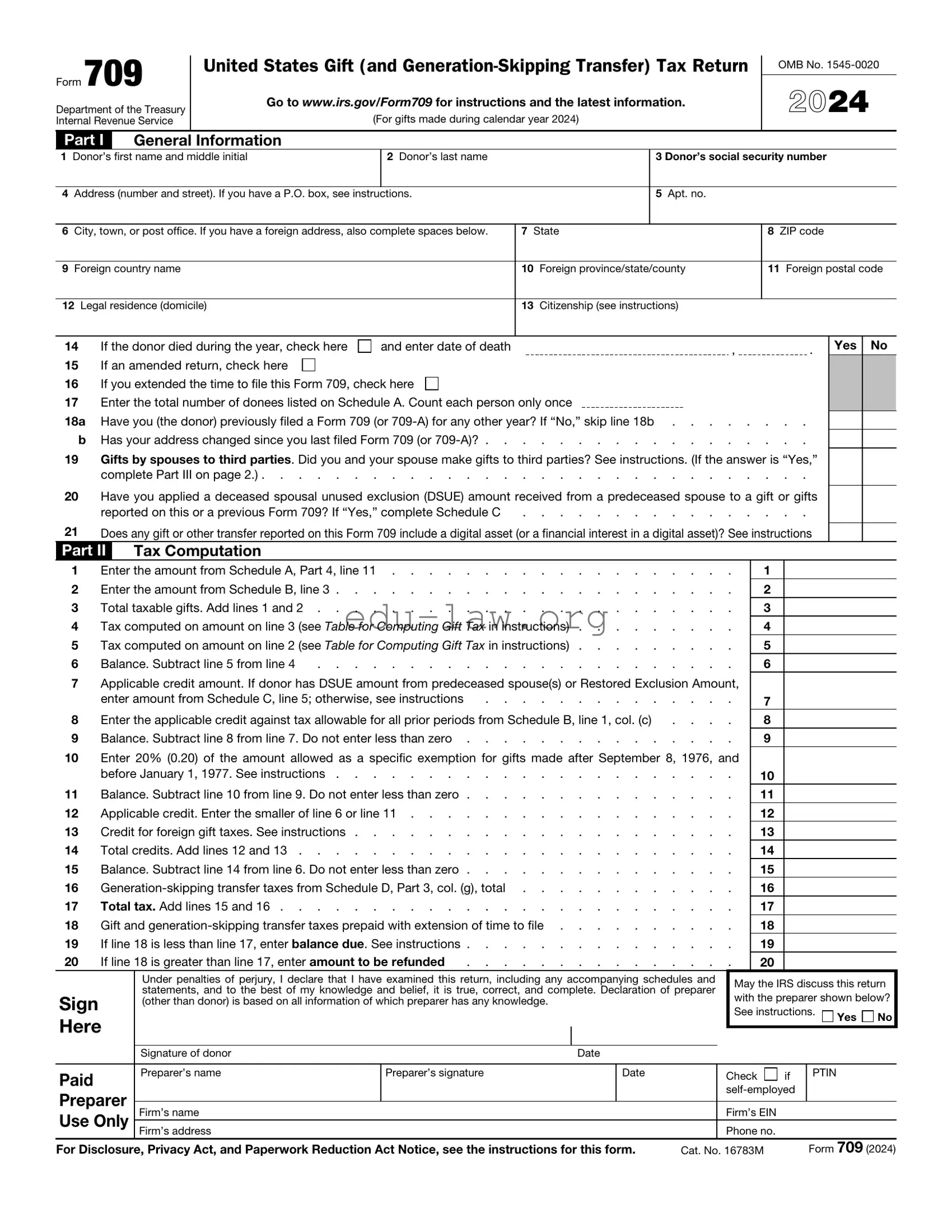

The IRS 709 form plays a crucial role in the realm of gift and generation-skipping transfer taxes, serving as a necessary tool for individuals who make substantial gifts during their lifetime. It is essential for anyone who gives gifts exceeding the annual exclusion limit, which is adjusted periodically, to report these transactions accurately. By filing this form, taxpayers not only disclose their gifts but also track their lifetime gift tax exemption. This exemption allows individuals to give away a significant amount of money without incurring taxes, promoting generosity while ensuring compliance with federal regulations. Additionally, the form requires detailed information about the recipient, the value of the gift, and any applicable deductions, making it a comprehensive document that reflects the giver's financial decisions. Understanding the nuances of the IRS 709 form is vital for effective estate planning and for minimizing potential tax liabilities. Ignoring this form could lead to unexpected tax consequences, emphasizing the importance of being informed and proactive in financial matters.

Form 709 |

United States Gift (and |

|

|

||

Department of the Treasury |

Go to www.irs.gov/Form709 for instructions and the latest information. |

|

(For gifts made during calendar year 2024) |

||

Internal Revenue Service |

Part I General Information

OMB No.

2024

1Donor’s first name and middle initial

2Donor’s last name

3 Donor’s social security number

4Address (number and street). If you have a P.O. box, see instructions.

5Apt. no.

6City, town, or post office. If you have a foreign address, also complete spaces below.

7State

8ZIP code

9Foreign country name

10Foreign province/state/county

11Foreign postal code

12Legal residence (domicile)

13Citizenship (see instructions)

14 |

If the donor died during the year, check here |

and enter date of death |

, |

. |

15 |

If an amended return, check here |

|

|

|

16 |

If you extended the time to file this Form 709, check here |

|

|

|

17Enter the total number of donees listed on Schedule A. Count each person only once

18a |

Have you (the donor) previously filed a Form 709 (or |

b |

Has your address changed since you last filed Form 709 (or |

19Gifts by spouses to third parties. Did you and your spouse make gifts to third parties? See instructions. (If the answer is “Yes,”

complete Part III on page 2.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20Have you applied a deceased spousal unused exclusion (DSUE) amount received from a predeceased spouse to a gift or gifts

reported on this or a previous Form 709? If “Yes,” complete Schedule C |

. . . . . . . . . . . . . . . . |

21Does any gift or other transfer reported on this Form 709 include a digital asset (or a financial interest in a digital asset)? See instructions

Part II Tax Computation

Yes No

1 |

Enter the amount from Schedule A, Part 4, line 11 |

|

2 |

Enter the amount from Schedule B, line 3 |

|

3 |

Total taxable gifts. Add lines 1 and 2 |

|

4 |

Tax computed on amount on line 3 (see Table for Computing Gift Tax in instructions) |

|

5 |

Tax computed on amount on line 2 (see Table for Computing Gift Tax in instructions) |

|

6 |

Balance. Subtract line 5 from line 4 |

. . . . . . . . . . . . . . . . . . . . . . . |

7Applicable credit amount. If donor has DSUE amount from predeceased spouse(s) or Restored Exclusion Amount,

|

enter amount from Schedule C, line 5; otherwise, see instructions |

. . . . . . . . . . . . . . |

|

8 |

Enter the applicable credit against tax allowable for all prior periods from Schedule B, line 1, col. (c) |

. . . . |

|

9 |

Balance. Subtract line 8 from line 7. Do not enter less than zero |

||

10Enter 20% (0.20) of the amount allowed as a specific exemption for gifts made after September 8, 1976, and

|

before January 1, 1977. See instructions |

|

11 |

Balance. Subtract line 10 from line 9. Do not enter less than zero |

|

12 |

Applicable credit. Enter the smaller of line 6 or line 11 |

|

13 |

Credit for foreign gift taxes. See instructions |

|

14 |

Total credits. Add lines 12 and 13 |

|

15 |

Balance. Subtract line 14 from line 6. Do not enter less than zero |

|

16 |

||

17 |

Total tax. Add lines 15 and 16 |

|

18 |

Gift and |

|

19 |

If line 18 is less than line 17, enter balance due. See instructions |

|

20 |

If line 18 is greater than line 17, enter amount to be refunded |

. . . . . . . . . . . . . . . |

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

|

Under penalties of perjury, I declare that I have examined this return, including any accompanying schedules and |

|

May the IRS discuss this return |

||||||||

|

statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer |

|

|||||||||

Sign |

|

with the preparer shown below? |

|||||||||

(other than donor) is based on all information of which preparer has any knowledge. |

|

|

|

|

|||||||

|

|

|

|

|

See instructions. |

|

|

||||

Here |

|

|

|

|

|

|

Yes |

No |

|||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature of donor |

|

Date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

Preparer’s name |

Preparer’s signature |

|

Date |

|

Check |

if |

PTIN |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

|

Firm’s EIN |

|

|

|

|

||

Use Only |

|

|

|

|

|

|

|

|

|||

Firm’s address |

|

|

|

|

Phone no. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|||

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see the instructions for this form. |

Cat. No. 16783M |

|

Form 709 (2024) |

||||||||

Form 709 (2024) |

|

Page 2 |

|

Part III |

Spouse’s Consent on Gifts to Third Parties |

|

|

1 Gifts by spouses to third parties. Do you consent to have the gifts (including |

Yes |

No |

|

|

|

||

by your spouse to third parties during the calendar year considered as made |

|

|

|

answer is “Yes,” the following information must be furnished. If the answer is “No,” skip lines |

|

|

|

2Name of consenting spouse

3SSN of consenting spouse

4 |

Were you married to one another during the entire calendar year? See instructions |

. . . . . . . . . . . . . |

||||

5 |

If line 4 is “No,” check whether |

married |

divorced or |

widowed/deceased, and give date. See instructions |

|

|

6 |

Will a gift tax return for this year be filed by your spouse? If “Yes,” mail both returns in the same envelope |

. . . . . . |

||||

7Consent of Spouse. Have you obtained required spousal consent for gifts made to third parties to be considered as made

Form 709 (2024)

Form 709 (2024) |

Page 3 |

SCHEDULE A Computation of Taxable Gifts (Including transfers in trust) (see instructions)

A |

Does the value of any item listed on Schedule A reflect any valuation discount? If “Yes,” attach explanation |

Yes |

No |

BIf you elect under section 529(c)(2)(B) to treat any transfers made this year to a qualified tuition program as made ratably over a

(a)

Item

number

(b)

Donee’s name and address

(c)

Relationship

to donor

(if any)

(d)

Description of gift

(e)

Donor’s

adjusted basis

of gift

(f) |

(g) |

Date of gift |

Value at |

date of gift

(h) |

(i) |

For split |

Net transfer |

gifts, enter |

(subtract col. |

1/2 of |

(h) from col. |

column (g) |

(g)) |

|

|

Check boxes where applicable

|

(j) |

(k) |

(l) |

(m) |

|

Reserved |

Charitable |

Deductible |

2652(a)(3) |

||

for future |

gift |

gift to |

election |

||

use |

|

spouse |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gifts made by

Total of Part 1. Add amounts from Part 1, column (i) . . . . . . . . . . . . . . . . . . . . . . . . . . .

(If more space is needed, attach additional statements.)

Form 709 (2024)

Form 709 (2024) |

Page 4 |

SCHEDULE A Computation of Taxable Gifts (Including transfers in trust) (see instructions) (continued)

Part

(a)

Item

number

(b)

Donee’s name and address

(c)

Relationship

to donor (if

any)

(d)

Description of gift

(e) |

(f) |

(g) |

(h) |

Donor’s adjusted |

Date of gift |

Value at date of |

For split gifts, |

basis of gift |

|

gift |

enter 1/2 of |

|

|

|

column (g) |

|

|

|

|

(i) |

Check boxes |

|

Net transfer |

where applicable |

|

(subtract col. (h) |

|

|

(j) |

||

from col. (g)) |

||

|

2632(b) |

|

|

election out |

|

|

|

Gifts made by

Total of Part 2. Add amounts from Part 2, column (i) |

|

(If more space is needed, attach additional statements.) |

Form 709 (2024) |

Form 709 (2024) |

Page 5 |

SCHEDULE A Computation of Taxable Gifts (Including transfers in trust) (see instructions) (continued)

Part

(a)

Item

number

(b)

Donee’s name and address

(c)

Relationship

to donor (if

any)

(d)

Description of gift

(e)

Donor’s

adjusted basis

of gift

(f) |

(g) |

(h) |

(i) |

Date of gift |

Value at |

For split |

Net transfer |

|

date of gift |

gifts, enter |

(subtract col. |

|

|

1/2 of |

(h) from col. |

|

|

column (g) |

(g)) |

|

|

|

|

Check boxes where applicable

|

(j) |

(k) |

|

(l) |

(m) |

(n) |

||||||

Reserved |

Charitable |

Deductible |

2652(a)(3) |

2632(c) |

||||||||

for future |

gift |

gift to |

election |

election |

||||||||

use |

|

|

|

spouse |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gifts made by

Total of Part 3. Add amounts from Part 3, column (i) . . . . . . . . . . . . . . . . . . . . . . . .

(If more space is needed, attach additional statements.)

Form 709 (2024)

Form 709 (2024) |

Page 6 |

SCHEDULE A Computation of Taxable Gifts (Including transfers in trust) (see instructions) (continued)

Part

1 |

Total value of gifts of donor. Add totals from column (i) of Parts 1, 2, and 3 |

2 |

Total annual exclusions for gifts listed on line 1 (see instructions) |

3Total included amount of gifts. Subtract line 2 from line 1 . . . . . . . . . . . . . . . . . . . . . . . . .

Deductions (see instructions)

4Gifts of interests to spouse for which a marital deduction will be claimed. Enter the total value of items on Parts 1 and 3 of Schedule A for which the box in column (l) is checked . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 |

Exclusions attributable to gifts on line 4 |

6 |

Marital deduction. Subtract line 5 from line 4 |

7Charitable deduction. Enter the total value of items on Parts 1 and 3 of Schedule A for which the box in column (k) is checked, less

|

exclusions |

8 |

Total deductions. Add lines 6 and 7 |

9 |

Subtract line 8 from line 3 |

10 |

|

11 |

Taxable gifts. Add lines 9 and 10. Enter here and on page 1, Part |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

4

5

6

7

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

1

2

3

8

9

10

11

Qualified Terminable Interest Property (QTIP) Marital Deduction (See instructions for Schedule A, Part 4, line 4.)

If a trust (or other property) meets the requirements of qualified terminable interest property under section 2523(f), and: a. The trust (or other property) is listed on Schedule A; and

b. The value of the trust (or other property) is entered in whole or in part as a deduction on Schedule A, Part 4, line 4, then the donor shall be deemed to have made an election to have such trust (or other property) treated as qualified terminable interest property under section 2523(f).

If less than the entire value of the trust (or other property) that the donor has included in Parts 1 and 3 of Schedule A is entered as a deduction on line 4, the donor shall be considered to have made an election only as to a fraction of the trust (or other property). The numerator of this fraction is equal to the amount of the trust (or other property) deducted on Schedule A, Part 4, line 6. The denominator is equal to the total value of the trust (or other property) listed in Parts 1 and 3 of Schedule A.

If you make the QTIP election, the terminable interest property involved will be included in your spouse’s gross estate upon your spouse’s death (section 2044). See instructions for line 4 of Schedule A. If your spouse disposes (by gift or otherwise) of all or part of the qualifying life income interest, your spouse will be considered to have made a transfer of the entire property that is subject to the gift tax. See Transfer of Certain Life Estates Received From Spouse in the instructions.

12Election Out of QTIP Treatment of Annuities

Check here if you elect under section 2523(f)(6) not to treat as qualified terminable interest property any joint and survivor annuities that are reported on Schedule A and would otherwise be treated as qualified terminable interest property under section 2523(f). See instructions. Enter the item numbers from Schedule A for the annuities for which you are making this election.

Form 709 (2024)

Form 709 (2024) |

Page 7 |

SCHEDULE B Gifts From Prior Periods

If you answered “Yes” on line 18a of page 1, Part I, see the instructions for completing Schedule B. If you answered “No,” skip to Part II, Tax Computation on page 1 (or Schedule C or D, if applicable). Complete Schedule A before beginning Schedule B. See instructions for recalculation of the column (c) amounts. Attach calculations.

(a)

Calendar year or calendar quarter (see instructions)

(b)

Internal Revenue office

where prior return was filed

(c)

Amount of applicable credit (unified credit) against gift tax for periods after December 31, 1976

(d)

Amount of specific exemption for prior periods ending before January 1, 1977

(e)

Amount of

taxable gifts

1 |

Totals for prior periods |

|

1 |

|

2 |

Amount, if any, by which total specific exemption, line 1, column (d), is more than $30,000 . . . |

. . . . . . . . . . . . . . . . |

2 |

|

3Total amount of taxable gifts for prior periods. Add amount on line 1, column (e), and amount, if any, on line 2. Enter here and on page 1, Part

Computation, line 2 |

3 |

(If more space is needed, attach additional statements.) |

Form 709 (2024) |

Form 709 (2024) |

Page 8 |

SCHEDULE C Deceased Spousal Unused Exclusion (DSUE) Amount and Restored Exclusion

Provide the following information to determine the DSUE amount and applicable credit received from prior spouses. Complete Schedule A before beginning Schedule C.

(a) |

|

(b) |

|

(c) |

(d) |

(e) |

(f) |

|

Name of deceased spouse |

|

Date of death |

Portability election made? |

If “Yes,” DSUE |

DSUE amount applied by |

Date of gift(s) (enter as |

||

(dates of death after December 31, 2010, only) |

|

|

|

|

|

amount received |

donor to lifetime gifts (list |

mm/dd/yy for Part 1 and |

|

|

|

|

|

|

from spouse |

current |

as yyyy for Part 2) |

|

|

|

Yes |

|

No |

|

and prior gifts) |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Part |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part |

|

|

|

|

|

|

|

|

TOTAL (for all DSUE amounts applied from column (e) for Part 1 and Part 2. Enter here and on line 2 below) |

|

|

|

1 |

Donor’s basic exclusion amount (see instructions) |

1 |

|

2 |

Total from column (e), Parts 1 and 2 |

2 |

|

3 |

Restored Exclusion Amount (see instructions) |

3 |

|

4 |

Add lines 1, 2, and 3 |

4 |

|

5 |

Applicable credit on amount on line 4 (see Table for Computing Gift Tax in the instructions). Enter here and on line 7, Part |

5 |

|

(If more space is needed, attach additional statements.) |

|

Form 709 (2024) |

|

Form 709 (2024) |

Page 9 |

SCHEDULE D Computation of

Note: Inter vivos direct skips that are completely excluded by the GST exemption must still be fully reported (including value and exemptions claimed) on Schedule D.

Part

(a) |

(b) |

(c) |

(d) |

(e) |

Item number (from |

Description |

Value (from Schedule A, Part 2, |

Nontaxable portion of transfer |

Net transfer (subtract |

Schedule A, Part 2, col. (a), |

(only for ETIP transfers) |

col. (i), or close of ETIP |

|

col. (d) from col. (c)) |

then ETIP transfers, if any) |

|

described in col. (b)) |

|

|

1

Gifts made by spouse (for gift splitting only)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(If more space is needed, attach additional statements.) |

|

|

Form 709 (2024) |

|

Form 709 (2024) |

Page 10 |

||

SCHEDULE D |

Computation of |

|

|

Part |

|

||

Complete items |

|

||

1 |

Maximum allowable exemption (see instructions) |

1 |

|

2 |

Total exemption used for periods before filing this return |

2 |

|

3 |

Exemption available for this return. Subtract line 2 from line 1 |

3 |

|

4 |

Exemption claimed on this return from Part 3, column (c), total below |

4 |

|

5Automatic allocation of exemption to transfers reported on Schedule A, Part 3. To opt out of the automatic allocation rules, you must attach an “Election Out”

|

statement. See instructions |

5 |

6 |

Exemption allocated to transfers not shown on line 4 or line 5 above. You must attach a “Notice of Allocation.” See instructions |

6 |

7 |

Add lines 4, 5, and 6 |

7 |

8 |

Exemption available for future transfers. Subtract line 7 from line 3 |

8 |

Part

(a) |

(b) |

(c) |

(d) |

(e) |

(f) |

(g) |

Item number |

Net transfer |

GST exemption allocated |

Divide col. (c) |

Inclusion ratio |

Applicable rate |

|

(from Schedule D, |

(from Schedule D, |

|

by col. (b) |

(subtract col. (d) |

(multiply col. (e) |

transfer tax |

Part 1) |

Part 1, col. (e)) |

|

|

from 1.000) |

by 40% (0.40)) |

(multiply col. (b) |

|

|

|

|

|

|

by col. (f)) |

|

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gifts made by spouse (for gift splitting only)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total exemption claimed. Enter here and on Part |

|

|

|

|

|

|

2, line 4, above. May not exceed Part 2, line 3, |

|

Total |

|

|||

above |

|

10; and on page 1, Part |

|

|||

|

|

|

|

|

|

|

(If more space is needed, attach additional statements.) |

|

|

|

Form 709 (2024) |

||

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 709 is used to report gifts made during the tax year that exceed the annual exclusion limit, which is set by the IRS. |

| Filing Requirement | Individuals must file Form 709 if they give a gift valued over the annual exclusion amount, which is $17,000 for the year 2023. |

| Gift Splitting | Married couples can choose to split gifts, allowing each spouse to give up to the annual exclusion amount, effectively doubling the limit. |

| State-Specific Forms | Some states have their own gift tax forms, governed by laws such as California's Revenue and Taxation Code Section 13600. |

| Deadline | Form 709 is due on April 15 of the year following the gift, coinciding with the federal income tax filing deadline. |

Completing the IRS 709 form is an important step for individuals who are required to report gifts made during the tax year. After filling out the form, you will need to submit it to the IRS along with any necessary documentation. This process ensures that all relevant information is accurately reported.

What is the IRS Form 709 and why is it important?

The IRS Form 709, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is a crucial document for individuals who make gifts that exceed the annual exclusion limit set by the IRS. This form is used to report gifts made during the tax year and to calculate any potential gift tax liability. Understanding the importance of this form is essential for proper estate planning and ensuring compliance with tax regulations. By filing Form 709, individuals can keep track of their lifetime gift tax exemption, which can ultimately affect their estate tax liability upon death.

Who is required to file Form 709?

Individuals are required to file Form 709 if they make gifts that exceed the annual exclusion amount, which is adjusted periodically for inflation. For example, in recent years, this amount has been $15,000 per recipient. If a person gifts more than this amount to any individual in a given year, they must file Form 709 to report the excess. Additionally, if a couple decides to split gifts, both partners may need to file the form, depending on the total amount gifted. It is important to note that even if no tax is owed, the form must still be filed to document the gift properly.

What types of gifts must be reported on Form 709?

Form 709 requires reporting a variety of gifts, including cash, property, and other assets. Gifts can include tangible items like real estate or vehicles, as well as intangible assets such as stocks or bonds. Additionally, any gift made to a trust or a gift that involves a future interest must be reported. It is essential to consider not only the value of the gift but also the recipient's relationship to the giver, as this can affect tax implications. Gifts made to spouses, for example, may qualify for different exclusions or exemptions.

What happens if I do not file Form 709 when required?

Failing to file Form 709 when required can lead to significant consequences. The IRS may impose penalties for late filing, which can accumulate over time. Additionally, not reporting a gift can result in the loss of the lifetime gift tax exemption, which could lead to a higher estate tax liability in the future. It is also possible that the IRS may audit the individual’s tax returns, leading to further complications. To avoid these issues, it is advisable to consult with a tax professional who can provide guidance on compliance and help ensure that all necessary forms are filed accurately and on time.

Not providing accurate personal information. Ensure that names, addresses, and Social Security numbers are correct. Any errors can delay processing.

Failing to report all gifts. All gifts over the annual exclusion amount must be reported. Omitting any can lead to penalties.

Incorrectly calculating the gift tax. Understanding the annual exclusion and lifetime exemption is crucial. Miscalculations can result in unexpected tax liabilities.

Forgetting to sign the form. A missing signature renders the form invalid. Always double-check before submitting.

Not filing on time. The IRS has strict deadlines for the 709 form. Late filings can incur penalties and interest.

Using outdated forms. Always download the latest version of the IRS 709 form from the official IRS website. Using old forms can lead to rejection.

Neglecting to include necessary attachments. Supporting documents, such as appraisals for gifts of property, should be included. Missing attachments can complicate processing.

Not seeking professional help when needed. Complex situations may require expert advice. Consulting a tax professional can prevent costly mistakes.

The IRS Form 709, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is an important document for individuals who have made significant gifts during the tax year. However, it is often accompanied by other forms and documents that help provide a complete picture of an individual's financial situation and tax obligations. Below is a list of commonly used forms and documents that may be necessary when filing the IRS Form 709.

Understanding these forms and documents can help ensure that you are fully prepared when filing the IRS Form 709. Each item plays a role in providing clarity and transparency regarding your financial situation and tax responsibilities. If you have any questions or need assistance, seeking professional guidance can be beneficial.

The IRS Form 706 is similar to Form 709 in that both are used for estate and gift tax purposes. Form 706 is filed by the executor of an estate to report the value of the deceased person's estate. Like Form 709, it calculates the amount of tax owed based on the total value of assets, including gifts made during the individual's lifetime. Both forms aim to ensure compliance with federal tax laws regarding the transfer of wealth, whether through gifts or inheritance.

Form 1040, the individual income tax return, shares similarities with Form 709 in that both require detailed reporting of financial information. While Form 1040 focuses on income earned during the year, it may also include information on gifts received. Both forms are essential for determining tax liabilities, and each requires accurate reporting to avoid penalties. The process of gathering information for both forms can be quite similar, as both require thorough documentation of financial activities.

Form 990 is another document related to financial reporting, specifically for tax-exempt organizations. While it does not directly deal with gift taxes, it requires organizations to disclose large donations and gifts received. Similar to Form 709, Form 990 promotes transparency in financial dealings and ensures that organizations comply with IRS regulations regarding charitable contributions. Both forms emphasize the importance of accurate reporting to maintain tax compliance.

The IRS Form 4506-T, which requests a transcript of tax returns, is similar to Form 709 in that both may be used during audits or reviews. Form 4506-T helps taxpayers obtain necessary documentation to support claims made on their tax returns, including gifts reported on Form 709. This connection underscores the importance of maintaining accurate records for both gift tax reporting and overall tax compliance.

Form 1041, the U.S. Income Tax Return for Estates and Trusts, also shares a relationship with Form 709. While Form 1041 is used to report income generated by an estate or trust, it may involve gifts made by the trust or estate. Both forms require careful tracking of financial transactions and assets, ensuring that all income and gifts are reported correctly to the IRS.

Form 709 and Form 8822, which is used to change an address, are related in that both require taxpayers to keep the IRS updated on their personal information. While Form 709 focuses on reporting gifts, Form 8822 ensures that the IRS has the correct address for sending important tax documents. Keeping contact information current is crucial for receiving timely notifications regarding any tax obligations or changes.

Form 1099 is another document that relates to reporting financial transactions. While it primarily reports income received by individuals, it may also include information about gifts if they exceed certain thresholds. Both Form 709 and Form 1099 require accurate reporting to ensure compliance with IRS regulations. They serve as critical tools for the IRS to track financial activities and assess tax liabilities.

Form W-2, which reports wages and salaries, is similar to Form 709 in that both require accurate reporting of financial information. While Form W-2 focuses on employment income, it may indirectly relate to gift tax liabilities if significant gifts are made by an employer to an employee. Both forms play a role in the overall financial picture of individuals and ensure proper tax compliance.

Lastly, Form 8862, which is used to claim a tax credit after a prior denial, connects with Form 709 in the context of maintaining accurate tax records. If a taxpayer has previously been denied a credit due to unreported gifts, they must provide detailed information on Form 709 to support their claim. Both forms emphasize the importance of thorough documentation and accurate reporting to avoid complications with the IRS.

When filling out the IRS 709 form, it's essential to be careful and thorough. Here are some important do's and don'ts to keep in mind:

Taking these steps can help ensure that your filing goes smoothly and that you meet all necessary requirements.

The IRS Form 709, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, often leads to confusion. Here are eight common misconceptions about this form that many people have:

Understanding these misconceptions can help you navigate the complexities of gift taxes more confidently. Always consult a tax professional for personalized advice based on your situation.

When filling out and using the IRS 709 form, there are several important points to keep in mind: