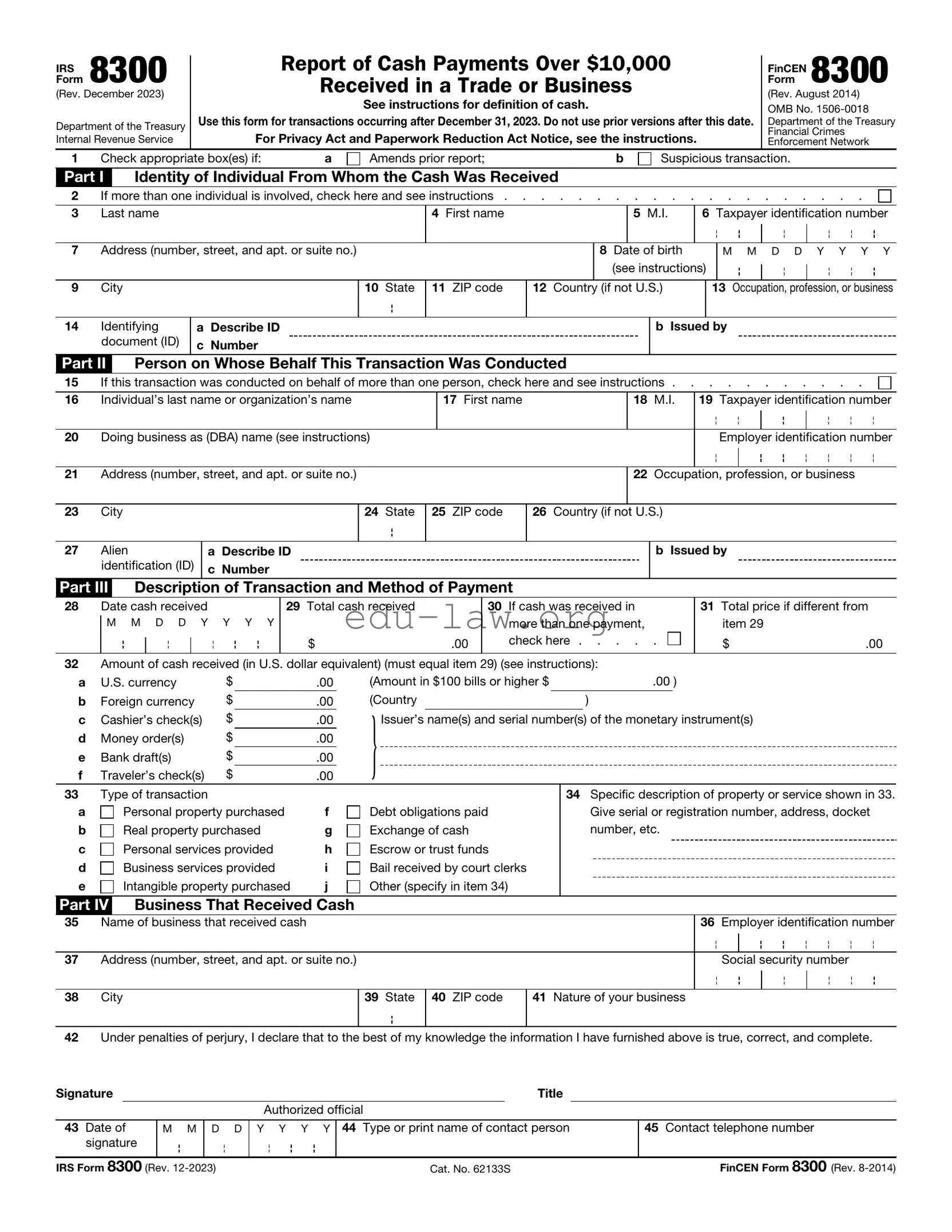

When it comes to large cash transactions, understanding the IRS Form 8300 is crucial for both businesses and individuals. This form plays a significant role in reporting any cash payments exceeding $10,000 received in a single transaction or a series of related transactions. The primary aim is to combat money laundering and tax evasion, making compliance essential for maintaining the integrity of financial systems. Notably, the form requires detailed information, including the identity of the payer, the amount received, and the nature of the transaction. Failure to file or incorrect reporting can lead to hefty penalties, making it imperative for businesses to be vigilant. Additionally, certain exemptions and nuances exist, which can impact how and when the form should be filed. Understanding these elements not only helps in adhering to legal requirements but also fosters transparency in financial dealings.

IRS 8300

Form

(Rev. December 2023)

Department of the Treasury Internal Revenue Service

Report of Cash Payments Over $10,000

Received in a Trade or Business

See instructions for definition of cash.

Use this form for transactions occurring after December 31, 2023. Do not use prior versions after this date.

For Privacy Act and Paperwork Reduction Act Notice, see the instructions.

FinCEN 8300 Form

(Rev. August 2014)

OMB No.

Department of the Treasury

Financial Crimes

Enforcement Network

1 Check appropriate box(es) if: |

a |

Amends prior report; |

b |

Part I Identity of Individual From Whom the Cash Was Received

Suspicious transaction.

2 |

If more than one individual is involved, check here and see instructions |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Last name |

|

4 First name |

|

|

5 M.I. |

6 Taxpayer identification number |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

|

8 Date of birth |

|

|

M M D D Y Y Y Y |

|||

|

|

|

|

|

(see instructions) |

|

|||||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||

9 |

City |

10 State |

11 ZIP code |

12 Country |

(if not U.S.) |

|

13 Occupation, profession, or business |

||||

|

|

|

|

|

|

|

|

|

|

|

|

14 Identifying |

a |

Describe ID |

document (ID) |

c |

Number |

Part II Person on Whose Behalf This Transaction Was Conducted

b Issued by

15 |

If this transaction was conducted on behalf of more than one person, check here and see instructions |

|||

|

|

|

|

|

16 |

Individual’s last name or organization’s name |

17 First name |

18 M.I. |

19 Taxpayer identification number |

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27 Alien |

a |

Describe ID |

identification (ID) |

c |

Number |

Part III Description of Transaction and Method of Payment

b Issued by

28Date cash received

M M D D Y Y Y Y

29Total cash received

$.00

30If cash was received in more than one payment, check here . . . . .

31Total price if different from item 29

$.00

32Amount of cash received (in U.S. dollar equivalent) (must equal item 29) (see instructions):

a |

U.S. currency |

$ |

.00 |

(Amount in $100 bills or higher $ |

.00 ) |

||||

b |

Foreign currency |

$ |

.00 |

(Country |

) |

|

|||

|

|

$ |

|

} |

|

|

|

||

c |

Cashier’s check(s) |

.00 |

Issuer’s name(s) and serial number(s) of the monetary instrument(s) |

||||||

d |

Money order(s) |

$ |

.00 |

|

|

|

|

|

|

e |

Bank draft(s) |

$ |

.00 |

|

|

|

|

|

|

f |

Traveler’s check(s) |

$ |

.00 |

|

|

|

|

|

|

33Type of transaction

a |

Personal property purchased |

f |

b |

Real property purchased |

g |

c |

Personal services provided |

h |

d |

Business services provided |

i |

e |

Intangible property purchased |

j |

Part IV |

Business That Received Cash |

|

Debt obligations paid Exchange of cash Escrow or trust funds

Bail received by court clerks Other (specify in item 34)

34Specific description of property or service shown in 33. Give serial or registration number, address, docket number, etc.

35Name of business that received cash

36Employer identification number

37Address (number, street, and apt. or suite no.)

Social security number

38City

39State

40ZIP code

41Nature of your business

42Under penalties of perjury, I declare that to the best of my knowledge the information I have furnished above is true, correct, and complete.

Signature |

|

|

|

|

|

Title |

|

|

|

|

|

|

Authorized official |

|

|

||

|

|

|

|

|

|

|

||

43 Date of |

M M |

D D |

Y Y Y Y |

44 Type or print name of contact person |

|

45 Contact telephone number |

||

signature |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

IRS Form 8300 (Rev. |

|

Cat. No. 62133S |

|

FinCEN Form 8300 (Rev. |

||||

IRS Form 8300 (Rev. |

Page 2 |

FinCEN Form 8300 (Rev. |

Multiple Parties

(Complete applicable parts below if box 2 or 15 on page 1 is checked.)

Part I

3 |

Last name |

|

|

4 First name |

|

5 M.I. |

6 Taxpayer identification number |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

8 |

Date of birth |

|

M M D D Y Y Y Y |

|||||

|

|

|

|

|

|

|

(see instructions) |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

City |

10 State |

11 ZIP code |

|

12 Country (if not U.S.) |

|

13 Occupation, profession, or business |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Last name |

|

|

4 First name |

|

5 M.I. |

6 Taxpayer identification number |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Address (number, street, and apt. or suite no.) |

|

|

8 |

Date of birth |

|

M M D D Y Y Y Y |

|||||

|

|

|

|

|

|

|

(see instructions) |

|

||||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

City |

10 State |

11 ZIP code |

|

12 Country (if not U.S.) |

|

13 Occupation, profession, or business |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

14Identifying document (ID)

aDescribe ID c Number

b Issued by

Part II

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

16Individual’s last name or organization’s name

17First name

18M.I.

19Taxpayer identification number

20Doing business as (DBA) name (see instructions)

Employer identification number

21Address (number, street, and apt. or suite no.)

22Occupation, profession, or business

23City

24State

25ZIP code

26Country (if not U.S.)

27Alien identification (ID)

aDescribe ID c Number

b Issued by

Comments – Please use the lines provided below to comment on or clarify any information you entered on any line in Parts I, II, III, and IV

IRS Form 8300 (Rev. |

FinCEN Form 8300 (Rev. |

| Fact Name | Details |

|---|---|

| Purpose | The IRS 8300 form is used to report cash payments over $10,000 received in a trade or business. |

| Filing Requirement | Businesses must file the form within 15 days of receiving the cash payment. |

| Who Must File | Any business that receives more than $10,000 in cash must file this form, regardless of the type of business. |

| Cash Definition | For this form, cash includes currency and certain negotiable instruments, such as money orders. |

| Penalties | Failure to file the IRS 8300 can result in significant penalties, including fines. |

| Privacy | The information provided on the form is confidential and protected under federal law. |

| State-Specific Forms | Some states have their own reporting requirements for cash transactions. For example, California has the California Business and Professions Code, Section 21600. |

| Record Keeping | Businesses must keep copies of filed forms and related documents for at least five years. |

| Filing Method | The form can be filed electronically or submitted via mail to the IRS. |

| Additional Information | For more details, businesses can refer to IRS Publication 1544, which provides guidance on reporting cash payments. |

After completing the IRS 8300 form, you will need to submit it to the IRS to report cash payments exceeding $10,000 received in a single transaction or related transactions. Make sure to keep a copy for your records. Following the steps below will help ensure that you fill out the form accurately.

What is the IRS 8300 form?

The IRS 8300 form is used to report cash payments over $10,000 received in a trade or business. This includes payments made in cash, cashier’s checks, money orders, and other forms of cash equivalents. Businesses must file this form to help the government track large cash transactions and prevent money laundering.

Who needs to file the IRS 8300 form?

If you are a business owner or operator and receive more than $10,000 in cash from a single transaction or related transactions, you are required to file this form. This applies to various types of businesses, including retail stores, car dealerships, and any service providers that deal in cash payments.

When is the IRS 8300 form due?

The IRS 8300 form must be filed within 15 days of receiving the cash payment. If the 15th day falls on a weekend or holiday, you should file it on the next business day. Timely filing is essential to avoid penalties.

What information is required on the IRS 8300 form?

You will need to provide several details on the form, including your business name, address, and Employer Identification Number (EIN). You must also include information about the individual or entity making the cash payment, such as their name, address, and taxpayer identification number. Additionally, you will need to describe the transaction and the amount received.

What happens if I fail to file the IRS 8300 form?

Failing to file the IRS 8300 form can lead to significant penalties. The IRS may impose fines for late filing, and if the failure is deemed willful, the penalties can be even more severe. It is important to comply with this requirement to avoid potential legal and financial consequences.

Can I file the IRS 8300 form electronically?

Yes, you can file the IRS 8300 form electronically using the IRS e-file system. This option can make the filing process easier and faster. However, if you prefer to file by mail, you can still do so by sending the completed form to the appropriate IRS address.

Where can I find more information about the IRS 8300 form?

For more information, you can visit the IRS website. They provide detailed instructions and resources related to the IRS 8300 form. You may also consider consulting with a tax professional if you have specific questions or need assistance with the filing process.

Incorrect Identification Information: Many people fail to provide accurate identification details. This includes the name, address, and taxpayer identification number. A simple typo can lead to significant delays or issues with the IRS.

Missing Required Signatures: Some individuals neglect to sign the form. Without a signature, the IRS will not process the form, and this can lead to penalties for failing to report cash transactions properly.

Not Reporting All Cash Transactions: Individuals sometimes only report a portion of the cash received. It's crucial to report all cash transactions that exceed $10,000. Failing to do so can raise red flags with the IRS.

Improper Filing Method: Some people choose to file the form incorrectly. Whether submitting it electronically or by mail, following the IRS guidelines is essential. Incorrect filing can lead to processing delays.

Ignoring Deadlines: Missing the deadline for filing the IRS 8300 form can result in penalties. It's important to be aware of the timelines and ensure that the form is submitted on time to avoid unnecessary fines.

The IRS Form 8300 is used to report cash payments over $10,000 received in a trade or business. When filing this form, several other documents may also be relevant. These documents help provide additional context or support for the information reported on Form 8300. Below is a list of other forms and documents commonly used in conjunction with the IRS 8300 form.

Using these documents alongside the IRS Form 8300 can help ensure compliance with tax regulations and provide a clearer picture of cash transactions. Keeping accurate records is essential for any business handling significant cash payments.

The IRS Form 1099 is a crucial document used to report various types of income other than wages, salaries, and tips. Similar to Form 8300, which reports cash transactions over $10,000, Form 1099 also serves as a tool for transparency in financial transactions. Businesses must issue Form 1099 to independent contractors or freelancers who earn $600 or more in a year. Both forms aim to ensure that the IRS receives accurate information about income, helping to prevent tax evasion.

Form 1040, the individual income tax return, is another important document in the tax landscape. While Form 8300 focuses on large cash transactions, Form 1040 encompasses a broader range of income and deductions for individuals. Taxpayers report their total income, including any amounts reported on Form 1099, on Form 1040. The connection between these forms lies in their shared goal of ensuring that all income is reported and taxed appropriately.

Form 945 is used to report annual withholding on nonpayroll payments, such as pensions and annuities. Like Form 8300, it is concerned with reporting significant financial transactions to the IRS. While Form 8300 deals with cash payments over $10,000, Form 945 focuses on the tax withheld from payments made to individuals. Both forms are essential for maintaining compliance with tax laws and ensuring that the IRS can track and collect the appropriate taxes.

Form 1065, the partnership return, is another document that shares similarities with Form 8300. This form is used to report income, deductions, gains, and losses from partnerships. While Form 8300 is focused on cash transactions, Form 1065 requires partnerships to report their financial activities, including any cash transactions that may exceed the $10,000 threshold. Both forms highlight the importance of transparency in financial dealings and the need for accurate reporting to the IRS.

Lastly, Form 990 is a tax form used by tax-exempt organizations to provide the IRS with information about their activities, governance, and finances. Similar to Form 8300, which tracks significant cash transactions, Form 990 helps the IRS monitor organizations to ensure they comply with tax regulations. Both forms are vital for promoting accountability and transparency in financial reporting, albeit in different contexts.

When it comes to filling out the IRS 8300 form, clarity and accuracy are key. This form is used to report cash payments over $10,000 received in a trade or business. To help you navigate this process, here are some important do's and don'ts.

By following these guidelines, you can help ensure that your filing process goes smoothly and that you remain compliant with IRS regulations.

The IRS Form 8300 is used to report cash payments over $10,000 received in a trade or business. Despite its importance, several misconceptions surround this form. Here are seven common misunderstandings:

This is incorrect. Any business that receives more than $10,000 in cash from a single transaction or related transactions must file the form, regardless of size.

While the form is primarily for cash, it also applies to certain cash equivalents, such as money orders or traveler's checks, if they total over $10,000.

This is a misconception. Filing is mandatory when cash payments exceed the threshold. Failure to file can result in penalties.

In reality, Form 8300 must be filed each time a qualifying cash transaction occurs, not just annually.

The information is also shared with other agencies, such as the Financial Crimes Enforcement Network (FinCEN), to help combat money laundering.

This is false. There are penalties for late filing, which can increase the longer the form is overdue.

Many find the form straightforward. The IRS provides guidance and resources to assist businesses in completing it correctly.

Understanding these misconceptions can help businesses comply with reporting requirements and avoid potential penalties.

The IRS 8300 form is an important document for reporting cash transactions. Here are some key takeaways to keep in mind when filling it out and using it:

By following these guidelines, you can ensure compliance with IRS regulations while effectively managing cash transactions.