The NC-4 form is an essential document for employees in North Carolina, as it helps determine the correct amount of state income tax to be withheld from your paycheck. This form is crucial for ensuring that you neither underpay nor overpay your taxes throughout the year. When you fill out the NC-4, you'll indicate the number of allowances you wish to claim, which directly affects your withholding rate. If you do not submit this form to your employer, they will default to withholding taxes as if you are single with zero allowances, which may not reflect your actual tax situation. There are different versions of the form, including the NC-4 EZ for those claiming standard deductions and the NC-4 NRA for nonresident aliens. Completing the NC-4 Allowance Worksheet is a key step in this process, as it guides you through determining your allowances based on various factors, such as income adjustments and potential tax credits. If your circumstances change, like a new job or a change in marital status, you must submit a new NC-4 within ten days. Understanding this form can help you manage your finances better and avoid surprises when tax season arrives.

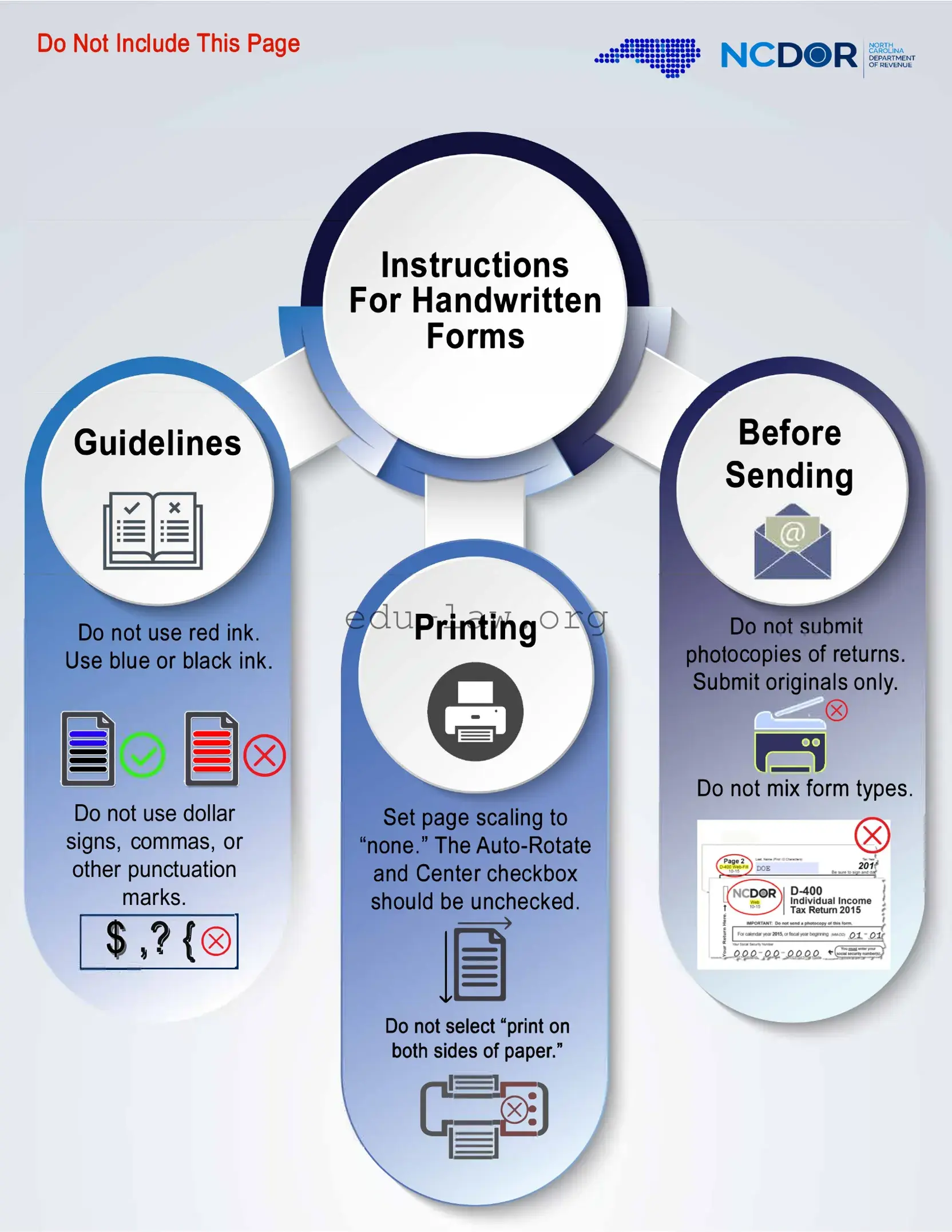

Do Not Include This Page

Guidelines

::::==·

. •• ··=!!!:::!:•

Instructions

For Handwritten

Forms

NCD(i)• R

Before Sending

I NORTH CAROLINA DEPARTMENT OF REVENUE

Do not use red ink. Use blue or black ink.

®

Do not use dollar signs, commas, or other punctuation

marks.

, 1 t®I

Printing

Set page scaling to

"none." The

1�

ocopies of returns. Submit originals only.

,,___(8)

Do not mix form types.

Do not select "print on bothc;sides of paper."

;�1

Web

Employee’s Withholding Allowance Certificate

PURPOSE - Complete Form

FORM

FORM

FORM

including the N.C. Child Deduction Amount, N.C. itemized deductions, and N.C. tax credits. However, you may claim fewer allowances than

you are entitled to if you wish to increase the tax withheld during the tax year. If your withholding allowances decrease, you must file a new

When an individual ceases to be “Head of Household” after maintaining the household for the major portion of the year, a new

TWO OR MORE JOBS - If you have more than one job, determine the total number of allowances you are entitled to claim on all jobs using one Form

“Multiple Jobs Table” to determine the additional amount to be withheld on Line 2 of Form

NONWAGE INCOME - If you have a large amount of nonwage income, such as interest or dividends, you should consider making estimated tax

payments using Form

ncdor.gov.

HEAD OF HOUSEHOLD - Generally you may claim “Head of Household” filing status on your tax return only if you are unmarried and pay more than 50% of the costs of keeping up a home for yourself and your dependent(s)

or other qualifying individuals.

SURVIVING SPOUSE - You may claim “Surviving Spouse” filing status only if your spouse died in either of the two preceding tax years and you meet the following requirements:

1.Your home is maintained as the main household of a child or stepchild for whom you can claim a federal exemption; and

2.You were entitled to file a joint return with your spouse in the year of your spouse’s death.

MARRIED TAXPAYERS - For married taxpayers, both spouses must agree as to whether they will complete the

the filing status, “Married Filing Jointly” or “Married Filing Separately.”

•Married taxpayers who complete the worksheet based on the filing status, “Married Filing Jointly” should consider the sum of both spouses’ income, federal and State adjustments to income, and State tax credits to determine the number of allowances.

•Married taxpayers who complete the worksheet based on the filing status, “Married Filing Separately” should consider only his or her portion of income, federal and State adjustments to income, and State tax credits to determine the number of allowances.

All

CAUTION: If you furnish an employer with an Employee’s Withholding Allowance Certificate that contains information which has no reasonable basis and results in a lesser amount of tax being withheld than would have been withheld had you furnished reasonable information, you are subject to a penalty of 50% of the amount not properly withheld.

Cut here and give this certificate to your employer. Keep the top portion for your records.

WebEmployee’s Withholding Allowance Certificate

1.Total number of allowances you are claiming

(Enter zero (0), or the number of allowances from Page 2, Line 17 of the

2. Additional amount, if any, withheld from each pay period (Enter whole dollars)

,.00

Social Security Number

Filing Status |

|

|

Single or Married Filing Separately |

Head of Household |

Married Filing Jointly or Surviving Spouse |

First Name (USE CAPITAL LETTERS FOR YOUR NAME AND ADDRESS) |

M.I. |

|

|

Last Name |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

County (Enter first five letters) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

State |

Zip Code (5 Digit) |

|

|

Country (If not U.S.) |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employee’s Signature |

Date |

I certify, under penalties provided by law, that I am entitled to the number of withholding allowances claimed on Line 1 above.

|

|

|

|

|

PART I |

||

|

Answer all of the following questions for your filing status. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Single - |

|

|

|

|

|

|

|

1. |

Will your N.C. itemized deductions from Page 3, Schedule 1 exceed $13,249? |

Yes |

o |

No |

o |

|

|

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

|

|

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

|

|

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

|

|

If you answered “No” to all of the above, STOP HERE and enter ZERO (0) as total allowances on Form |

|

|||||

|

If you answered “Yes” to any of the above, you may choose to go to Page 2, Part II to determine if you qualify for |

|

|||||

|

additional allowances. Otherwise, enter ZERO (0) on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Married Filing Jointly - |

|

|

|

|

|

|

|

1. |

Will your N.C. itemized deductions from Page 3, Schedule 1 exceed $23,999? |

Yes |

o |

No |

o |

|

|

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

|

|

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

|

|

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

|

|

5. |

Will your spouse receive combined wages and taxable retirement benefits of |

|

|

|

|

|

|

|

less than $8,250 or only retirement benefits not subject to N.C. income tax? |

Yes |

o |

No |

o |

|

|

If you answered “No” to all of the above, STOP HERE and enter ZERO (0) as total allowances on Form |

|

|||||

|

If you answered “Yes” to any of the above, you may choose to go to Page 2, Part II to determine if you qualify for |

|

|||||

|

additional allowances. Otherwise, enter ZERO (0) on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Married Filing Separately - |

|

|

|

|

|

|

|

1. |

Will your portion of N.C. itemized deductions from Page 3, Schedule 1 exceed $13,249? |

Yes |

o |

No |

o |

|

|

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

|

|

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

|

|

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

|

|

If you answered “No” to all of the above, STOP HERE and enter ZERO (0) as total allowances on Form |

|

|||||

|

If you answered “Yes” to any of the above, you may choose to go to Page 2, Part II to determine if you qualify for |

|

|||||

|

additional allowances. Otherwise, enter ZERO (0) on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Head of Household- |

|

|

|

|

|

|

|

1. |

Will your N.C. itemized deductions from Page 3, Schedule 1 exceed $18,624? |

Yes |

o |

No |

o |

|

|

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

|

|

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

|

|

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

|

|

If you answered “No” to all of the above, STOP HERE and enter ZERO (0) as total allowances on Form |

|

|||||

|

If you answered “Yes” to any of the above, you may choose to go to Page 2, Part II to determine if you qualify for |

|

|||||

|

additional allowances. Otherwise, enter ZERO (0) on Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 1

Surviving Spouse - |

|

|

|

|

|

1. |

Will your N.C. itemized deductions from Page 3, Schedule 1 exceed 23,999? |

Yes |

o |

No |

o |

2. |

Will your N.C. Child Deduction Amount from Page 3, Schedule 2 exceed $2,499? |

Yes |

o |

No |

o |

3. |

Will you have federal adjustments or State deductions from income? |

Yes |

o |

No |

o |

4. |

Will you be able to claim any N.C. tax credits or tax credit carryovers? |

Yes |

o |

No |

o |

If you answered “No” to all of the above, STOP HERE and enter FOUR (4) as total allowances on Form |

|||||

If you answered “Yes” to any of the above, you may choose to go to Part II to determine if you qualify for additional |

|||||

allowances. Otherwise, enter FOUR (4) on Form |

|

|

|

|

|

1. |

Enter your total estimated N.C. itemized deductions from Page 3, Schedule 1 |

..................................................... |

1. |

_______________________$ |

. |

|||

|

|

|

||||||

2. |

Enter the applicable |

{ |

$10,750 if Single |

|

|

|

|

|

|

N.C. standard deduction |

$21,500 if Married Filing Jointly or Surviving Spouse |

|

|

|

|||

|

based on your filing status. |

$10,750 if Married Filing Separately |

|

|

|

_______________________$ |

. |

|

|

|

$16,125 if Head of Household |

|

2. |

||||

3. |

Subtract Line 2 from Line 1. If Line 1 is less than Line 2, enter ZERO (0) |

|

3. |

_______________________$ |

. |

|||

|

|

|||||||

4. |

Enter an estimate of your total N.C. Child Deduction Amount from Page 3, Schedule 2 |

4. |

_______________________$ |

. |

||||

|

||||||||

5. |

Enter an estimate of your total federal adjustments to income and State deductions from |

|

_______________________$ |

. |

||||

|

federal adjusted gross income |

................................................................................................................................ |

|

|

5. |

|||

|

|

|

|

|

|

|||

6. |

Add Lines 3, 4, and 5 |

|

|

|

6. |

_______________________$ |

. |

|

|

|

|

|

|||||

7. |

Enter an estimate of your nonwage income (such as dividends or interest) |

7. |

$_____________________ |

. |

|

|

||

|

|

|

||||||

8.Enter an estimate of your State additions to federal adjusted gross

|

income |

8. |

$ |

. |

|

|

|

|

|

|

|||

9. |

Add Lines 7 and 8 |

|

9. |

$ |

. |

|

|

|

|||||

10. |

Subtract Line 9 from Line 6 (Do not enter less than zero) |

|

10. |

$ |

. |

|

|

|

|||||

11. |

Divide the amount on Line 10 by $2,500 . Round down to whole number |

|

11. |

_______________________ |

||

|

Ex. $3,900 ÷ $2,500 = 1.56 rounds down to 1 |

|

|

|

|

|

12. |

Enter the amount of your estimated N.C. tax credits |

12. |

$ |

. |

|

|

|

|

|

||||

13. |

Divide the amount on Line 12 by $134. Round down to whole number |

|

13. |

_______________________ |

||

|

Ex. $200 ÷ $134 = 1.49 rounds down to 1 |

|

|

|

|

|

14. If filing as Single, Head of Household, or Married Filing Separately, enter zero (0) on this line. If filing as Surviving Spouse, enter 4.

If filing as Married Filing Jointly, enter the appropriate number from either (a), (b), (c), (d), or (e) below.

(a)Your spouse expects to have combined wages and taxable retirement benefits of $0 for N.C. purposes, enter 4. (Taxable retirement benefits do not include: Bailey, Social Security, and Railroad retirement)

(b)Your spouse expects to have combined wages and taxable retirement benefits of more than $0 but less than or equal to $3,250, enter 3.

(c)Your spouse expects to have combined wages and taxable retirement benefits of more than $3,250 but less than or equal to $5,750, enter 2.

(d)Your spouse expects to have combined wages and taxable retirement benefits of more than $5,750 but less than or equal to $8,250, enter 1.

(e)Your spouse expects to have combined wages and taxable retirement benefits of more than

$8,250, enter 0 |

14. |

_______________________ |

|

|

15. Add Lines 11, 13, and 14, and enter the total here |

15. |

_______________________ |

|

|

16. If you completed this worksheet on the basis of Married Filing Jointly, the total number of allowances determined |

|

|

|

|

on Line 15 may be split between you and your spouse, however, you choose. Enter the number of allowances |

|

|

|

|

from Line 15 that your spouse plans to claim |

16. |

_______________________ |

|

|

17. Subtract Line 16 from Line 15 and enter the total number of allowances here and on Line 1 of your |

|

|

|

|

Form |

17. |

_______________________ |

|

|

|

|

|

|

|

|

|

Page |

|

2 |

|

|

|

|

|

Important: If you cannot reasonably estimate the amount to enter in the schedules below, you should enter ZERO (0) on Line 1,

Schedule 1 |

Estimated N.C. Itemized Deductions |

|

|

|

Qualifying mortgage interest |

$ |

. |

|

|

Real estate property taxes |

$ |

. |

|

. |

Total qualifying mortgage interest and real estate property taxes* |

$ |

|||

Charitable Contributions (Same as allowed for federal purposes) |

$ |

. |

||

Medical and Dental Expenses (Same as allowed for federal purposes) |

$ |

. |

||

Total estimated N.C. itemized deductions. Enter on Page 2, Part II, Line 1 |

|

$ |

. |

|

*The sum of your qualified mortgage interest and real estate property taxes may not exceed $20,000. For married taxpayers, the $20,000 limitation applies to the combined total of qualified mortgage interest and real estate property

taxes claimed by both spouses, rather than to each spouse separately.

Schedule 2 |

Estimated N.C. Child Deduction Amount |

A taxpayer who is allowed a federal child tax credit under section 24 of the Internal Revenue Code is allowed a deduction for each dependent child unless adjusted gross income exceeds the threshold amount shown below.

The N.C. Child Deduction Amount can be claimed only for a child who is under 17 years of age on the last day of the year.

|

|

|

Deduction |

|

|

|

No. of |

Amount per |

Estimated |

Filing Status |

Adjusted Gross Income |

Children |

Qualifying Child |

Deduction |

Single |

Up to |

$ |

20,000 |

|

Over |

$ |

20,000 |

|

Over |

$ |

30,000 |

|

Over |

$ |

40,000 |

|

Over |

$ |

50,000 |

|

Over |

$ |

60,000 |

MFJ or SS |

Up to |

$ |

40,000 |

|

Over |

$ |

40,000 |

|

Over |

$ |

60,000 |

|

Over |

$ |

80,000 |

|

Over |

$ |

100,000 |

|

Over |

$ |

120,000 |

HOH |

Up to |

$ |

30,000 |

|

Over |

$ |

30,000 |

|

Over |

$ |

45,000 |

|

Over |

$ |

60,000 |

|

Over |

$ |

75,000 |

|

Over |

$ |

90,000 |

MFS |

Up to |

$ |

20,000 |

|

Over |

$ |

20,000 |

|

Over |

$ |

30,000 |

|

Over |

$ |

40,000 |

|

Over |

$ |

50,000 |

|

Over |

$ |

60,000 |

|

|

|

_____________ |

$ |

2,500 |

______________ |

Up to |

$ |

30,000 |

_____________ |

$ |

2,000 |

______________ |

Up to |

$ |

40,000 |

_____________ |

$ |

1,500 |

______________ |

Up to |

$ |

50,000 |

_____________ |

$ |

1,000 |

______________ |

Up to |

$ |

60,000 |

_____________ |

$ |

500 |

______________ |

|

|

|

_____________ |

$ |

- |

______________ |

|

|

|

_____________ |

$ |

2,500 |

______________ |

Up to |

$ |

60,000 |

_____________ |

$ |

2,000 |

______________ |

Up to |

$ |

80,000 |

_____________ |

$ |

1,500 |

______________ |

Up to |

$ |

100,000 |

_____________ |

$ |

1,000 |

______________ |

Up to |

$ |

120,000 |

_____________ |

$ |

500 |

______________ |

|

|

|

_____________ |

$ |

- |

______________ |

|

|

|

_____________ |

$ |

2,500 |

______________ |

Up to |

$ |

45,000 |

_____________ |

$ |

2,000 |

______________ |

Up to |

$ |

60,000 |

_____________ |

$ |

1,500 |

______________ |

Up to |

$ |

75,000 |

_____________ |

$ |

1,000 |

______________ |

Up to |

$ |

90,000 |

_____________ |

$ |

500 |

______________ |

|

|

|

_____________ |

$ |

- |

______________ |

|

|

|

_____________ |

$ |

2,500 |

______________ |

Up to |

$ |

30,000 |

_____________ |

$ |

2,000 |

______________ |

Up to |

$ |

40,000 |

_____________ |

$ |

1,500 |

______________ |

Up to |

$ |

50,000 |

_____________ |

$ |

1,000 |

______________ |

Up to |

$ |

60,000 |

_____________ |

$ |

500 |

______________ |

|

|

|

_____________ |

$ |

- |

______________ |

Page 3

Multiple Jobs Table

Find the amount of your estimated annual wages from your lowest paying job(s) in the left hand column. Follow across to find the amount of additional tax to be withheld for each pay period. Enter the additional amount to be withheld on Line 2 of your Form

Additional Withholding for Single, Married, or Surviving Spouse with Multiple Jobs

Estimated Annual Wages |

|

Payroll Period |

|

||

At Least |

But Less Than |

Monthly |

Semimonthly |

Biweekly |

Weekly |

|

|

|

|

|

|

0 |

1000 |

2 |

1 |

1 |

1 |

1000 |

2000 |

7 |

3 |

3 |

2 |

|

|

|

|

|

|

2000 |

3000 |

11 |

6 |

5 |

3 |

|

|

|

|

|

|

3000 |

4000 |

16 |

8 |

7 |

4 |

|

|

|

|

|

|

4000 |

5000 |

20 |

10 |

9 |

5 |

|

|

|

|

|

|

5000 |

6000 |

25 |

12 |

11 |

6 |

|

|

|

|

|

|

6000 |

7000 |

29 |

14 |

13 |

7 |

7000 |

8000 |

33 |

17 |

15 |

8 |

|

|

|

|

|

|

8000 |

9000 |

38 |

19 |

17 |

9 |

9000 |

10000 |

42 |

21 |

20 |

10 |

10000 |

10750 |

46 |

23 |

21 |

11 |

|

|

|

|

|

|

10750 |

Unlimited |

48 |

24 |

22 |

11 |

Additional Withholding for Head of Household Filers with Multiple Jobs

Estimated Annual Wages |

|

Payroll Period |

|

||

At Least |

But Less Than |

Monthly |

Semimonthly |

Biweekly |

Weekly |

|

|

|

|

|

|

0 |

1000 |

2 |

1 |

1 |

1 |

|

|

|

|

|

|

1000 |

2000 |

7 |

3 |

3 |

2 |

2000 |

3000 |

11 |

6 |

5 |

3 |

|

|

|

|

|

|

3000 |

4000 |

16 |

8 |

7 |

4 |

4000 |

5000 |

20 |

10 |

9 |

5 |

5000 |

6000 |

25 |

12 |

11 |

6 |

6000 |

7000 |

29 |

14 |

13 |

7 |

7000 |

8000 |

33 |

17 |

15 |

8 |

8000 |

9000 |

38 |

19 |

17 |

9 |

9000 |

10000 |

42 |

21 |

20 |

10 |

10000 |

11000 |

47 |

23 |

22 |

11 |

11000 |

12000 |

51 |

26 |

24 |

12 |

12000 |

13000 |

56 |

28 |

26 |

13 |

13000 |

14000 |

60 |

30 |

28 |

14 |

14000 |

15000 |

65 |

32 |

30 |

15 |

15000 |

16000 |

69 |

35 |

32 |

16 |

16000 |

Unlimited |

71 |

36 |

33 |

16 |

Page 4

| Fact Name | Details |

|---|---|

| Purpose | The NC-4 form is used to determine the correct amount of North Carolina state income tax to withhold from an employee's pay. |

| Filing Requirement | If an employee does not submit an NC-4, the employer must withhold taxes as if the employee is single with zero allowances. |

| Form Variants | There are different versions of the NC-4: NC-4 EZ for standard deductions, and NC-4 NRA for nonresident aliens. |

| Withholding Allowances | Employees can claim allowances based on their financial situation, which can reduce the amount withheld from their paychecks. |

| Multiple Jobs | Employees with more than one job should use one NC-4 to claim all allowances for the highest-paying job. |

| Tax Credits | Tax credits and deductions can influence the number of allowances claimed on the NC-4 form. |

| Head of Household | To qualify as Head of Household, an employee must be unmarried and contribute more than half of household expenses for dependents. |

| Surviving Spouse | Surviving spouses can claim this status if their spouse died in the last two tax years and they maintain a household for a dependent child. |

| Legal Review | All NC-4 forms may be reviewed by the North Carolina Department of Revenue, ensuring compliance with state tax laws. |

Completing the NC-4 form is essential for ensuring the correct amount of state income tax is withheld from your pay. Follow these steps to accurately fill out the form.

After completing the form, submit it to your employer. Keep a copy for your records. If your circumstances change, such as a change in filing status or number of allowances, submit a new NC-4 within ten days of the change.

What is the purpose of the NC-4 form?

The NC-4 form is an Employee’s Withholding Allowance Certificate used to determine the correct amount of North Carolina state income tax to withhold from an employee's pay. Employees must complete this form and provide it to their employer. If an employee does not submit an NC-4, the employer is required to withhold taxes as if the employee is single with zero allowances, which may result in higher tax withholding than necessary.

Who should use the NC-4 EZ form?

The NC-4 EZ form is designed for individuals who plan to claim either the North Carolina Standard Deduction or the North Carolina Child Deduction Amount without any other deductions or tax credits. This simplified form allows eligible taxpayers to quickly determine their withholding allowances, making the process more efficient.

What should I do if my withholding allowances change?

If there is a change in your circumstances that affects your withholding allowances, you must submit a new NC-4 form to your employer within 10 days of the change. For example, if you cease to qualify as "Head of Household," you are not required to file a new NC-4 until the next tax year. It is crucial to keep your employer informed to ensure that the correct amount of tax is withheld from your pay.

What happens if I provide incorrect information on my NC-4?

Providing inaccurate information on the NC-4 that leads to a lower amount of tax being withheld than what should be is a serious matter. If it is determined that the information lacks a reasonable basis, the employee may face a penalty of 50% of the amount that was not properly withheld. It is essential to provide accurate and truthful information to avoid such penalties.

Using the Wrong Ink Color: It’s essential to use blue or black ink when filling out the NC-4 form. Using red ink can lead to issues with readability and processing.

Including Punctuation: When entering your information, do not use dollar signs, commas, or other punctuation marks. This can cause confusion and errors in your tax withholding calculations.

Submitting Copies Instead of Originals: Always submit the original NC-4 form to your employer. Sending copies can result in delays or complications in processing your withholding allowances.

Mixing Form Types: Ensure that you are using the correct form for your situation. For example, nonresident aliens must use Form NC-4 NRA. Mixing different forms can lead to incorrect withholding amounts.

Not Updating Allowances: If your personal situation changes, such as losing a dependent or changing your filing status, you must file a new NC-4 within 10 days. Failing to do so can result in incorrect tax withholding.

Claiming Incorrect Allowances: Make sure to accurately complete the NC-4 Allowance Worksheet. Claiming too many or too few allowances can lead to underpayment or overpayment of taxes throughout the year.

The NC-4 form is an Employee's Withholding Allowance Certificate used in North Carolina to determine the appropriate amount of state income tax to withhold from an employee's paycheck. Several other forms and documents may accompany the NC-4 to provide additional information or fulfill specific requirements related to tax withholding and deductions. Below is a list of these forms and documents.

These forms and documents work together to ensure accurate tax withholding and compliance with North Carolina tax regulations. Completing them correctly can help individuals manage their tax obligations effectively.

The NC-4 form is similar to the IRS Form W-4, which is used by employees to determine the amount of federal income tax withholding from their paychecks. Both forms allow employees to claim allowances based on their personal and financial situations. By providing this information, employees help their employers withhold the correct amount of tax, ensuring that they neither owe a large sum at tax time nor receive a substantial refund. The W-4 also requires updates when personal circumstances change, similar to the NC-4.

Another similar document is the IRS Form W-4P, which is used for withholding on pension or annuity payments. Like the NC-4, this form allows individuals to specify the amount of tax to be withheld from their retirement income. It is essential for ensuring that retirees manage their tax liabilities effectively. Both forms require the individual to assess their tax situation and make informed decisions about withholding allowances.

The NC-4 is also comparable to the IRS Form 1040-ES, which is used for making estimated tax payments. Individuals who expect to owe tax may use this form to calculate and submit quarterly payments. Similar to the NC-4, it requires taxpayers to estimate their income and deductions to determine their tax liability. Both forms aim to prevent underpayment penalties by ensuring that individuals pay the appropriate amount of tax throughout the year.

Form NC-4 EZ is another related document, designed for individuals who wish to claim the North Carolina Standard Deduction or Child Deduction without additional complexities. This form simplifies the process by allowing taxpayers to avoid claiming other deductions or credits. Like the NC-4, it serves the purpose of adjusting withholding amounts based on specific tax situations, but with fewer requirements.

The NC-4 NRA is tailored for nonresident aliens, similar to IRS Form 1040-NR. Both forms cater to individuals who are not U.S. citizens and have specific tax obligations. They provide guidelines for determining withholding allowances and ensuring compliance with tax laws. Each form addresses the unique circumstances of nonresident taxpayers, allowing them to report income accurately.

Form NC-40 is relevant for individuals making estimated tax payments in North Carolina, similar to IRS Form 1040-ES. Both forms help taxpayers manage their tax responsibilities by allowing them to pay estimated taxes throughout the year. They serve as proactive measures to avoid underpayment penalties, particularly for those with nonwage income or fluctuating earnings.

The NC-4 Allowance Worksheet is akin to the IRS W-4 Worksheet, which assists taxpayers in calculating their withholding allowances. Both worksheets guide individuals through a series of questions about their financial situation, helping them determine the appropriate number of allowances to claim. This process ensures that the withholding aligns with their tax liability, minimizing the risk of owing taxes at the end of the year.

Lastly, the NC-4 for Married Filing Jointly and Separately is similar to the IRS Form 1040, where married couples can choose to file jointly or separately. Both forms require couples to consider their combined income and deductions to optimize their tax situation. The decisions made on these forms can significantly impact the amount of tax withheld and the overall tax liability for the couple.

When filling out the NC-4 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below is a list of ten things to do and avoid.

This is incorrect. Employees must complete the NC-4 form to ensure their employer withholds the correct amount of state income tax. Without it, employers default to withholding based on a “Single” filing status with zero allowances.

The instructions specify that only blue or black ink should be used. Using red ink or other colors may result in processing issues.

It is essential to submit only one type of form. Mixing form types can lead to incorrect withholding calculations.

If your withholding allowances decrease, you must file a new NC-4 within 10 days of the change. Failure to do so could result in incorrect tax withholding.

While you may claim fewer allowances than you are entitled to, you cannot claim more. Doing so can lead to penalties for providing false information.

Nonresident aliens must use the NC-4 NRA form, which is specifically designed for their tax situation.

Individuals with significant nonwage income should consider making estimated tax payments using Form NC-40 to avoid underpayment penalties.

Married taxpayers have the option to file jointly or separately. Each filing status has different implications for allowances and tax calculations.

Any individual earning income in North Carolina, including part-time workers and freelancers, should complete the NC-4 to ensure proper tax withholding.

The NC-4 form must be printed and submitted in hard copy to your employer. Electronic submissions are not accepted for this form.