The IRS Schedule B (Form 941) plays a crucial role for employers in managing their payroll taxes. This form is used to report the amount of federal income tax withheld from employees' wages, along with the employer's share of Social Security and Medicare taxes. It is essential for businesses to accurately complete this form to ensure compliance with federal tax laws and avoid potential penalties. Schedule B is particularly important for employers who have a large payroll or who have made adjustments to their tax liabilities during the quarter. By providing detailed information about tax deposits, this form helps the IRS track whether employers are meeting their tax obligations. Understanding the nuances of Schedule B is vital for maintaining good standing with the IRS and ensuring smooth payroll operations.

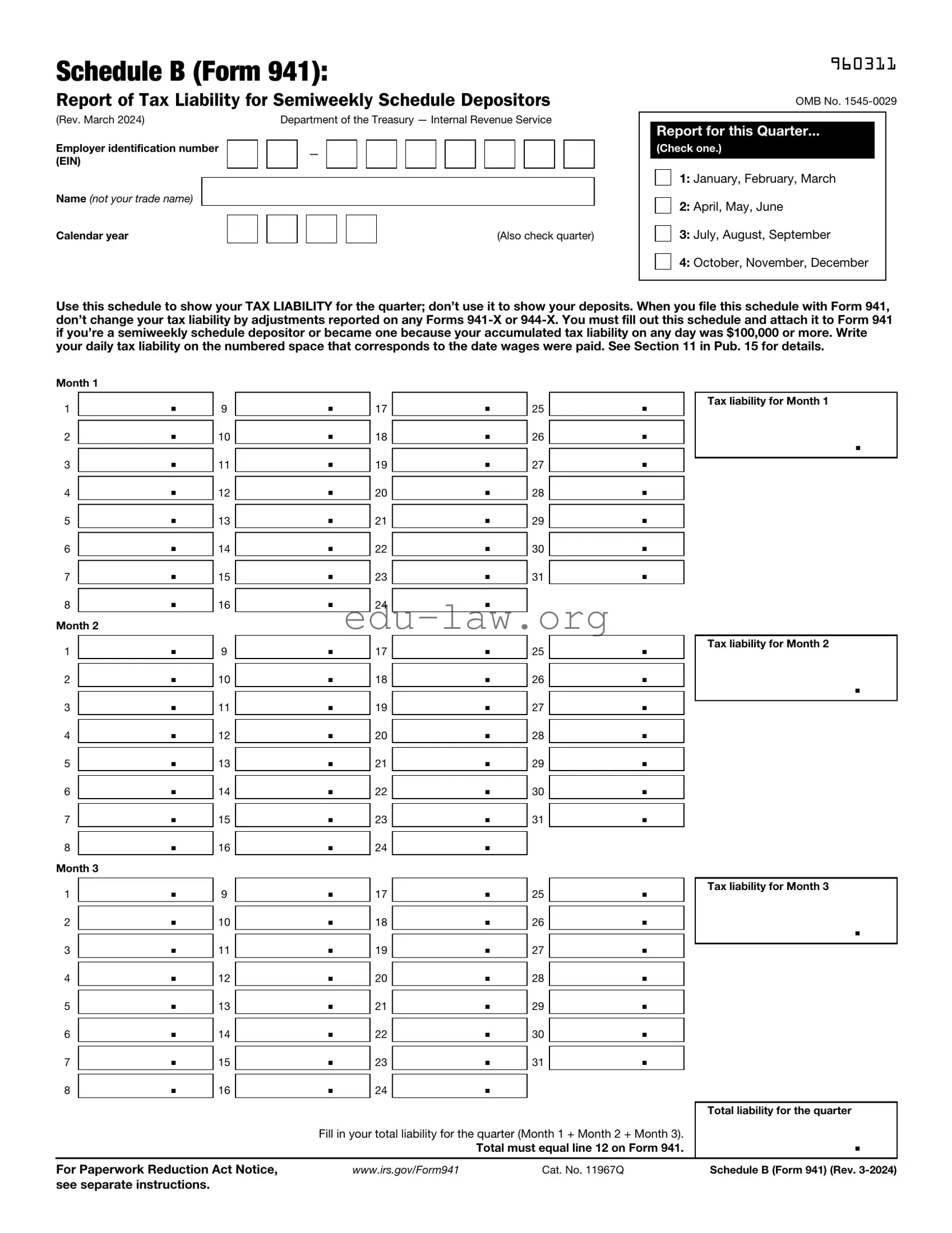

Schedule B (Form 941):

Report of Tax Liability for Semiweekly Schedule Depositors

(Rev. March 2024) |

|

|

Department of the Treasury — Internal Revenue Service |

|||||||||||||||||||

Employer identification number |

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Also check quarter) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

960311

OMB No.

Report for this Quarter...

(Check one.)

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Use this schedule to show your TAX LIABILITY for the quarter; don’t use it to show your deposits. When you file this schedule with Form 941, don’t change your tax liability by adjustments reported on any Forms

Month 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 1 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

Month 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 2 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

Month 3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 3 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liability for the quarter |

|

|

|

|

|

Fill in your total liability for the quarter (Month 1 + Month 2 + Month 3). |

|

. |

|||||||

|

|

|

|

|

|

|

|

|

Total must equal line 12 on Form 941. |

|

||||

For Paperwork Reduction Act Notice, |

|

www.irs.gov/Form941 |

|

Cat. No. 11967Q |

|

|

Schedule B (Form 941) (Rev. |

|||||||

see separate instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

||

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule B (Form 941) is used by employers to report their federal income tax withheld from employees and to report their share of Social Security and Medicare taxes. |

| Filing Frequency | This form must be filed quarterly by employers who are required to report payroll taxes. |

| Due Dates | Employers must submit Schedule B along with Form 941 by the last day of the month following the end of the quarter. |

| State-Specific Requirements | Employers may need to comply with state-specific payroll tax laws, which can vary. Check local regulations for additional forms or requirements. |

After gathering the necessary information, you are ready to fill out the IRS Schedule B (Form 941). This form is essential for reporting your employment taxes. Following these steps will help ensure that you complete it accurately.

Once you have filled out the form, review it for accuracy before submitting it to the IRS. Proper completion is crucial for compliance and to avoid potential penalties.

What is IRS Schedule B (Form 941)?

IRS Schedule B (Form 941) is a supplemental form used by employers to report their tax liability for federal income tax withheld and for Social Security and Medicare taxes. This form provides detailed information on the amount of taxes that were withheld from employee paychecks and is typically filed alongside Form 941, which is the Employer's Quarterly Federal Tax Return.

Who needs to file Schedule B?

Employers who accumulate a tax liability of $100,000 or more on any day during the deposit period must file Schedule B. This applies to both large and small employers. If your business has a high payroll or withholds a significant amount of taxes, it is crucial to include this form to ensure compliance with IRS regulations.

When is Schedule B due?

Schedule B is due at the same time as Form 941. Employers must file Form 941 quarterly, and the due dates for these filings are typically the last day of the month following the end of each quarter. For example, for the first quarter ending March 31, the due date is April 30. It’s essential to adhere to these deadlines to avoid penalties.

How do I complete Schedule B?

To complete Schedule B, you will need to provide information about your tax liability for each month of the quarter. This includes the total amount of taxes withheld, Social Security, and Medicare taxes. You will also need to indicate any adjustments or corrections from previous filings. Make sure to double-check all figures for accuracy to avoid complications with the IRS.

What happens if I don’t file Schedule B?

If you are required to file Schedule B but fail to do so, the IRS may impose penalties. These can include fines for late filing or failure to file altogether. Additionally, not filing can lead to an inaccurate representation of your tax liability, which could result in further scrutiny from the IRS.

Can I file Schedule B electronically?

Yes, you can file Schedule B electronically if you are using IRS-approved e-file software or services. Electronic filing can help streamline the process and reduce the likelihood of errors. It also allows for faster processing and confirmation of your submission.

What if I make a mistake on Schedule B?

If you discover an error after submitting Schedule B, you should correct it as soon as possible. You can do this by filing an amended Form 941. Be sure to include an explanation of the changes made. Timely corrections can help prevent penalties and ensure your records are accurate.

Where can I find the latest version of Schedule B?

The latest version of Schedule B (Form 941) can be found on the IRS website. It is important to use the most current form, as tax laws and regulations can change. Always check for updates before filing to ensure compliance with the latest requirements.

Is assistance available for completing Schedule B?

Yes, assistance is available for completing Schedule B. Many tax professionals, accountants, and payroll services can help guide you through the process. Additionally, the IRS website offers resources and instructions for filling out the form. Don’t hesitate to seek help if you have questions or concerns.

Not including all required information. Ensure that every section is filled out completely. Missing details can lead to delays or rejections.

Incorrectly calculating tax liabilities. Double-check your math. Errors in calculations can result in underpayment or overpayment of taxes.

Failing to report all employees. Every employee that received wages must be included. Omitting employees can raise red flags with the IRS.

Using outdated forms. Always use the latest version of the Schedule B 941 form. Using an old form can lead to compliance issues.

Not signing the form. A signature is mandatory. Without it, the form is considered incomplete and invalid.

Ignoring deadlines. Submit your form on time to avoid penalties. Late submissions can incur additional fees and interest.

Not keeping copies of submitted forms. Always retain a copy for your records. This can be helpful for future reference or in case of an audit.

Overlooking instructions. Each section has specific guidelines. Take the time to read through the instructions carefully to avoid mistakes.

The IRS Schedule B (Form 941) is used by employers to report the number of employees and the amount of federal income tax withheld. It is important to have other forms and documents ready when filing this form to ensure compliance with tax regulations. Below is a list of commonly used forms and documents that may accompany Schedule B.

Having these forms and documents ready can help streamline the filing process and ensure that all necessary information is reported accurately. Always check for the latest updates from the IRS to confirm requirements and deadlines.

The IRS Schedule B (Form 941) is a vital document for employers who report their payroll taxes. It is similar to the IRS Form 940, which is the Employer's Annual Federal Unemployment (FUTA) Tax Return. While Form 941 is filed quarterly to report income taxes, Social Security tax, and Medicare tax withheld from employee wages, Form 940 is an annual report that focuses on unemployment taxes. Both forms are essential for compliance with federal tax laws and ensure that employers meet their obligations to the IRS.

Another document that shares similarities with Schedule B is the IRS Form W-2. This form is used to report wages paid to employees and the taxes withheld from them. While Schedule B provides a breakdown of tax liabilities for the quarter, Form W-2 summarizes an employee's annual earnings and tax withholdings. Both documents are crucial for accurate tax reporting and play a role in an employee's tax return, ensuring that individuals receive proper credit for taxes paid throughout the year.

The IRS Form 1099 is also comparable to Schedule B, particularly in the context of reporting income. While Schedule B focuses on payroll taxes for employees, Form 1099 is used to report payments made to independent contractors and other non-employees. Both forms require accurate reporting to the IRS to prevent discrepancies and potential penalties. They serve to inform the IRS about different types of income and the corresponding taxes owed.

Form 941 is akin to the IRS Form 944, which is the Employer's Annual Federal Tax Return. Form 944 is designed for smaller employers with a lower payroll tax liability, allowing them to file annually instead of quarterly. Both forms require similar information regarding employee wages and taxes withheld, but the filing frequency differs based on the employer's size and tax obligations. This distinction helps streamline the reporting process for small businesses.

The IRS Form 720 is another document that shares some similarities with Schedule B. Form 720 is used to report and pay federal excise taxes, which can include taxes on certain goods and services. While Schedule B focuses on payroll taxes, both forms require detailed reporting and timely submission to avoid penalties. They are essential tools for ensuring compliance with federal tax laws and maintaining accurate records of tax liabilities.

Additionally, the IRS Form 8862 is relevant in this context as it relates to the Earned Income Tax Credit (EITC). While not directly similar in purpose to Schedule B, both forms involve tax compliance and reporting. Form 8862 is used by individuals who have previously been denied the EITC and wish to claim it again. Accurate reporting on all relevant forms, including Schedule B, is crucial for individuals and businesses to ensure they receive the credits and deductions they are entitled to.

Lastly, the IRS Form 945 is comparable to Schedule B in that it deals with federal income tax withheld from nonpayroll payments. This form is used to report backup withholding and other payments that do not fall under traditional payroll tax reporting. Both forms require accurate calculations and timely submissions to the IRS, ensuring that all tax obligations are met and reducing the risk of audits or penalties.

When filling out the IRS Schedule B (Form 941), it’s important to approach the task with care. Here are some essential do's and don'ts to keep in mind:

By following these guidelines, you can ensure that your Schedule B is filled out correctly, helping to avoid unnecessary complications with the IRS.

Understanding the IRS Schedule B (Form 941) can be challenging. Here are nine common misconceptions about this form, clarified for better comprehension.

This is not true. Any employer who is required to file Form 941 must also complete Schedule B if they meet certain criteria, regardless of their size.

While wages are a significant part of the form, Schedule B is primarily used to report the tax liability for federal income tax withheld and Social Security and Medicare taxes.

This is a misconception. If you are required to file Form 941, you must also file Schedule B, even if there is no tax liability.

This is incorrect. Schedule B is specifically tied to Form 941, which is filed quarterly, but it is not limited to just that timeframe.

All employees, including part-time and seasonal workers, must be included when calculating tax liabilities on Schedule B.

This is a misunderstanding. Electronic filing does not exempt you from completing Schedule B if it is required.

Even if you are a sole proprietor or a business owner without traditional employees, Schedule B may still apply if you have other tax liabilities.

This is false. If you meet the filing requirements, you must complete and submit Schedule B along with your Form 941.

Not all tax liabilities are reported here. Schedule B is specifically for federal tax liabilities related to wages, not for other types of taxes.

By addressing these misconceptions, you can ensure that you complete the IRS Schedule B accurately and avoid potential penalties.

Filling out and using the IRS Schedule B (Form 941) is essential for employers who need to report their tax liabilities accurately. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can ensure compliance and streamline your payroll tax reporting process.