The Missouri Promissory Note form serves as a vital financial instrument that outlines the terms of a loan agreement between a borrower and a lender. It establishes a clear record of the borrower's commitment to repay a specified amount, along with any applicable interest, by a predetermined date. Essential components of this form include the names and addresses of both parties, the principal amount being borrowed, and the interest rate, which can be fixed or variable. Additionally, the document may specify repayment terms, including the frequency of payments and any late fees that may apply. By detailing these key elements, the Missouri Promissory Note helps to protect the interests of both parties involved, ensuring that expectations are clearly defined and legally enforceable. Understanding the structure and purpose of this form is crucial for anyone considering entering into a lending agreement in Missouri.

Missouri Promissory Note Template

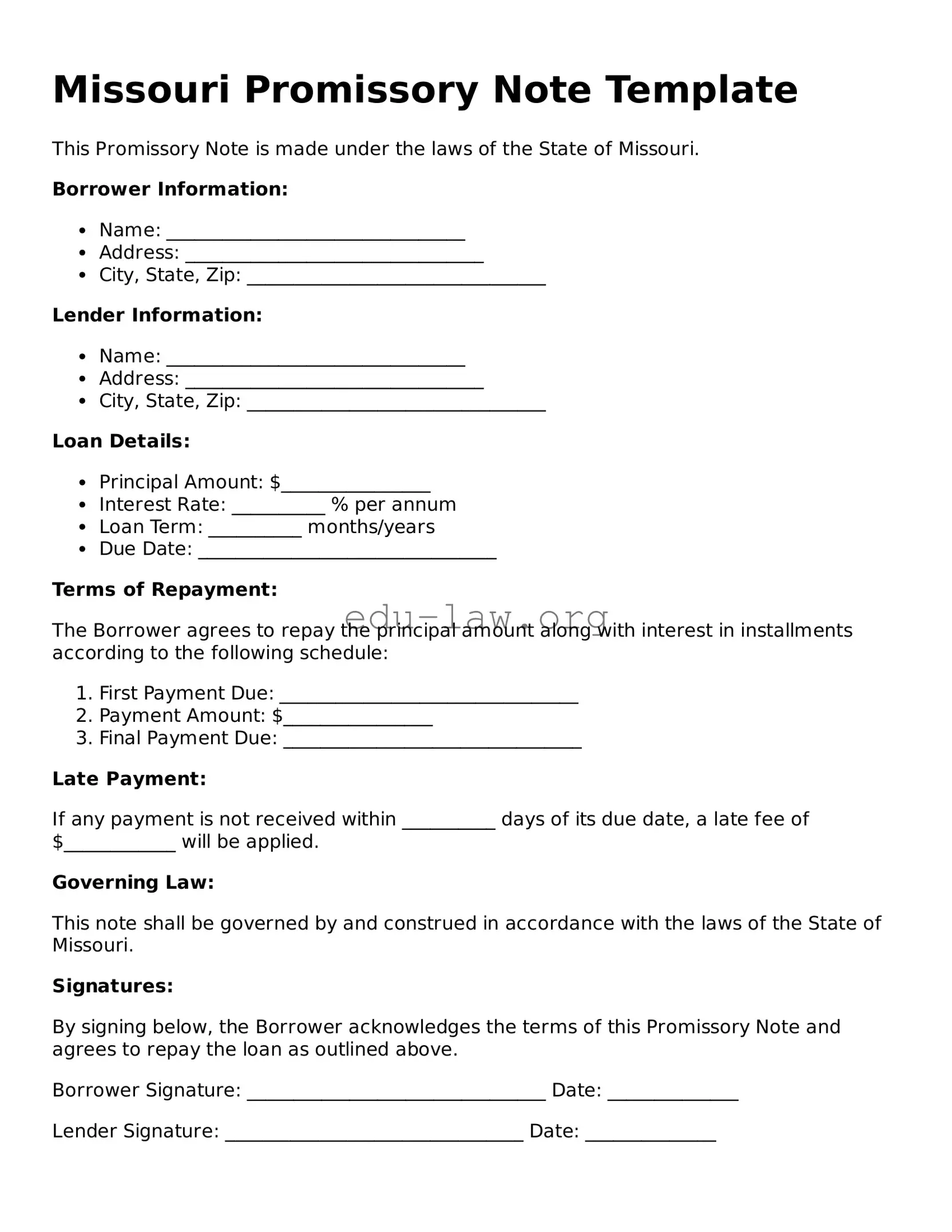

This Promissory Note is made under the laws of the State of Missouri.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the principal amount along with interest in installments according to the following schedule:

Late Payment:

If any payment is not received within __________ days of its due date, a late fee of $____________ will be applied.

Governing Law:

This note shall be governed by and construed in accordance with the laws of the State of Missouri.

Signatures:

By signing below, the Borrower acknowledges the terms of this Promissory Note and agrees to repay the loan as outlined above.

Borrower Signature: ________________________________ Date: ______________

Lender Signature: ________________________________ Date: ______________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated party at a determined time. |

| Governing Law | The Missouri Uniform Commercial Code (UCC) governs promissory notes in Missouri. |

| Parties Involved | Typically, there are two parties: the maker (borrower) and the payee (lender). |

| Interest Rate | The interest rate can be fixed or variable, depending on the agreement between the parties. |

| Payment Terms | Payment terms should clearly outline when and how payments will be made. |

| Default Clause | A default clause may be included, specifying what happens if the borrower fails to make payments. |

| Notarization | While notarization is not required, it can provide additional legal protection. |

| Transferability | Promissory notes can be transferred to other parties, often through endorsement. |

| Enforceability | For a promissory note to be enforceable, it must meet certain legal requirements, including clarity and specificity. |

| State-Specific Considerations | Missouri law may have specific provisions regarding the enforcement of promissory notes, including statute of limitations. |

Once you have the Missouri Promissory Note form in front of you, it is important to carefully fill it out to ensure that all necessary information is accurately recorded. This document will serve as a formal agreement between the borrower and the lender, detailing the terms of the loan. Following the steps below will help guide you through the process of completing the form correctly.

After completing the form, it is advisable to keep copies for both parties. This ensures that everyone has a record of the agreement and can refer to it in the future if needed. Proper documentation is key to maintaining clarity and trust in financial transactions.

What is a Missouri Promissory Note?

A Missouri Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. This document outlines the terms of the loan, including the interest rate, payment schedule, and any collateral involved. It serves as a legal record of the debt agreement between the borrower and the lender.

Who can use a Missouri Promissory Note?

Anyone can use a Missouri Promissory Note. This includes individuals, businesses, and organizations. Whether you’re lending money to a friend, financing a car, or providing a loan to a business, this document can help protect both parties by clearly defining the terms of the agreement.

What information should be included in a Promissory Note?

A well-drafted Missouri Promissory Note should include the following information: the names and addresses of both the borrower and lender, the principal amount of the loan, the interest rate, the repayment schedule, and any late fees or penalties for missed payments. Additionally, it should specify whether the loan is secured or unsecured and include any other relevant terms.

Is a Missouri Promissory Note legally binding?

Yes, a Missouri Promissory Note is legally binding as long as it meets certain criteria. Both parties must agree to the terms, and the document should be signed by both the borrower and lender. It’s also advisable to have a witness or notary present during the signing to further validate the agreement.

What happens if the borrower fails to repay the loan?

If the borrower fails to repay the loan as outlined in the Promissory Note, the lender has the right to take legal action. This could include filing a lawsuit to recover the owed amount. The specific steps may vary based on the terms of the note and Missouri law, so it’s essential to understand your rights and obligations.

Can a Promissory Note be modified?

Yes, a Promissory Note can be modified if both parties agree to the changes. It’s important to document any modifications in writing and have both parties sign the amended agreement. This ensures that the updated terms are clear and enforceable.

Where can I find a Missouri Promissory Note template?

You can find Missouri Promissory Note templates online through various legal websites or resources. Many templates are available for free or at a low cost. However, it’s advisable to consult with a legal expert to ensure that the template meets your specific needs and complies with Missouri law.

Incomplete Information: One common mistake is leaving sections blank. All relevant fields must be filled out to ensure the document is valid.

Incorrect Names: People often misspell names or use nicknames instead of legal names. Always use the full legal name of the borrower and lender.

Missing Signatures: A promissory note is not valid without the signatures of both parties. Ensure that both the borrower and lender sign the document.

Improper Dates: Failing to include the date of signing can lead to confusion later. Always write the date clearly in the designated space.

Vague Terms: People sometimes use unclear language regarding repayment terms. Be specific about the payment schedule, interest rate, and any penalties for late payments.

Ignoring State Laws: Each state has specific requirements for promissory notes. Familiarize yourself with Missouri's laws to ensure compliance.

Failure to Keep Copies: After signing, it’s crucial to keep a copy of the note for your records. This helps in case of disputes or misunderstandings.

When dealing with a Missouri Promissory Note, several other documents may be needed to support the transaction. Each of these documents plays a crucial role in ensuring clarity and legal compliance. Below is a list of commonly used forms and documents.

Understanding these documents can help ensure a smoother lending process. Each plays a vital role in protecting both the lender and the borrower throughout the loan lifecycle.

The Missouri Promissory Note form shares similarities with a Loan Agreement. Both documents outline the terms of a loan, including the amount borrowed, interest rates, and repayment schedule. A Loan Agreement may be more detailed, specifying conditions under which the loan may be defaulted upon, while the Promissory Note focuses primarily on the borrower's promise to repay the loan. Essentially, the Promissory Note can be viewed as a simpler version of a Loan Agreement, capturing the core elements of the borrowing arrangement.

Another document akin to the Missouri Promissory Note is a Secured Loan Agreement. This type of agreement includes additional provisions that specify collateral backing the loan. Like the Promissory Note, it outlines the borrower's obligation to repay the borrowed amount. The key difference lies in the presence of collateral in the Secured Loan Agreement, which provides the lender with a form of security if the borrower fails to repay.

A Personal Loan Agreement also resembles the Missouri Promissory Note. Both documents are used when one individual lends money to another. They detail the loan amount, interest rate, and repayment terms. However, a Personal Loan Agreement may include more personal details about the parties involved, as well as specific conditions that govern the loan, making it slightly more comprehensive than a basic Promissory Note.

The Commercial Promissory Note is another document that aligns with the Missouri Promissory Note. This type of note is specifically designed for business transactions. It serves the same purpose of documenting a promise to pay, but it often includes terms that reflect the nature of commercial lending, such as payment terms that accommodate business cash flow cycles. Thus, while both documents serve similar functions, the Commercial Promissory Note is tailored for business contexts.

A Mortgage Note can also be compared to the Missouri Promissory Note. Both documents serve as a promise to repay a loan, but a Mortgage Note is specifically tied to real estate transactions. It includes details about the property being financed and often contains provisions regarding foreclosure if the borrower defaults. The core idea of a repayment promise remains, but the context and additional stipulations set the Mortgage Note apart.

The Student Loan Note is another document similar to the Missouri Promissory Note. It outlines the terms under which a borrower agrees to repay funds used for educational expenses. Like the Promissory Note, it specifies the loan amount and repayment terms. However, the Student Loan Note may include specific provisions related to deferment or forgiveness, reflecting the unique nature of educational financing.

Finally, an IOU (I Owe You) is a very basic document that shares some characteristics with the Missouri Promissory Note. An IOU acknowledges a debt and the amount owed, but it typically lacks the formal structure and detailed terms found in a Promissory Note. While an IOU serves as a simple acknowledgment of debt, the Promissory Note provides a more comprehensive framework for repayment, including interest rates and a repayment schedule.

When filling out the Missouri Promissory Note form, it's important to follow certain guidelines. Here are ten things to consider:

Following these guidelines can help ensure that the Promissory Note is completed correctly and is legally binding.

Understanding the Missouri Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are eight common misconceptions about this form:

By understanding these misconceptions, individuals can better navigate the complexities of the Missouri Promissory Note form and make informed decisions regarding their financial agreements.

When filling out and using the Missouri Promissory Note form, it is important to understand several key aspects to ensure the document is valid and effective. Below are essential takeaways to consider:

By paying attention to these details, individuals can create a clear and enforceable Promissory Note that protects the interests of both the borrower and the lender.