When navigating the complex world of home financing, understanding the Loan Estimate form is crucial for any prospective borrower. This essential document, provided by lenders, outlines key details about the loan you are considering. It includes important information such as the loan amount, interest rate, and monthly payments, giving you a clear picture of your financial commitment. Additionally, the Loan Estimate breaks down closing costs, allowing you to see exactly what you will owe at closing and how those costs are calculated. You’ll find sections dedicated to loan terms, projected payments, and even comparisons with other loans, which can be invaluable in making informed decisions. The form also highlights potential changes to your loan terms before closing, ensuring you are aware of any factors that could affect your overall costs. With all this information at your fingertips, you can confidently assess your options and compare different loan offers, ultimately leading to a more informed and empowered home-buying experience.

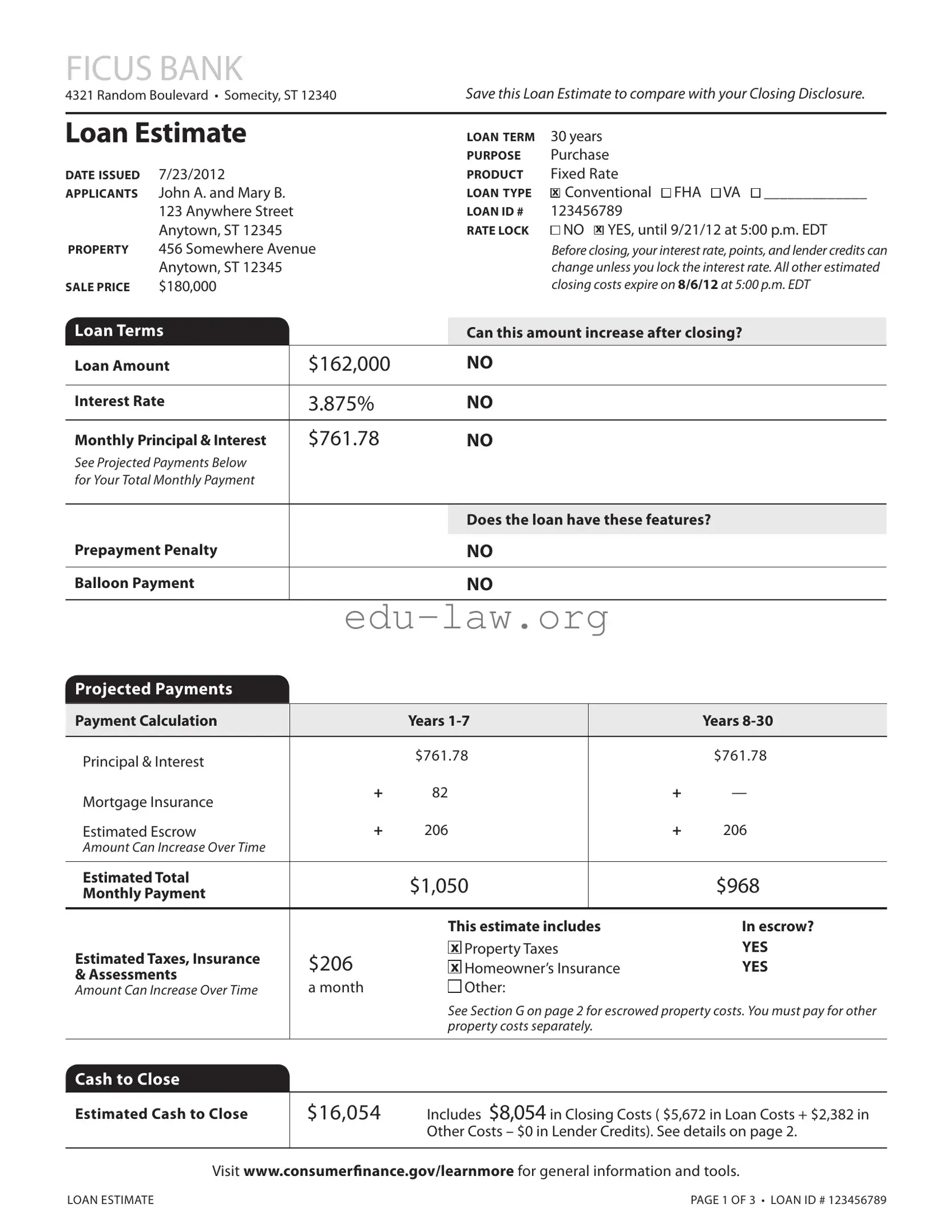

FICUS BANK

4321 Random Boulevard • Somecity, ST 12340Save this Loan Estimate to compare with your Closing Disclosure.

Loan estimate |

LOAN TeRM |

30 years |

|

|

|

PuRPOse |

Purchase |

DATe IssueD |

7/23/2012 |

PRODuCT |

Fixed Rate |

APPLICANTs |

John A. and Mary B. |

LOAN TyPe |

x Conventional FHA VA _____________ |

|

123 Anywhere Street |

LOAN ID # |

123456789 |

|

Anytown, ST 12345 |

RATe LOCK |

NO x YES, until 9/21/12 at 5:00 p.m. EDT |

PROPeRTy |

456 Somewhere Avenue |

|

Before closing, your interest rate, points, and lender credits can |

|

Anytown, ST 12345 |

|

change unless you lock the interest rate. All other estimated |

sALe PRICe |

$180,000 |

|

closing costs expire on 8/6/12 at 5:00 p.m. EDT |

Loan Terms |

|

Can this amount increase after closing? |

Loan Amount |

$162,000 |

NO |

|

|

|

Interest Rate |

3.875% |

NO |

|

|

|

Monthly Principal & Interest |

$761.78 |

NO |

See Projected Payments Below |

|

|

for Your Total Monthly Payment |

|

|

|

|

|

|

|

Does the loan have these features? |

Prepayment Penalty |

|

|

|

NO |

|

|

|

|

Balloon Payment |

|

NO |

|

|

|

Projected Payments

Payment Calculation |

|

years |

|

|

years |

|

|

|

|

|

|

Principal & Interest |

|

$761.78 |

|

|

$761.78 |

|

|

|

|

|

|

Mortgage Insurance |

+ |

82 |

|

+ |

— |

|

|

|

|

|

|

Estimated Escrow |

+ |

206 |

|

+ |

206 |

Amount Can Increase Over Time |

|

|

|

|

|

|

|

|

|

|

|

estimated Total |

|

$1,050 |

|

|

$968 |

Monthly Payment |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This estimate includes |

|

In escrow? |

|

estimated Taxes, Insurance |

$206 |

x Property Taxes |

|

yes |

|

x Homeowner’s Insurance |

|

yes |

|||

& Assessments |

|

||||

a month |

Other: |

|

|

||

Amount Can Increase Over Time |

|

|

|||

|

|

See Section G on page 2 for escrowed property costs. You must pay for other |

|||

|

|

property costs separately. |

|

|

|

|

|

|

|

|

|

Cash to Close |

|

|

|

|

|

|

|

|

|

||

estimated Cash to Close |

$16,054 |

Includes $8,054 in Closing Costs ( $5,672 in Loan Costs + $2,382 in |

|||

|

|

Other Costs – $0 in Lender Credits). See details on page 2. |

|||

|

|

|

|

|

|

Visit www.consumerinance.gov/learnmore for general information and tools.

LOAN ESTIMATE |

page 1 of 3 • Loan ID # 123456789 |

Closing Cost Details

Loan Costs

A. Origination Charges |

$1,802 |

.25 % of Loan Amount (Points) |

$405 |

Application Fee |

$300 |

Underwriting Fee |

$1,097 |

Other Costs

e. Taxes and Other Government Fees |

$85 |

||||||

Recording Fees and Other Taxes |

|

|

$85 |

||||

Transfer Taxes |

|

|

$0 |

||||

|

|

|

|

|

|

|

|

F. Prepaids |

|

|

$867 |

||||

Homeowner’s Insurance Premium ( |

6 months) |

$605 |

|||||

|

|

|

|

|

|

|

|

Mortgage Insurance Premium ( 0 |

months) |

$0 |

|||||

|

|

|

|

|

|

||

Prepaid Interest ( $17.44 per day for 15 days @ 3.875%) |

$262 |

||||||

Property Taxes ( 0 months) |

|

|

$0 |

||||

|

|

|

|

|

|

|

|

B. services you Cannot shop For |

$672 |

Appraisal Fee |

$405 |

Credit Report Fee |

$30 |

Flood Determination Fee |

$20 |

Flood Monitoring Fee |

$32 |

Tax Monitoring Fee |

$75 |

Tax Status Research Fee |

$110 |

G. Initial escrow Payment at Closing |

|

|

$413 |

|

Homeowner’s Insurance |

$100.83 per month for |

23mo. $202 |

||

Mortgage Insurance |

per month for |

0 |

mo. |

|

Property Taxes |

$105.30 per month for |

2 |

mo. |

$211 |

H. Other |

$1,017 |

Title – Owner’s Title Policy (optional) |

$1,017 |

C. services you Can shop For |

$3,198 |

Pest Inspection Fee |

$135 |

Survey Fee |

$65 |

Title – Insurance Binder |

$700 |

Title – Lender’s Title Policy |

$535 |

Title – Title Search |

$1,261 |

Title – Settlement Agent Fee |

$502 |

D. TOTAL LOAN COsTs (A + B + C) |

$5,672 |

I. TOTAL OTHeR COsTs (e + F + G + H) |

$2,382 |

|

|

J. TOTAL CLOsING COsTs |

$8,054 |

|

|

D + I |

$8,054 |

Lender Credits |

$0 |

Calculating Cash to Close |

|

|

|

Total Closing Costs (J) |

$8,054 |

Closing Costs Financed (Included in Loan Amount) |

$0 |

Down Payment/Funds from Borrower |

$18,000 |

Deposit |

– $10,000 |

Funds for Borrower |

$0 |

Seller Credits |

$0 |

Adjustments and Other Credits |

$0 |

estimated Cash to Close |

$16,054 |

|

|

LOAN ESTIMATE |

page 2 of 3 • Loan ID # 123456789 |

Additional Information About This Loan

LeNDeR NMLs/LICeNse ID

LOAN OFFICeR

NMLs ID

PHONe

Ficus Bank

Joe Smith 12345 [email protected]

MORTGAGe BROKeR NMLs/LICeNse ID LOAN OFFICeR NMLs ID

eMAIL PHONe

Comparisons |

use these measures to compare this loan with other loans. |

||

|

|

|

|

In 5 years |

$56,582 |

Total you will have paid in principal, interest, mortgage insurance, and loan costs. |

|

$15,773 |

Principal you will have paid of. |

||

|

|||

|

|

|

|

Annual Percentage Rate (APR) |

4.494% |

Your costs over the loan term expressed as a rate. This is not your interest rate. |

|

|

|

|

|

Total Interest Percentage (TIP) |

69.447% |

The total amount of interest that you will pay over the loan term as a |

|

|

|

percentage of your loan amount. |

|

|

|

|

|

Other Considerations

Appraisal |

We may order an appraisal to determine the property’s value and charge you for this |

|

appraisal. We will promptly give you a copy of any appraisal, even if your loan does not close. |

|

You can pay for an additional appraisal for your own use at your own cost. |

Assumption |

If you sell or transfer this property to another person, we |

|

will allow, under certain conditions, this person to assume this loan on the original terms. |

|

x will not allow this person to assume this loan on the original terms. |

Homeowner’s |

This loan requires homeowner’s insurance on the property, which you may obtain from a |

Insurance |

company of your choice that we ind acceptable. |

Late Payment |

If your payment is more than 15 days late, we will charge a late fee of 5% of the monthly |

|

principal and interest payment. |

Reinance |

Reinancing this loan will depend on your future inancial situation, the property value, and |

|

market conditions. You may not be able to reinance this loan. |

servicing |

We intend |

|

to service your loan. If so, you will make your payments to us. |

|

x to transfer servicing of your loan. |

Conirm Receipt

By signing, you are only conirming that you have received this form. You do not have to accept this loan because you have signed or received this form.

Applicant Signature |

Date |

Date |

LOAN ESTIMATE |

page 3 of 3 • Loan ID #123456789 |

| Fact Name | Description |

|---|---|

| Purpose | The Loan Estimate form is used to provide borrowers with clear information about the costs of a mortgage loan. |

| Loan Terms | It outlines key loan details, including the loan amount, interest rate, and monthly payment. |

| Rate Lock | Borrowers can lock in their interest rate, preventing changes before closing. |

| Closing Costs | The form details estimated closing costs, including both loan costs and other costs. |

| Projected Payments | It provides a breakdown of monthly payments over the loan term, including principal, interest, and insurance. |

| Comparisons | Borrowers can compare the Loan Estimate with other loan offers to make informed decisions. |

| Cash to Close | The estimated cash needed at closing is clearly stated, helping borrowers prepare financially. |

| Governing Law | In the U.S., the Loan Estimate form is governed by the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA). |

| Homeowner's Insurance | The loan typically requires homeowner's insurance, which protects the property against damage. |

Filling out the Loan Estimate form is an important step in understanding your mortgage options. After completing the form, you'll have a clearer picture of the costs involved in your loan. This will help you make informed decisions as you move forward in the mortgage process.

What is a Loan Estimate form?

The Loan Estimate form is a standardized document that lenders are required to provide to borrowers within three business days of receiving a loan application. It outlines the key details of the mortgage loan, including loan terms, estimated monthly payments, and closing costs. This form is designed to help borrowers understand the financial implications of the loan and compare it with other loan offers. It is crucial to review this document carefully, as it serves as a foundation for your mortgage decision-making process.

How can I use the Loan Estimate to compare different loans?

The Loan Estimate includes essential information such as the interest rate, monthly payments, and total closing costs. By reviewing these figures, you can easily compare different loan offers from various lenders. Pay particular attention to the Annual Percentage Rate (APR), which reflects the total cost of borrowing over the loan term. This allows you to evaluate not just the interest rate but also the associated fees. Make sure to save each Loan Estimate you receive, as they will help you make informed decisions about which loan best meets your financial needs.

What should I do if I notice discrepancies in my Loan Estimate?

If you find any discrepancies or unclear information in your Loan Estimate, it is essential to contact your lender immediately. Clarifying these issues can prevent misunderstandings later in the loan process. Ask specific questions about any fees or terms that seem inconsistent with your expectations or previous discussions. Remember, you have the right to understand every aspect of your loan before proceeding, and your lender should be willing to provide explanations and corrections as needed.

What happens if I decide not to proceed with the loan after receiving the Loan Estimate?

Receiving a Loan Estimate does not obligate you to proceed with the loan. It is simply a document that confirms you have received important information about the loan terms. If you choose not to move forward, you can walk away without any penalty. However, it is advisable to communicate your decision to the lender, as this can help maintain a good relationship should you wish to explore other options in the future.

How long is the Loan Estimate valid?

The Loan Estimate is valid for a specific period, typically until the closing costs expire, as indicated on the form. In this case, the closing costs expire on 8/6/12 at 5:00 p.m. EDT. After this date, the lender may issue a new Loan Estimate if the terms of the loan change or if you decide to proceed with the application. It is important to keep track of these timelines to ensure you are making decisions based on the most current information available.

Neglecting to Review the Form Thoroughly: Many applicants fail to carefully read the Loan Estimate. This can lead to misunderstandings about terms and costs.

Overlooking the Interest Rate Lock: Some individuals do not pay attention to whether their interest rate is locked. A locked rate can protect against future increases.

Ignoring Estimated Closing Costs: Applicants often overlook the total closing costs. This can result in unexpected expenses at closing.

Failing to Compare with Other Offers: Many people do not compare the Loan Estimate with offers from other lenders. This can lead to missed opportunities for better terms.

Misunderstanding Escrow Payments: Some borrowers do not grasp how escrow payments work. This can affect their monthly budget and cash flow.

Not Asking Questions: Applicants often hesitate to ask questions about unclear terms. This can lead to confusion and mistakes later in the process.

Assuming the Loan Terms Will Not Change: Many individuals mistakenly believe that the terms outlined in the Loan Estimate are final. In reality, changes can occur before closing.

Forgetting to Confirm Receipt: Some applicants neglect to sign and confirm receipt of the Loan Estimate. This step is crucial for ensuring that all parties are on the same page.

The Loan Estimate form is an essential document in the mortgage process, providing borrowers with a clear overview of their loan terms and associated costs. However, several other forms and documents often accompany it, each serving a unique purpose. Here’s a list of those documents and a brief description of each.

Understanding these documents can empower borrowers to navigate the mortgage process with confidence. Each form plays a vital role in ensuring transparency and protecting the interests of all parties involved. Being informed helps in making educated decisions throughout the home buying journey.

The Loan Estimate form is similar to the Good Faith Estimate (GFE), which was commonly used before the implementation of the TILA-RESPA Integrated Disclosure rule. Both documents provide borrowers with an estimate of the costs associated with obtaining a mortgage. They aim to help consumers understand the financial aspects of their loan options. However, the Loan Estimate is more detailed and standardized, making it easier for borrowers to compare different loan offers. The GFE, while informative, lacked the same level of clarity and uniformity that the Loan Estimate now provides.

Another document akin to the Loan Estimate is the Closing Disclosure. This form is provided to borrowers three days before closing on their mortgage. It outlines the final terms of the loan and the closing costs. While the Loan Estimate offers an initial view of costs and terms, the Closing Disclosure provides the actual figures that borrowers will encounter at closing. Both documents serve the purpose of ensuring transparency and allowing borrowers to review and compare costs, but the Closing Disclosure reflects the finalized terms after all negotiations are complete.

The Truth in Lending (TIL) statement also shares similarities with the Loan Estimate. This document provides important information about the costs of borrowing, including the annual percentage rate (APR) and total interest paid over the life of the loan. Like the Loan Estimate, the TIL statement aims to inform borrowers about the financial implications of their loan. However, the Loan Estimate is more comprehensive, incorporating additional details about closing costs and monthly payments, which the TIL statement does not cover in depth.

The HUD-1 Settlement Statement is another document that resembles the Loan Estimate. Historically, this form was used at closing to itemize all charges and credits involved in a real estate transaction. While the HUD-1 provided a detailed breakdown of costs, it was often criticized for being confusing. The Loan Estimate improves upon this by presenting estimated costs in a clearer format, making it easier for borrowers to understand what to expect when they reach the closing table.

The Mortgage Loan Disclosure Statement (MLDS) is similar in that it provides borrowers with key details about their mortgage. This document typically includes information about the loan amount, interest rate, and other terms. However, the Loan Estimate is more standardized and user-friendly, allowing for easier comparisons between different loan offers. Both documents aim to ensure that borrowers are well-informed about their mortgage options.

The Pre-Closing Disclosure is another document that bears a resemblance to the Loan Estimate. This form is often provided to borrowers shortly before closing, summarizing the terms of the loan and the closing costs. Similar to the Loan Estimate, it is designed to help borrowers understand their financial obligations. However, the Pre-Closing Disclosure is more focused on the final details of the loan, while the Loan Estimate provides an initial overview of costs and terms.

The Loan Commitment Letter also shares characteristics with the Loan Estimate. This document is issued by the lender once the borrower has been approved for a loan. It outlines the terms of the loan and any conditions that must be met before closing. While both documents serve to inform the borrower about the loan's terms, the Loan Commitment Letter is typically more specific to the approval stage, whereas the Loan Estimate provides a broader overview of potential costs and terms at the outset.

The Borrower’s Affidavit is another document that can be compared to the Loan Estimate. This form is often required at closing and attests to the borrower's identity and financial situation. While it does not provide cost estimates, it is part of the overall mortgage process. The Loan Estimate, on the other hand, focuses on providing a clear breakdown of costs and terms associated with the loan, helping borrowers make informed decisions.

Finally, the Application for a Mortgage Loan also shares some similarities with the Loan Estimate. The application collects essential information from the borrower, including income, assets, and debts. This information helps lenders determine the loan amount and terms. While the Loan Estimate presents the estimated costs and terms of the loan, the application serves as the foundation upon which those estimates are built, making both documents integral to the mortgage process.

When filling out the Loan Estimate form, it's essential to approach the process thoughtfully. Here are ten things you should and shouldn't do to ensure accuracy and clarity.

The Loan Estimate is not a final commitment to lend. It is an estimate of the loan terms and costs that can change before closing.

While the Loan Estimate provides an overview of expected costs, some fees can change before closing, especially if the loan terms are modified.

The interest rate can change unless it is locked in by the borrower. This is an important detail to consider when reviewing the estimate.

The Loan Estimate covers many costs, but it does not include every potential expense, such as future property taxes or homeowners' association fees.

Each lender may provide different Loan Estimates based on their terms, rates, and fees. Comparing estimates from multiple lenders is advisable.

Signing the Loan Estimate confirms receipt but does not obligate the borrower to accept the loan. The borrower can still explore other options.

The Loan Estimate remains relevant throughout the loan process, especially when comparing it to the Closing Disclosure, which provides final terms.

Understanding the Loan Estimate form is crucial for anyone looking to secure a mortgage. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the loan process with greater confidence and clarity.