The IRS Schedule C (Form 1040) plays a crucial role for many individuals who operate their own businesses or engage in self-employment activities. This form is essential for reporting income and expenses related to a sole proprietorship, allowing business owners to calculate their net profit or loss. By detailing various types of income, such as sales and services rendered, Schedule C enables taxpayers to accurately depict their financial situation to the IRS. Additionally, it provides a structured way to deduct allowable business expenses, which can include costs like supplies, utilities, and even home office expenses. Understanding how to fill out this form correctly is vital, as it impacts tax liability and potential refunds. Furthermore, the form requires careful attention to detail, as errors can lead to audits or penalties. Whether you’re a freelancer, consultant, or small business owner, mastering Schedule C can significantly influence your financial health and compliance with tax regulations.

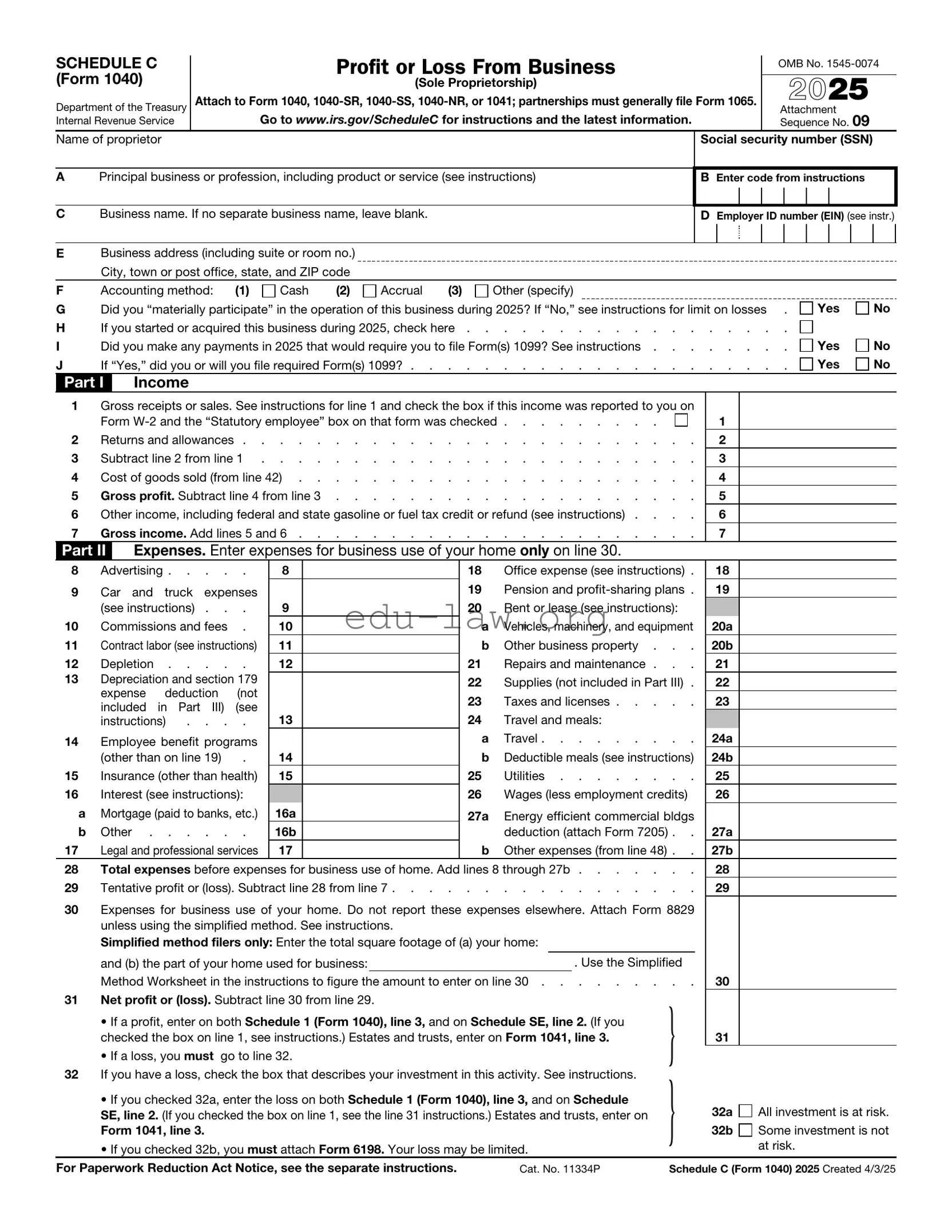

SCHEDULE C (Form 1040)

Department of the Treasury Internal Revenue Service

Profit or Loss From Business

(Sole Proprietorship)

Attach to Form 1040,

Go to www.irs.gov/ScheduleC for instructions and the latest information.

OMB No.

2025

Attachment Sequence No. 09

Name of proprietor

APrincipal business or profession, including product or service (see instructions)

CBusiness name. If no separate business name, leave blank.

Social security number (SSN)

BEnter code from instructions

DEmployer ID number (EIN) (see instr.)

EBusiness address (including suite or room no.) City, town or post office, state, and ZIP code

F |

Accounting method: |

(1) |

Cash |

(2) |

Accrual |

(3) |

Other (specify) |

G |

Did you “materially participate” in the operation of this business during 2025? If “No,” see instructions for limit on losses . |

||||||

H |

If you started or acquired this business during 2025, check here |

||||||

I |

Did you make any payments in 2025 that would require you to file Form(s) 1099? See instructions |

||||||

J |

If “Yes,” did you or will you file required Form(s) 1099? |

||||||

Yes No

Yes No

Yes No

Part I |

|

Income |

|

|

|

|

|

|

|

||

1 |

Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on |

|

|

||||||||

|

Form |

. . . . . . . . . |

1 |

|

|||||||

2 |

Returns and allowances |

. . . . . . . . . . . |

2 |

|

|||||||

3 |

Subtract line 2 from line 1 |

. . . . . . . . . . . |

3 |

|

|||||||

4 |

Cost of goods sold (from line 42) |

. . . . . . . . . . . |

4 |

|

|||||||

5 |

Gross profit. Subtract line 4 from line 3 |

. . . . . . . . . . . |

5 |

|

|||||||

6 |

Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . |

6 |

|

||||||||

7 |

Gross income. Add lines 5 and 6 |

. . . . . . . . . . . |

7 |

|

|||||||

Part II |

|

Expenses. Enter expenses for business use of your home only on line 30. |

|

|

|||||||

8 |

Advertising |

8 |

|

18 |

Office expense (see instructions) . |

18 |

|

||||

9 |

Car |

and |

truck expenses |

|

|

19 |

Pension and |

19 |

|

||

|

(see instructions) . . . |

9 |

|

20 |

Rent or lease (see instructions): |

|

|

||||

10 |

Commissions and fees . |

10 |

|

a |

Vehicles, machinery, and equipment |

20a |

|||||

11 |

Contract labor (see instructions) |

11 |

|

b |

Other business property . . . |

20b |

|||||

12 |

Depletion |

12 |

|

21 |

Repairs and maintenance . . . |

21 |

|

||||

13 |

Depreciation and section 179 |

|

|

22 |

Supplies (not included in Part III) . |

22 |

|

||||

|

expense |

deduction |

(not |

|

|

|

|||||

|

|

|

23 |

Taxes and licenses |

23 |

|

|||||

|

included in Part III) (see |

|

|

|

|||||||

|

instructions) . . . . |

13 |

|

24 |

Travel and meals: |

|

|

||||

14 |

Employee benefit programs |

|

|

a |

Travel |

24a |

|||||

|

(other than on line 19) |

. |

14 |

|

b |

Deductible meals (see instructions) |

24b |

||||

15 |

Insurance (other than health) |

15 |

|

25 |

Utilities |

25 |

|

||||

16 |

Interest (see instructions): |

|

|

26 |

Wages (less employment credits) |

26 |

|

||||

a |

Mortgage (paid to banks, etc.) |

16a |

|

27a |

Energy efficient commercial bldgs |

|

|

||||

b |

Other |

16b |

|

|

deduction (attach Form 7205) . . |

27a |

|||||

17 |

Legal and professional services |

17 |

|

b |

Other expenses (from line 48) . . |

27b |

|||||

28 |

Total expenses before expenses for business use of home. Add lines 8 through 27b |

28 |

|

||||||||

29 |

Tentative profit or (loss). Subtract line 28 from line 7 |

. . . . . . . . . . . |

29 |

|

|||||||

30Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method. See instructions.

Simplified method filers only: Enter the total square footage of (a) your home:

|

and (b) the part of your home used for business: |

|

|

. Use the Simplified |

|

|

|

|

Method Worksheet in the instructions to figure the amount to enter on line 30 |

. . |

30 |

|

|||

31 |

Net profit or (loss). Subtract line 30 from line 29. |

|

|

} |

|

|

|

|

• If a profit, enter on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you |

|

|

||||

|

checked the box on line 1, see instructions.) Estates and trusts, enter on Form 1041, line 3. |

31 |

|

||||

|

• If a loss, you must go to line 32. |

|

|

|

|

||

32 |

If you have a loss, check the box that describes your investment in this activity. See instructions. |

} |

|

|

|||

|

• If you checked 32a, enter the loss on both Schedule 1 (Form 1040), line 3, and on Schedule |

32a |

All investment is at risk. |

||||

|

SE, line 2. (If you checked the box on line 1, see the line 31 instructions.) Estates and trusts, enter on |

||||||

|

Form 1041, line 3. |

|

|

32b |

Some investment is not |

||

|

• If you checked 32b, you must attach Form 6198. Your loss may be limited. |

|

|

at risk. |

|||

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11334P |

Schedule C (Form 1040) 2025 Created 4/3/25 |

|||||

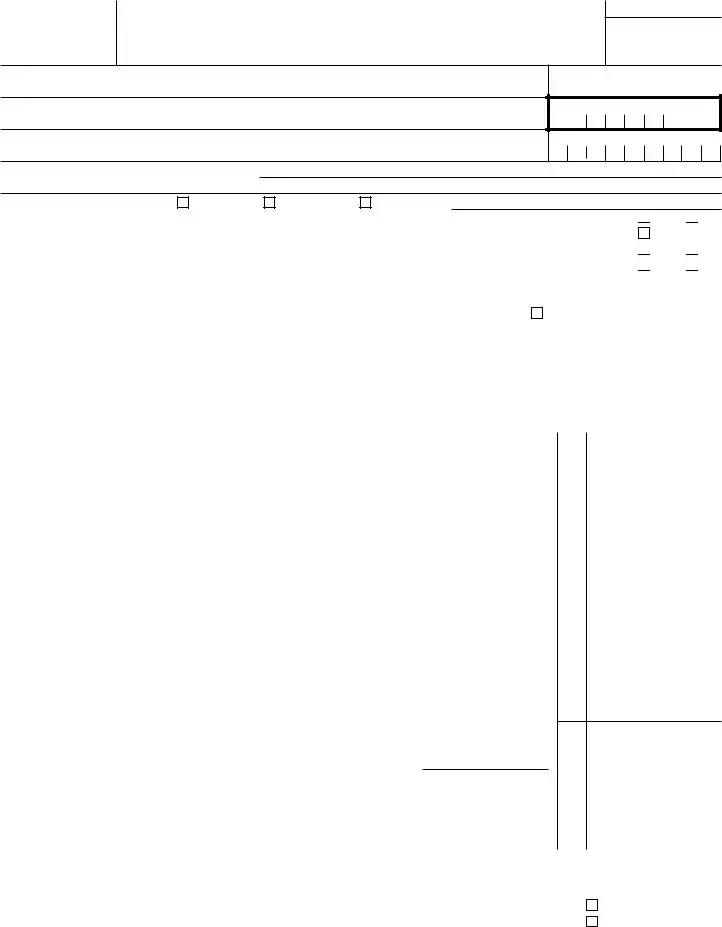

Schedule C (Form 1040) 2025 |

Page 2 |

|

Part III |

Cost of Goods Sold (see instructions) |

|

33 |

Method(s) used to |

|

|

|

|

|

|

|

value closing inventory: |

a |

Cost |

b |

Lower of cost or market |

c |

Other (attach explanation) |

34Was there any change in determining quantities, costs, or valuations between opening and closing inventory?

If “Yes,” attach explanation |

Yes |

No

35 |

Inventory at beginning of year. If different from last year’s closing inventory, attach explanation . . . |

35 |

36 |

Purchases less cost of items withdrawn for personal use |

36 |

37 |

Cost of labor. Do not include any amounts paid to yourself |

37 |

38 |

Materials and supplies |

38 |

39 |

Other costs |

39 |

40 |

Add lines 35 through 39 |

40 |

41 |

Inventory at end of year |

41 |

42 |

Cost of goods sold. Subtract line 41 from line 40. Enter the result here and on line 4 |

42 |

Part IV Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 and are not required to file Form 4562 for this business. See the instructions for line 13 to find out if you must file Form 4562.

43 |

When did you place your vehicle in service for business purposes? (month/day/year) |

/ |

/ |

44Of the total number of miles you drove your vehicle during 2025, enter the number of miles you used your vehicle for:

a Business |

b Commuting (see instructions) |

c Other |

45 Was your vehicle available for personal use during

46 Do you (or your spouse) have another vehicle available for personal use?. . . . . . . . . . . . . .

47a Do you have evidence to support your deduction? . . . . . . . . . . . . . . . . . . . .

b If “Yes,” is the evidence written? . . . . . . . . . . . . . . . . . . . . . . . . .

Part V Other Expenses. List below business expenses not included on lines

Yes

Yes

Yes

Yes

No

No

No

No

48 |

Total other expenses. Enter here and on line 27b |

48

Schedule C (Form 1040) 2025

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule C (Form 1040) is used by sole proprietors to report income or loss from a business they operated or a profession they practiced. |

| Filing Requirement | Taxpayers must file Schedule C if they earned income from self-employment, typically if their net earnings are $400 or more. |

| Deductible Expenses | Various business expenses can be deducted, including costs for supplies, advertising, and home office expenses, which can reduce taxable income. |

| Net Profit or Loss | After calculating total income and expenses, taxpayers will report their net profit or loss, which is then transferred to Form 1040. |

| State-Specific Forms | Many states have their own forms for reporting self-employment income, governed by state tax laws. For example, California uses Form 540 for individual income tax. |

| Deadline | The deadline for filing Schedule C is typically April 15, aligning with the due date for individual income tax returns. |

Filling out the IRS Schedule C (Form 1040) is an essential step for self-employed individuals and sole proprietors to report income and expenses from their business. Completing this form accurately ensures that you provide the IRS with the necessary information about your business activities. The following steps will guide you through the process of filling out the form.

After completing the Schedule C form, review all entries for accuracy. Make sure to keep a copy for your records and submit it along with your Form 1040 by the tax deadline. This process will help ensure that you meet your tax obligations while accurately reporting your business income and expenses.

What is IRS Schedule C?

IRS Schedule C is a form used by sole proprietors to report income or loss from their business. It is part of the individual income tax return, Form 1040. This form allows self-employed individuals to detail their business earnings, expenses, and net profit or loss, which ultimately affects their overall tax liability.

Who needs to file Schedule C?

Any individual who operates a business as a sole proprietor must file Schedule C. This includes freelancers, independent contractors, and anyone earning income from a business that is not incorporated. If your business earns more than $400 in net income, you are required to file this form.

What types of income should be reported on Schedule C?

All income generated from your business activities must be reported on Schedule C. This includes sales revenue, commissions, fees, and any other income related to your business operations. Even if you receive cash payments, they must be reported. Accurate reporting is crucial to avoid potential penalties.

What expenses can I deduct on Schedule C?

Schedule C allows for various deductions that can reduce your taxable income. Common deductible expenses include costs related to supplies, advertising, business travel, home office expenses, and professional fees. It’s essential to keep detailed records and receipts to substantiate these expenses in case of an audit.

How do I calculate my net profit or loss on Schedule C?

To calculate your net profit or loss, subtract your total business expenses from your total business income. If your income exceeds your expenses, you will report a profit. Conversely, if your expenses exceed your income, you will report a loss. This figure is then transferred to your Form 1040.

What happens if I have a loss on Schedule C?

If you report a loss on Schedule C, it can offset other income you have, such as wages or salaries, potentially lowering your overall tax bill. However, if your losses are consistent over several years, the IRS may scrutinize your business activities to determine if they are legitimate or considered a hobby.

Where can I find more information about filling out Schedule C?

The IRS provides detailed instructions for completing Schedule C on its official website. Additionally, you can find resources through tax professionals or accounting software that can guide you through the process. It’s advisable to seek assistance if you have questions or complex situations to ensure compliance with tax laws.

Failing to report all income. It’s important to include every source of income related to your business. Missing even a small amount can lead to issues with the IRS.

Incorrectly categorizing expenses. Make sure to classify your expenses accurately. Misclassifying can result in denied deductions.

Not keeping adequate records. Good record-keeping is essential. Without proper documentation, you may struggle to substantiate your claims if audited.

Omitting the business name and address. This information is crucial for identification. Double-check that it’s filled out correctly.

Ignoring self-employment tax. Remember, self-employment tax applies to net earnings. Be sure to calculate this correctly to avoid surprises.

Not using the correct form version. Always use the latest version of the Schedule C form. Using an outdated form can lead to errors.

Forgetting to sign and date the form. A signature is necessary for the form to be valid. Ensure this step isn’t overlooked.

Neglecting to consult a tax professional when needed. If your situation is complex, seeking help can save time and prevent mistakes.

When filing taxes as a sole proprietor, the IRS Schedule C (Form 1040) is a key document. However, it is often accompanied by several other forms and documents that provide additional information and support for your tax return. Here is a list of commonly used forms and documents that may be necessary alongside Schedule C.

Understanding these forms and documents is crucial for accurate and compliant tax filing. Each one plays a specific role in ensuring that your tax return reflects your financial situation correctly. Taking the time to gather and prepare these documents can lead to a smoother filing process and help avoid potential issues with the IRS.

The IRS Schedule C (Form 1040) is similar to the IRS Schedule E (Form 1040), which is used for reporting income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and more. Both forms are filed by individuals who are self-employed or have income from pass-through entities. While Schedule C focuses on business income and expenses, Schedule E captures income from investments and passive activities, allowing taxpayers to report various sources of income on their individual tax returns.

Another document akin to Schedule C is the IRS Schedule F (Form 1040), which is specifically for reporting farm income and expenses. Like Schedule C, Schedule F allows farmers to detail their income and deduct allowable expenses related to their farming operations. Both forms require a breakdown of income sources and expenses, reflecting the unique nature of the taxpayer's business activities, whether in general business or agriculture.

The IRS Form 1065 is a partnership return that shares similarities with Schedule C, as both require the reporting of income and expenses. However, Form 1065 is used by partnerships to report their financial activity, while Schedule C is for sole proprietors. Each document provides a means to calculate net income, but Form 1065 also includes a Schedule K-1, which details each partner's share of income, deductions, and credits, ultimately passing that information to individual partners for their personal tax returns.

IRS Form 1120, the corporate tax return, also bears resemblance to Schedule C. Both forms are used to report income and expenses, but Form 1120 is for corporations, while Schedule C is for sole proprietorships. Corporations must adhere to different tax rates and regulations compared to sole proprietors. Despite these differences, both forms require a detailed accounting of income and allowable deductions to determine the taxable amount.

IRS Form 1065 and Schedule K-1 are closely related to Schedule C. While Schedule C is for individuals reporting self-employment income, Form 1065 is for partnerships, and Schedule K-1 provides each partner with their share of the partnership’s income, deductions, and credits. This information is then reported on the partners' individual tax returns, similar to how sole proprietors report their business income on Schedule C.

IRS Form 990 is another document that resembles Schedule C, particularly for non-profit organizations. Both forms require detailed financial reporting, but Form 990 is specifically for tax-exempt organizations, requiring them to disclose their revenue, expenses, and activities. While the purpose of Form 990 is different, the structure of reporting income and expenses is similar, emphasizing transparency in financial operations.

Schedule C also shares characteristics with IRS Form 1040-X, the amended return. While Schedule C is used to report income and expenses for a business, Form 1040-X allows taxpayers to correct errors on their previously filed tax returns, including adjustments related to business income reported on Schedule C. Both documents require careful attention to detail to ensure accuracy in financial reporting.

IRS Form 941, the Employer's Quarterly Federal Tax Return, is another document that has a connection to Schedule C. While Schedule C is for self-employed individuals, Form 941 is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. Both forms involve financial reporting, but they serve different purposes in the realm of taxation, with Schedule C focusing on self-employment income and Form 941 on employer obligations.

Finally, IRS Form 1099-MISC and Schedule C are related in that both deal with income reporting. Form 1099-MISC is used by businesses to report payments made to non-employees, such as independent contractors. When a self-employed individual receives a 1099-MISC, they must report that income on Schedule C. Both forms emphasize the importance of accurately reporting income received in various forms, reflecting the taxpayer's overall financial situation.

When filling out the IRS Schedule C (Form 1040), which is used for reporting income or loss from a business you operated or a profession you practiced as a sole proprietor, it is essential to approach the task with care. Here are ten important dos and don'ts to consider:

Understanding the IRS Schedule C 1040 form is crucial for self-employed individuals and small business owners. However, several misconceptions can lead to confusion. Here are seven common misunderstandings:

This is incorrect. Even sole proprietors without employees must file Schedule C to report their business income and expenses.

While most income related to your business should be reported, there are exceptions, such as income from investments or other non-business activities.

While keeping receipts is important, you can also use other documentation, like bank statements, to support your expense claims.

Filing Schedule C does not automatically trigger an audit. The IRS selects returns for audit based on various risk factors, not solely on the form filed.

This is misleading. Some indirect expenses, like a portion of your home office or car expenses, can also be deducted if they are used for business purposes.

While it is primarily used by sole proprietors, single-member LLCs also file Schedule C to report business income and expenses.

This is false. You can change your business structure at any time, but it may have tax implications that you should consider.

Clearing up these misconceptions can help ensure accurate reporting and compliance with tax regulations.

When filling out and using the IRS Schedule C (Form 1040), it's essential to understand the key elements that can impact your tax filing. Here are some important takeaways: