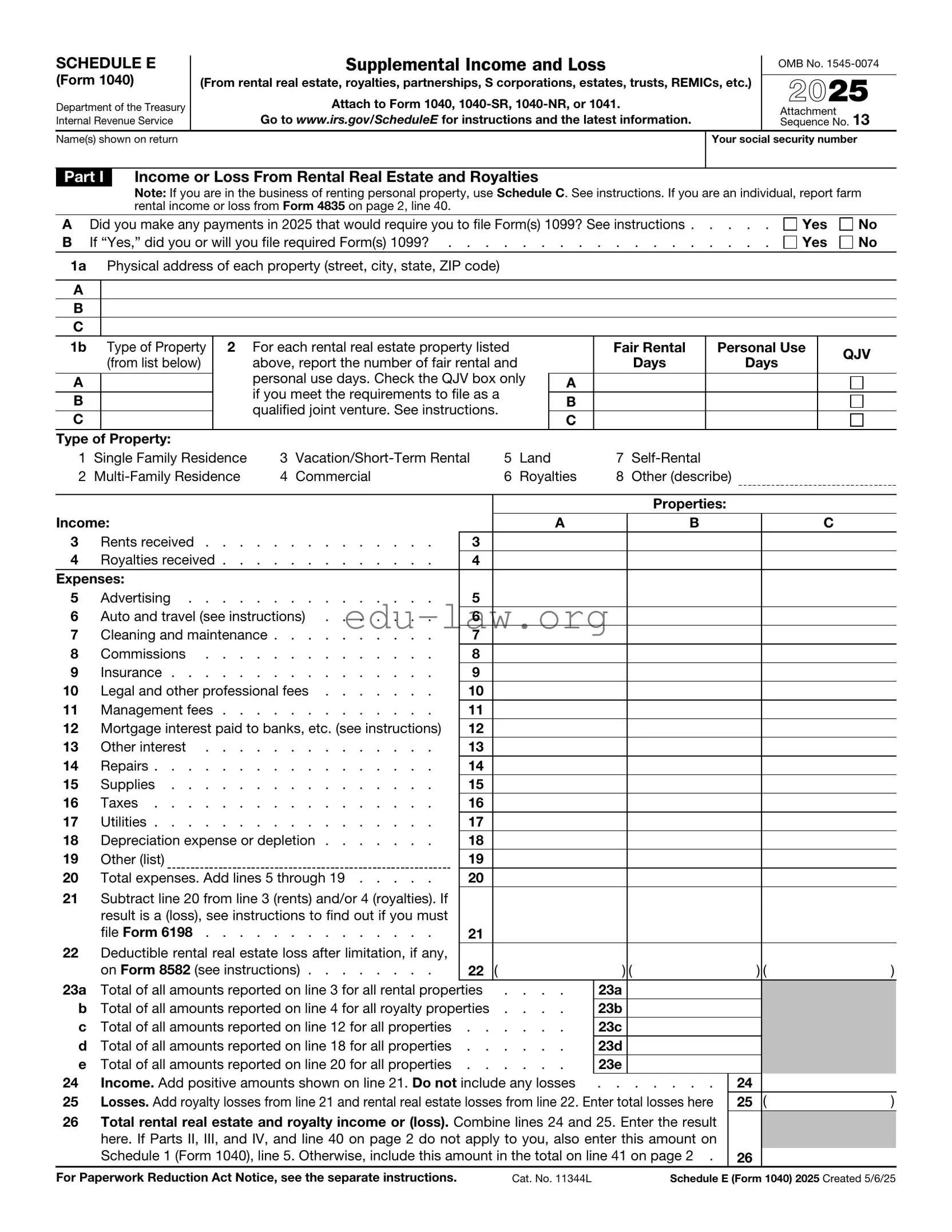

The IRS Schedule E (Form 1040) plays a crucial role for individuals who earn income from various sources beyond traditional employment. This form is primarily used to report income or loss from rental real estate, partnerships, S corporations, estates, trusts, and other pass-through entities. Taxpayers must carefully detail their income, expenses, and deductions related to these activities, ensuring accurate reporting to the IRS. Additionally, it provides a framework for calculating passive activity losses and credits, which can significantly impact overall tax liability. Understanding the nuances of Schedule E is essential for anyone involved in real estate or partnerships, as it helps in maximizing potential deductions while complying with federal tax regulations. Whether you are a seasoned investor or a first-time landlord, familiarity with this form can lead to better financial outcomes and smoother tax filing experiences.

SCHEDULE E |

|

|

|

|

Supplemental Income and Loss |

|

|

|

|

OMB No. |

||||||||||||||

|

|

|

|

|

|

|||||||||||||||||||

(Form 1040) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

(From rental real estate, royalties, partnerships, S corporations, estates, trusts, REMICs, etc.) |

|

2025 |

||||||||||||||||||||

Department of the Treasury |

|

|

|

|

Attach to Form 1040, |

|

|

|

||||||||||||||||

Internal Revenue Service |

|

|

|

Go to www.irs.gov/ScheduleE for instructions and the latest information. |

|

|

Attachment |

|

13 |

|||||||||||||||

|

|

|

|

|

Sequence No. |

|||||||||||||||||||

Name(s) shown on return |

|

|

|

|

|

|

|

|

|

|

|

Your social security number |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Part I |

|

Income or Loss From Rental Real Estate and Royalties |

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

Note: If you are in the business of renting personal property, use Schedule C. See instructions. If you are an individual, report farm |

||||||||||||||||||||

|

|

|

|

rental income or loss from Form 4835 on page 2, line 40. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

A |

Did you make any payments in 2025 that would require you to file Form(s) 1099? See instructions . |

. . . . |

Yes |

|

No |

|||||||||||||||||||

B |

If “Yes,” did you or will you file required Form(s) 1099? . |

. . . . . . . . . . . . . |

. . . . |

Yes |

|

No |

||||||||||||||||||

1a Physical address of each property (street, city, state, ZIP code) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b |

|

Type of Property |

2 |

For each rental real estate property listed |

|

|

|

|

Fair Rental |

Personal Use |

|

QJV |

||||||||||||

|

|

(from list below) |

|

above, report the number of fair rental and |

|

|

|

|

|

Days |

Days |

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

personal use days. Check the QJV box only |

|

|

|

|

|

|

|

|

|

|

|

|||||

A |

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

if you meet the requirements to file as a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

B |

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

qualified joint venture. See instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

C |

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Type of Property: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

1 |

Single Family Residence |

3 |

5 |

Land |

|

|

7 |

|

|

|

|

|

|

|||||||||||

2 |

4 |

Commercial |

|

|

6 |

Royalties |

8 |

Other (describe) |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Properties: |

|

|

|

|

||

Income: |

|

|

|

|

|

|

|

|

|

|

|

A |

|

B |

|

|

|

C |

|

|

||||

3 |

|

Rents received |

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

4 |

|

Royalties received |

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

5 |

|

Advertising |

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

6 |

|

Auto and travel (see instructions) |

6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

7 |

|

Cleaning and maintenance |

7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

8 |

|

Commissions |

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

9 |

|

Insurance |

9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

10 |

|

Legal and other professional fees |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

11 |

|

Management fees |

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

12 |

|

Mortgage interest paid to banks, etc. (see instructions) |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

13 |

|

Other interest |

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

14 |

|

Repairs |

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

15 |

|

Supplies |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

16 |

|

Taxes |

16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

17 |

|

Utilities |

17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

18 |

|

Depreciation expense or depletion |

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

19 |

|

Other (list) |

|

|

19 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

20 |

|

Total expenses. Add lines 5 through 19 |

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

21Subtract line 20 from line 3 (rents) and/or 4 (royalties). If result is a (loss), see instructions to find out if you must

file Form 6198 |

21 |

22Deductible rental real estate loss after limitation, if any,

|

on Form 8582 (see instructions) |

22 ( |

) ( |

|

) ( |

) |

23a |

Total of all amounts reported on line 3 for all rental properties . . . . |

23a |

|

|

|

|

b |

Total of all amounts reported on line 4 for all royalty properties . . . . |

23b |

|

|

|

|

c |

Total of all amounts reported on line 12 for all properties |

23c |

|

|

|

|

d |

Total of all amounts reported on line 18 for all properties |

23d |

|

|

|

|

e |

Total of all amounts reported on line 20 for all properties |

23e |

|

|

|

|

24 |

Income. Add positive amounts shown on line 21. Do not include any losses |

. . . . . . . |

24 |

|

|

|

25 |

Losses. Add royalty losses from line 21 and rental real estate losses from line 22. Enter total losses here |

25 |

( |

) |

||

26Total rental real estate and royalty income or (loss). Combine lines 24 and 25. Enter the result here. If Parts II, III, and IV, and line 40 on page 2 do not apply to you, also enter this amount on

Schedule 1 (Form 1040), line 5. Otherwise, include this amount in the total on line 41 on page 2 . |

26 |

||

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11344L |

Schedule E (Form 1040) 2025 Created 5/6/25 |

|

Schedule E (Form 1040) 2025 |

Attachment Sequence No. 13 |

Page 2 |

Name(s) shown on return. Do not enter name and social security number if shown on other side. |

Your social security number |

|

Caution: The IRS compares amounts reported on your tax return with amounts shown on Schedule(s)

Part II Income or Loss From Partnerships and S Corporations

Note: If you report a loss, receive a distribution, dispose of stock, or receive a loan repayment from an S corporation, you must check the box in column (e) on line 28 and attach the required basis computation. If you report a loss from an

27Are you reporting any loss not allowed in a prior year due to the

passive activity (if that loss was not reported on Form 8582), or unreimbursed partnership expenses? If you answered “Yes,”

see instructions before completing this section |

Yes |

No |

28

A

B

C

D

(a)Name

(b)Enter P for partnership; S

for S corporation

(c)Check if foreign

partnership

(d)Employer

identification number

(e)Check if

basis computation

is required

(f)Check if any amount is

not at risk

|

|

Passive Income and Loss |

Nonpassive Income and Loss |

|

|||||

|

(g) Passive loss allowed |

(h) Passive income |

(i) Nonpassive loss allowed |

|

(j) Section 179 expense |

(k) Nonpassive income |

|||

|

(attach Form 8582 if required) |

from Schedule |

(see Schedule |

|

deduction from Form 4562 |

from Schedule |

|||

A |

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

29a |

Totals |

|

|

|

|

|

|

|

|

b |

Totals |

|

|

|

|

|

|

|

|

30 |

Add columns (h) and (k) of line 29a |

. . . . . . . . . |

|

. . . . . . |

30 |

|

|

||

31 |

Add columns (g), (i), and (j) of line 29b |

. . . . . . . . . |

|

. . . . . . |

31 ( |

) |

|||

32 |

Total partnership and S corporation income or (loss). Combine lines 30 and 31 |

. . . . . |

32 |

|

|

||||

Part III Income or Loss From Estates and Trusts

33

A

B

(a)Name

(b)Employer

identification number

|

|

|

Passive Income and Loss |

|

Nonpassive Income and Loss |

|

|||||

|

|

(c) Passive deduction or loss allowed |

|

(d) Passive income |

|

(e) Deduction or loss |

|

(f) Other income from |

|

||

|

|

|

(attach Form 8582 if required) |

|

from Schedule |

|

from Schedule |

|

Schedule |

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

34a |

Totals |

|

|

|

|

|

|

|

|

|

|

b |

Totals |

|

|

|

|

|

|

|

|

|

|

35 |

Add columns (d) and (f) of line 34a |

. . . . . . . . . . . . |

35 |

|

|

||||||

36 |

Add columns (c) and (e) of line 34b |

. . . . . . . . . . . . |

36 |

( |

) |

||||||

37 |

Total estate and trust income or (loss). Combine lines 35 and 36 |

37 |

|

|

|||||||

Part IV |

Income or Loss From Real Estate Mortgage Investment Conduits |

Holder |

|

||||||||

38 |

|

|

(a) Name |

|

(b) Employer |

(c) Excess inclusion from |

(d) Taxable income |

(e) Income from |

|

||

|

|

|

|

identification number |

Schedules Q, line 2c |

(net loss) from |

|

Schedules Q, line 3b |

|

||

|

|

|

|

|

(see instructions) |

Schedules Q, line 1b |

|

||||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

||||

39 |

Combine columns (d) and (e) only. Enter |

the result here and include in the total on line 41 below . |

39 |

|

|

||||||

Part V |

Summary |

|

|

|

|

|

|

|

|

||

40 |

Net farm rental income or (loss) from Form 4835. Also, complete line 42 below |

40 |

|

|

|||||||

41Total income or (loss). Combine lines 26, 32, 37, 39, and 40. Enter the result here and on Schedule

1 (Form 1040), line 5 |

. . . . . . . . . |

41 |

|

42 Reconciliation of farming and fishing income. Enter your gross |

|

|

|

farming and fishing income reported on Form 4835, line 7; Schedule |

|

|

|

(Form 1065), box 14, code B; Schedule |

|

|

|

AN; and Schedule |

42 |

|

|

43 Reconciliation for real estate professionals. If you were a real estate |

|

|

|

professional (see instructions), enter the net income or (loss) you |

|

|

|

reported anywhere on Form 1040, Form |

|

|

|

from all rental real estate activities in which you materially participated |

|

|

|

under the passive activity loss rules |

43 |

|

|

Schedule E (Form 1040) 2025

| Fact Name | Description |

|---|---|

| Purpose | Schedule E (Form 1040) is used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. |

| Filing Requirement | Taxpayers must file Schedule E if they have income or losses from the aforementioned sources, regardless of whether they are actively involved in managing those properties or businesses. |

| Income Reporting | Income reported on Schedule E is typically considered passive income, which may affect the taxpayer's eligibility for certain deductions and credits. |

| State-Specific Forms | Some states require additional forms for reporting rental income. For example, California mandates the use of Form 540 for state income tax purposes under California Revenue and Taxation Code Section 17041. |

| Filing Deadline | Schedule E must be filed by the tax return deadline, which is typically April 15 for most taxpayers, unless an extension has been granted. |

Filling out the IRS Schedule E 1040 form requires careful attention to detail. This form is essential for reporting income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and more. Ensure you have all necessary documentation before starting the process.

What is IRS Schedule E used for?

IRS Schedule E is primarily used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and other pass-through entities. By detailing these income sources, taxpayers can accurately calculate their total income on Form 1040, which is essential for determining their tax liability.

Who needs to file Schedule E?

Taxpayers who earn income from rental properties, receive royalties, or participate in partnerships or S corporations typically need to file Schedule E. If you own a rental property, even if it was not rented for the entire year, you must report any income or expenses related to that property.

What types of income are reported on Schedule E?

Schedule E encompasses various income types. This includes rental income from properties, royalties from intellectual property, and income from partnerships and S corporations. Additionally, if you have income from estates or trusts, that must also be reported on this form.

Can I deduct expenses on Schedule E?

Yes, you can deduct certain expenses associated with the income reported on Schedule E. Common deductions include mortgage interest, property tax, repairs, maintenance, and management fees. These deductions can help reduce your taxable income, making it crucial to keep accurate records of all related expenses.

How do I report rental income on Schedule E?

To report rental income, you will need to provide details about each rental property you own. This includes the address, the type of property, and the total rental income received. You'll also list any related expenses to calculate your net rental income or loss, which will ultimately flow to your Form 1040.

What if I have a loss from my rental property?

If you experience a loss from your rental property, you can report that loss on Schedule E. Depending on your overall income, you may be able to deduct this loss from other income, potentially lowering your overall tax liability. However, there are specific rules regarding passive activity losses that may affect your ability to deduct these losses.

Is there a deadline for filing Schedule E?

Schedule E must be filed along with your Form 1040 by the tax filing deadline, which is usually April 15th. If you need additional time, you can file for an extension, but it’s important to pay any estimated taxes owed by the original deadline to avoid penalties and interest.

Where can I find more information about Schedule E?

For more detailed information about Schedule E, you can visit the IRS website. The IRS provides comprehensive resources, including instructions for completing the form and specific guidelines on reporting various types of income and expenses. Additionally, consulting a tax professional can provide personalized guidance based on your unique financial situation.

Not reporting all rental income: It's crucial to include all sources of rental income. Failing to report even a small amount can lead to penalties.

Incorrectly categorizing expenses: Understanding which expenses are deductible is essential. Misclassifying expenses can result in an inaccurate tax return.

Omitting depreciation: Many individuals overlook the opportunity to deduct depreciation on their rental properties. This can significantly impact the overall tax liability.

Not keeping accurate records: Failing to maintain detailed records of income and expenses can lead to confusion and mistakes on the form.

Ignoring passive activity loss rules: Understanding the limitations on deducting losses from rental properties is vital. Ignoring these rules may lead to disallowed deductions.

Filing with incorrect personal information: Ensure that your name, Social Security number, and other personal details are accurate. Mistakes can delay processing and lead to further complications.

Overlooking special situations: Some taxpayers may have unique circumstances, such as short-term rentals or mixed-use properties. Failing to address these can result in errors.

Not consulting tax regulations: Tax laws can change frequently. Not staying informed about the latest regulations can lead to unintentional mistakes.

Rushing the completion of the form: Taking time to carefully review the form can prevent errors. Rushing through it often leads to mistakes.

Neglecting to sign and date the form: A common oversight is forgetting to sign and date the return. This can result in the form being considered invalid.

The IRS Schedule E (Form 1040) is a crucial document for reporting income or loss from rental real estate, partnerships, S corporations, estates, trusts, and more. Alongside this form, several other documents often play a significant role in accurately reporting income and ensuring compliance with tax regulations. Below are four commonly used forms and documents that complement Schedule E.

Understanding these forms and their purposes can enhance the accuracy of tax filings and ensure that all eligible deductions are claimed. Proper documentation is essential for maintaining compliance and maximizing potential tax benefits.

The IRS Schedule C form is similar to Schedule E in that both are used by individuals who report income from business activities. Schedule C is specifically for sole proprietors who operate a business, allowing them to report income and deduct expenses directly related to that business. In contrast, Schedule E focuses on income derived from rental properties, partnerships, and S corporations. While both forms aim to calculate taxable income, they cater to different types of income sources.

Schedule F is another document that shares similarities with Schedule E. This form is used by farmers to report income and expenses related to farming activities. Like Schedule E, it allows for the deduction of expenses, helping to determine net income. Both schedules require detailed reporting of income sources and expenses, making them essential for individuals in specific industries to accurately report their earnings.

The IRS Form 1065 is a partnership tax return that resembles Schedule E because it also addresses income from partnerships. While Schedule E is used by individual partners to report their share of partnership income, Form 1065 is filed by the partnership itself. Both documents require accurate reporting of income and expenses, ensuring that partners receive the correct information for their personal tax returns.

Form 1120S, the S Corporation tax return, is similar to Schedule E in that it reports income from S Corporations. Shareholders of S Corporations use Schedule E to report their share of the corporation’s income, deductions, and credits. Both forms emphasize the flow-through nature of income, where it is taxed at the individual level rather than at the corporate level, ensuring that shareholders accurately report their earnings.

The IRS Form 1041, used for estates and trusts, has parallels with Schedule E. Both forms report income generated from properties or assets held by the estate or trust. Schedule E is used by beneficiaries to report income received from the estate or trust, while Form 1041 is filed by the fiduciary managing the estate or trust. Each document requires careful reporting to ensure compliance with tax obligations.

Form 8825 is utilized by partnerships and S corporations that own rental real estate, making it similar to Schedule E. This form reports income and expenses for rental real estate activities, allowing for deductions similar to those on Schedule E. Both forms help in calculating the net rental income, ensuring that the tax implications of rental activities are accurately reported.

Schedule K-1 is another relevant document, as it reports income, deductions, and credits from partnerships and S Corporations to individual partners or shareholders. While Schedule E is where individuals report this information on their tax returns, Schedule K-1 provides the necessary details that individuals need to complete Schedule E accurately. Both documents play a critical role in ensuring that income from these entities is properly taxed.

The IRS Form 990 is used by tax-exempt organizations to report their financial information, similar to how Schedule E reports income from various sources. While Form 990 focuses on the financial activities of non-profits, both documents require transparency in reporting income and expenses. This similarity lies in the need for accurate financial reporting, even though the entities involved are different.

Finally, Form 4562 is used for depreciation and amortization, which can relate to properties reported on Schedule E. While Schedule E reports income from rental properties, Form 4562 allows property owners to claim depreciation on those properties. Both forms work together to ensure that property owners can accurately report income while taking advantage of available deductions.

When filling out the IRS Schedule E (Form 1040), it is important to approach the process carefully. Here are some guidelines to help ensure accuracy and compliance.

By following these dos and don'ts, you can navigate the Schedule E form with greater confidence and accuracy.

The IRS Schedule E (Form 1040) is often misunderstood, leading to confusion among taxpayers. Here are five common misconceptions about this form:

Understanding these misconceptions can help taxpayers navigate the complexities of the IRS Schedule E more effectively. Accurate reporting is essential to avoid potential issues with the IRS.

When it comes to filling out the IRS Schedule E (Form 1040), understanding its purpose and requirements is essential for accurate reporting of rental income and other sources. Here are some key takeaways to keep in mind: