The Louisiana Promissory Note form serves as a vital tool in financial transactions, establishing a clear agreement between a borrower and a lender. This document outlines the amount borrowed, the interest rate, and the repayment schedule, ensuring both parties understand their obligations. It typically includes essential details such as the names and addresses of the parties involved, the date of the agreement, and the consequences of default. By clearly stating the terms, the form minimizes the potential for disputes and fosters trust between the parties. Additionally, it often contains provisions regarding prepayment and late fees, which can be critical in managing the loan's terms. Understanding the nuances of this form can empower individuals and businesses alike to navigate their financial dealings with confidence.

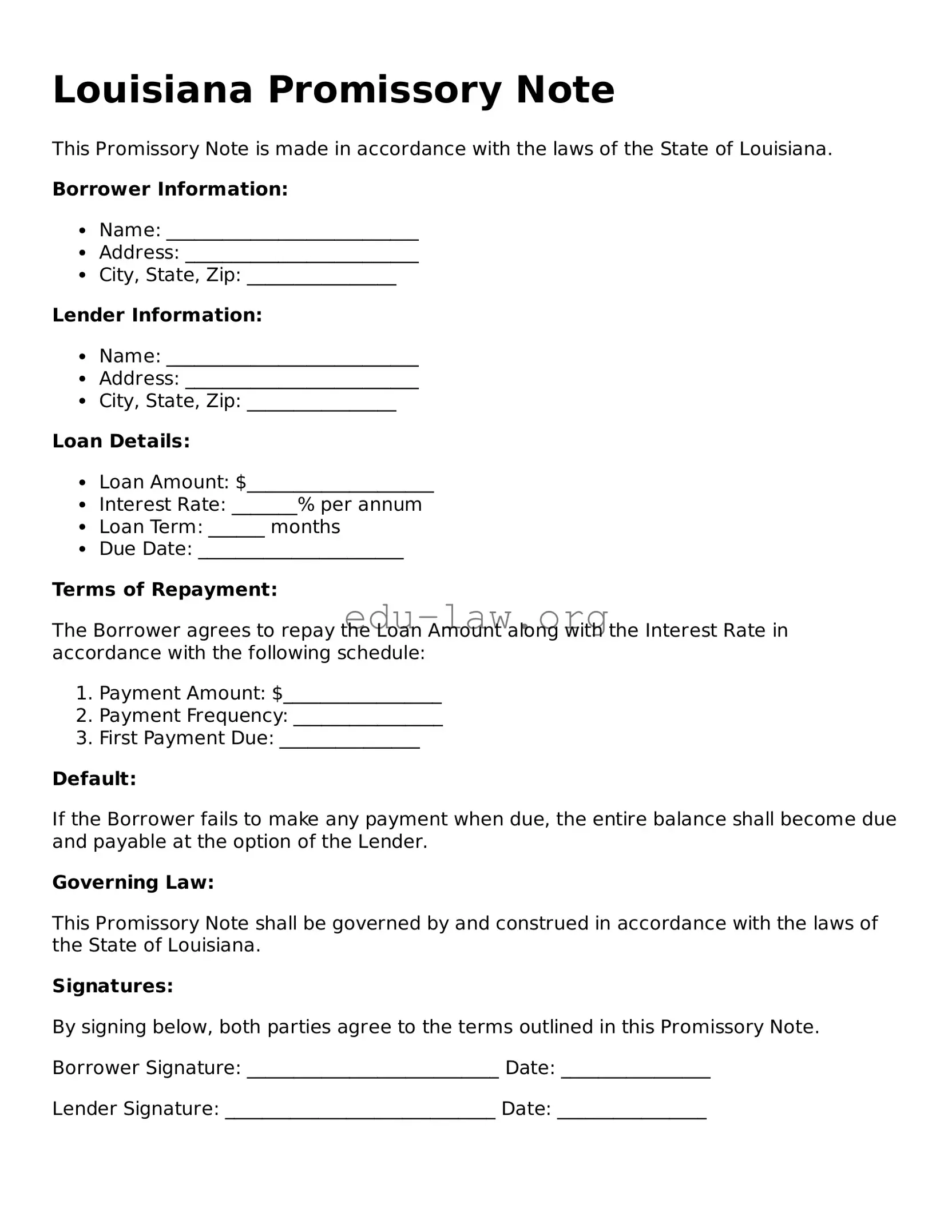

Louisiana Promissory Note

This Promissory Note is made in accordance with the laws of the State of Louisiana.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the Loan Amount along with the Interest Rate in accordance with the following schedule:

Default:

If the Borrower fails to make any payment when due, the entire balance shall become due and payable at the option of the Lender.

Governing Law:

This Promissory Note shall be governed by and construed in accordance with the laws of the State of Louisiana.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

Borrower Signature: ___________________________ Date: ________________

Lender Signature: _____________________________ Date: ________________

| Fact Name | Details |

|---|---|

| Definition | A Louisiana Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a specified time. |

| Governing Law | The Louisiana Civil Code governs promissory notes, particularly under Title 13, which outlines obligations and contracts. |

| Parties Involved | The note involves two main parties: the maker (borrower) and the payee (lender). |

| Interest Rates | Interest rates can be specified in the note, but they must comply with Louisiana's usury laws to avoid excessive charges. |

| Payment Terms | Payment terms, including the due date and method of payment, must be clearly stated in the note. |

| Enforceability | A properly executed promissory note is legally enforceable in Louisiana courts, provided it meets all legal requirements. |

| Signature Requirement | The maker must sign the note for it to be valid, indicating their commitment to repay the borrowed amount. |

Once you have the Louisiana Promissory Note form in hand, you can begin the process of filling it out. This form is essential for documenting a loan agreement between a borrower and a lender. After completing the form, both parties will need to sign it to make it legally binding.

What is a Louisiana Promissory Note?

A Louisiana Promissory Note is a legal document that outlines a borrower's promise to repay a specific amount of money to a lender under agreed-upon terms. It includes details such as the principal amount, interest rate, repayment schedule, and any applicable fees. This document serves as a binding agreement between the two parties and can be used in various financial transactions, including personal loans, business loans, or real estate financing.

What are the key components of a Louisiana Promissory Note?

Key components of a Louisiana Promissory Note typically include the names and addresses of both the borrower and lender, the principal amount borrowed, the interest rate, the repayment terms, and the maturity date. Additionally, it may outline any late fees or penalties for missed payments, as well as any collateral securing the loan. It is essential that all parties clearly understand these terms before signing the document.

Is a Louisiana Promissory Note enforceable in court?

Yes, a Louisiana Promissory Note is generally enforceable in court, provided it meets the legal requirements of a contract. This includes mutual consent, a lawful object, and consideration. If a borrower fails to repay the loan as agreed, the lender may take legal action to recover the owed amount. Having a properly executed note can significantly strengthen the lender's position in such cases.

Do I need a lawyer to create a Louisiana Promissory Note?

While it is not legally required to have a lawyer draft a Louisiana Promissory Note, consulting with one is advisable, especially for larger loans or complex agreements. A legal professional can ensure that the document complies with state laws and adequately protects the interests of both parties. For simpler transactions, templates are available that can be customized to fit specific needs.

Incorrect Borrower Information: Many individuals fail to provide accurate personal details, such as the full legal name and current address of the borrower. This can lead to confusion and complications later on.

Missing Lender Details: Just as with the borrower, the lender's name and address must be clearly stated. Omitting this information can render the note unenforceable.

Improper Loan Amount: Some people mistakenly write the loan amount incorrectly. It's crucial to ensure that both the numerical and written forms of the amount match.

Failure to Specify Interest Rate: Not indicating an interest rate or leaving it blank can lead to misunderstandings. Clearly stating the rate helps avoid disputes in the future.

Neglecting Payment Terms: Individuals often overlook the importance of defining the payment schedule. Clearly outlining the frequency and amount of payments is essential for both parties.

Not Signing the Document: A common oversight is forgetting to sign the promissory note. Without a signature, the document lacks legal validity and cannot be enforced.

The Louisiana Promissory Note is a crucial document in lending transactions, outlining the terms of a loan between a borrower and a lender. Alongside this form, several other documents are often utilized to ensure clarity and legal compliance in the agreement. Below is a list of common forms and documents that may accompany the Louisiana Promissory Note.

These documents collectively support the lending process, ensuring that both parties are informed and protected. Each plays a vital role in establishing a clear understanding of the loan terms and conditions.

A Louisiana Promissory Note is similar to a Loan Agreement. Both documents outline the terms of a loan between a borrower and a lender. They specify the amount borrowed, the interest rate, and the repayment schedule. While a promissory note is often simpler and focuses mainly on the borrower's promise to repay, a loan agreement may include additional clauses covering collateral, default conditions, and other legal protections for the lender.

An Installment Agreement also shares similarities with a Louisiana Promissory Note. This document details a payment plan for a loan, breaking down the total amount into smaller, manageable payments over time. Like a promissory note, it outlines the interest rate and repayment terms. However, an installment agreement typically emphasizes the payment schedule and may include consequences for missed payments, making it more comprehensive in some respects.

A Secured Promissory Note is another document that parallels the Louisiana Promissory Note. This type of note includes a promise to repay but is backed by collateral, such as property or assets. If the borrower defaults, the lender has the right to claim the collateral. This added layer of security for the lender distinguishes it from a standard promissory note, which does not require collateral.

A Demand Note is also akin to a Louisiana Promissory Note. This type of note allows the lender to demand repayment at any time, rather than following a set schedule. While both documents serve as a promise to pay, a demand note offers more flexibility for the lender. Borrowers should be aware that this can create uncertainty regarding when they will need to repay the loan.

A Personal Guarantee can be compared to a Louisiana Promissory Note as well. This document involves a third party who agrees to repay the loan if the primary borrower defaults. While a promissory note focuses on the borrower's promise, a personal guarantee adds an extra layer of security for the lender. It ensures that even if the borrower cannot pay, the lender has recourse to another party.

Lastly, a Mortgage Note resembles a Louisiana Promissory Note in that it is a written promise to repay borrowed money. However, a mortgage note specifically relates to real estate transactions. It includes details about the loan amount, interest rate, and repayment terms, just like a promissory note. The key difference lies in the fact that a mortgage note is secured by the property itself, giving the lender the right to foreclose if the borrower fails to make payments.

When filling out the Louisiana Promissory Note form, consider the following guidelines:

Understanding the Louisiana Promissory Note form can be challenging due to several misconceptions. Here are four common misunderstandings:

While notarization can provide an extra layer of authenticity, it is not a legal requirement for the validity of a promissory note in Louisiana. As long as the note is signed by the borrower and includes the necessary terms, it remains enforceable.

There is no mandated format for a Louisiana Promissory Note. The essential components include the names of the parties, the amount borrowed, the interest rate, and the repayment terms. Flexibility exists in how these elements are presented.

People often think that promissory notes are only necessary for substantial loans. However, even small personal loans or informal agreements can benefit from a written promissory note to clarify terms and protect both parties.

In reality, promissory notes can be amended if both parties agree to the changes. It is crucial to document any modifications in writing to ensure clarity and enforceability.

When filling out and using the Louisiana Promissory Note form, several important considerations should be kept in mind. Understanding these key aspects can help ensure that the document serves its intended purpose effectively.