding the NCUI 101 form is essential for employers in North Carolina. However, several misconceptions can lead to confusion. Here are six common misunderstandings:

By clarifying these misconceptions, employers can ensure they complete the NCUI 101 form accurately and on time, avoiding unnecessary penalties and ensuring compliance with North Carolina employment laws.

Key Takeaways for Filling Out and Using the NCUI 101 Form: