The Inventory Tax 50-246 form is a crucial document for motor vehicle dealers in Texas, ensuring compliance with state tax regulations. Each month, dealers must file this form alongside the total unit property tax owed for all vehicles sold in the previous month. This requirement stems from Tax Code Section 23.122, which mandates accurate reporting to local tax authorities. The form must be submitted separately for each business location and should include detailed information about each vehicle sold, including its make, model, and sales price. Dealers have the option to elect an alternative filing method under Tax Code Chapter 22, provided they meet specific criteria. This election can simplify the reporting process for eligible dealers. It's essential to file the Inventory Tax 50-246 by the 10th of each month to avoid penalties, which can accumulate quickly for late submissions. The form also outlines the responsibilities of dealers regarding documentation retention and the consequences of failing to comply with the filing requirements. Understanding these aspects is vital for maintaining good standing with tax authorities and ensuring smooth business operations.

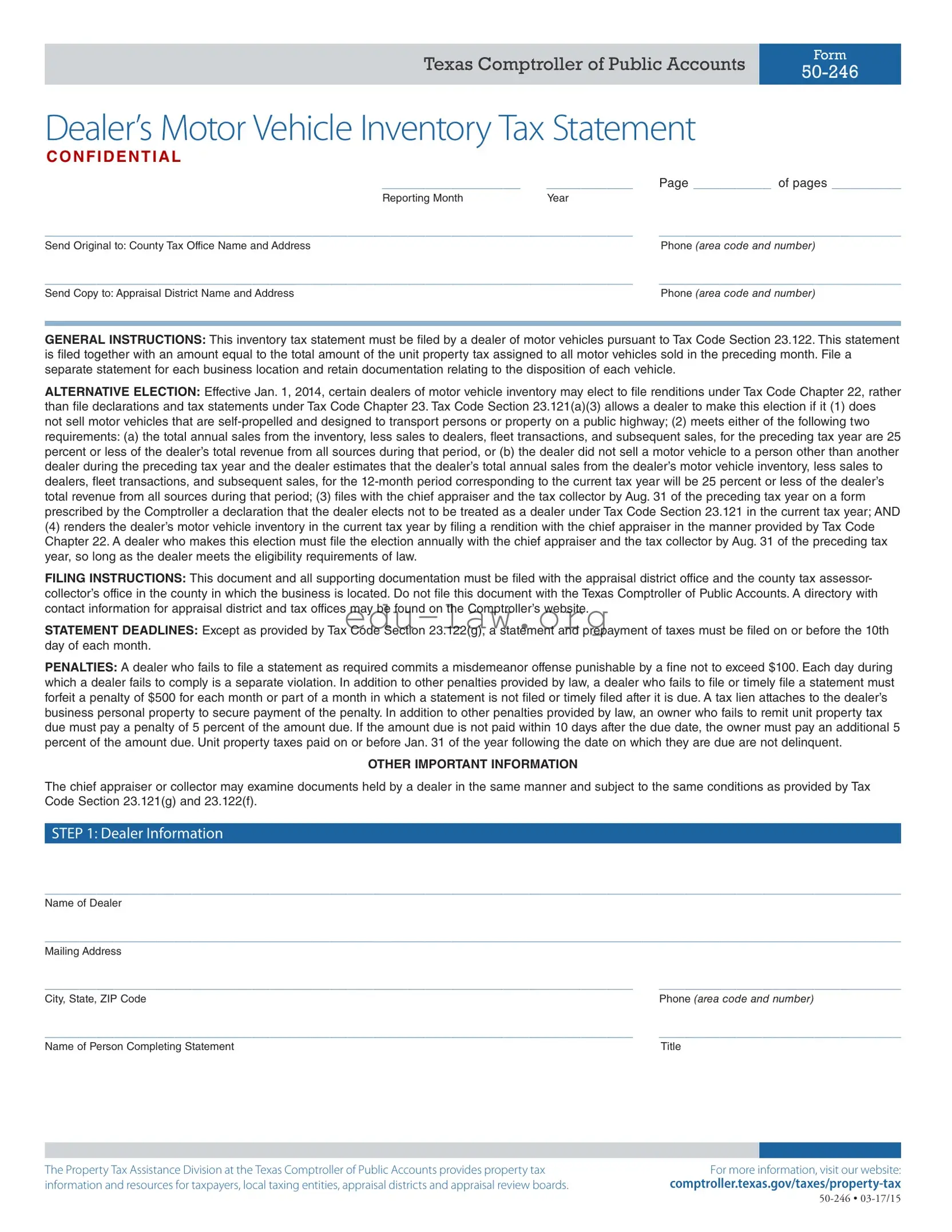

Texas Comptroller of Public Accounts |

Form |

|

|

Dealer’s Motor Vehicle Inventory Tax Statement

CONFIDENT IAL

________________ |

__________ |

Page _________ of pages ________ |

Reporting Month |

Year |

|

____________________________________________________________________ |

____________________________ |

|

Send Original to: County Tax Office Name and Address |

|

Phone (area code and number) |

____________________________________________________________________ |

____________________________ |

|

Send Copy to: Appraisal District Name and Address |

|

Phone (area code and number) |

GENERAL INSTRUCTIONS: This inventory tax statement must be filed by a dealer of motor vehicles pursuant to Tax Code Section 23.122. This statement is filed together with an amount equal to the total amount of the unit property tax assigned to all motor vehicles sold in the preceding month. File a separate statement for each business location and retain documentation relating to the disposition of each vehicle.

ALTERNATIVE ELECTION: Effective Jan. 1, 2014, certain dealers of motor vehicle inventory may elect to file renditions under Tax Code Chapter 22, rather than file declarations and tax statements under Tax Code Chapter 23. Tax Code Section 23.121(a)(3) allows a dealer to make this election if it (1) does not sell motor vehicles that are

(4)renders the dealer’s motor vehicle inventory in the current tax year by filing a rendition with the chief appraiser in the manner provided by Tax Code Chapter 22. A dealer who makes this election must file the election annually with the chief appraiser and the tax collector by Aug. 31 of the preceding tax year, so long as the dealer meets the eligibility requirements of law.

FILING INSTRUCTIONS: This document and all supporting documentation must be filed with the appraisal district office and the county tax assessor- collector’s office in the county in which the business is located. Do not file this document with the Texas Comptroller of Public Accounts. A directory with contact information for appraisal district and tax offices may be found on the Comptroller’s website.

STATEMENT DEADLINES: Except as provided by Tax Code Section 23.122(g), a statement and prepayment of taxes must be filed on or before the 10th day of each month.

PENALTIES: A dealer who fails to file a statement as required commits a misdemeanor offense punishable by a fine not to exceed $100. Each day during which a dealer fails to comply is a separate violation. In addition to other penalties provided by law, a dealer who fails to file or timely file a statement must forfeit a penalty of $500 for each month or part of a month in which a statement is not filed or timely filed after it is due. A tax lien attaches to the dealer’s business personal property to secure payment of the penalty. In addition to other penalties provided by law, an owner who fails to remit unit property tax due must pay a penalty of 5 percent of the amount due. If the amount due is not paid within 10 days after the due date, the owner must pay an additional 5 percent of the amount due. Unit property taxes paid on or before Jan. 31 of the year following the date on which they are due are not delinquent.

OTHER IMPORTANT INFORMATION

The chief appraiser or collector may examine documents held by a dealer in the same manner and subject to the same conditions as provided by Tax Code Section 23.121(g) and 23.122(f).

STEP 1: Dealer Information

___________________________________________________________________________________________________

Name of Dealer

___________________________________________________________________________________________________

Mailing Address

____________________________________________________________________ |

____________________________ |

City, State, ZIP Code |

Phone (area code and number) |

____________________________________________________________________ |

____________________________ |

Name of Person Completing Statement |

Title |

The Property Tax Assistance Division at the Texas Comptroller of Public Accounts provides property tax |

For more information, visit our website: |

information and resources for taxpayers, local taxing entities, appraisal districts and appraisal review boards. |

Texas Comptroller of Public Accounts |

Form |

|

|

STEP 2: Business’ Name and Physical Address of Business Location

Provide the appraisal district account number if available or attach tax bill or copy of appraisal or tax office correspondence concerning your account.

___________________________________________________________________________________________________

Name of Business

___________________________________________________________________________________________________

Address, City, State, ZIP Code

____________________________________________________________________ |

____________________________ |

Account Number |

Business Start Date, if Not in Business on Jan. 1 |

____________________________________________________________________ |

|

General Distinguishing Number (GDN) |

|

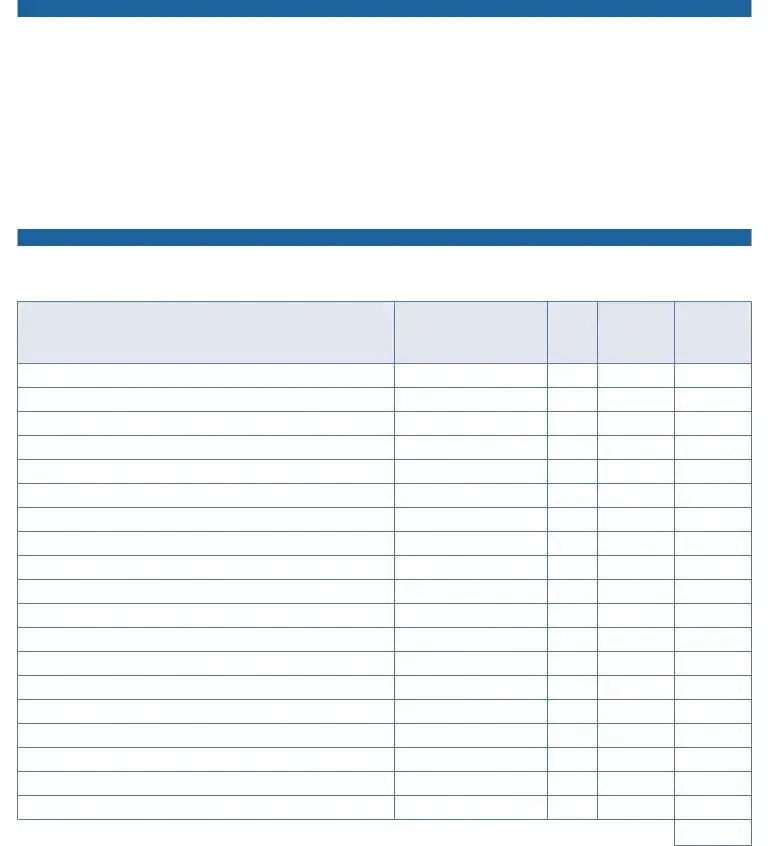

STEP 3: Vehicle Inventory Information

Provide the following information about each motor vehicle sale during the reporting month. Continue on additional sheets if necessary. In lieu of filling out the information in this step, you may attach separate documentation setting forth the information required. All such information must be separately identified in a manner that conforms to the column headers used in the table below. See last page for additional instructions and footnotes.

Description of Vehicle Sold

Date of |

Model |

|

Vehicle |

Sale |

Year |

Make |

Identification Number |

|

|

|

|

Purchaser’s

Name

Type of

Sale1

Sales Price2

Unit Property

Tax3

Total Unit Property Tax4

________________________________________________

Unit Property Tax Factor

For more information, visit our website: |

Page 2 |

|

|

Texas Comptroller of Public Accounts |

Form |

|

|

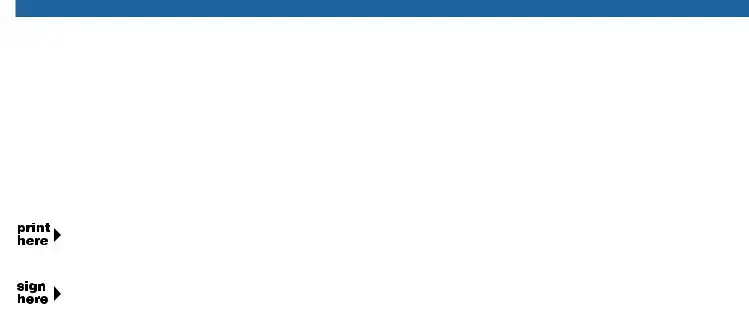

STEP 4: Total Units Sold and Total Sales

Number of units sold for reporting month:

______________________ |

______________________ |

______________________ |

_____________________ |

|||

Motor Vehicle Inventory |

Fleet Transactions |

Dealer Sales |

|

Subsequent Sales |

||

Sales amounts for reporting month: |

|

|

|

|

||

$_____________________ |

$_____________________ |

$_____________________ |

$ ____________________ |

|||

Motor Vehicle Inventory |

Fleet Transactions |

Dealer Sales |

|

Subsequent Sales |

||

|

|

|

|

|

|

|

STEP 5: Signature and Date |

|

|

|

|

||

Signature required on last page only. |

|

|

|

|

||

|

________________________________ |

|||||

|

|

__________________________________________________________ |

||||

|

||||||

|

|

Print Name |

|

|

Title |

|

|

________________________________ |

|||||

|

|

_________________________________________________________ |

||||

|

||||||

|

|

Authorized Signature |

|

|

Date |

|

If you make a false statement on this report, you could be found guilty of a Class A misdemeanor or a state jail felony under Penal Code Section 37.10

For more information, visit our website: |

Page 3 |

|

|

Texas Comptroller of Public Accounts |

Form |

|

|

Additional Instructions

Step 3: Information on each vehicle sold during the reporting month. Complete the information on each motor vehicle sold, including the date of sale, model year, model make, vehicle identification number, purchaser’s name, type of sale, sales price and unit property tax. The footnotes include:

1Type of Sale: Place one of the following codes by each sale reported:

MV – motor vehicle inventory – sales of motor vehi- cles. A motor vehicle is a fully

FL – fleet transactions – motor vehicles included in the sale of five or more motor vehicles from inventory to the same person within one calendar year.

DL – dealer sales – sales of vehicles to another Texas dealer or dealer who is legally recognized in another state as a motor vehicle dealer.

SS – subsequent sales –

2Sales Price: Total amount of money paid or to be paid for the purchase of a motor vehicle as set forth as sales price in the form entitled Application for Texas Certificate of Title promulgated by the Texas Department of Motor Vehicles. In a transaction that does not involve the use of that form, the term means an amount of money that is equivalent, or substantially equivalent, to the amount that would appear as sales price on the Application for Texas Certificate of Title if that form were involved.

3Unit Property Tax: To compute, multiply the sales price by the unit property tax factor. Contact either the county tax

4Total unit property tax for reporting month: Enter the total amount of unit property tax from the “Total for this page only” box on previous page(s). This is the total amount of unit property tax that will be submitted with the statement to the collector.

For more information, visit our website: |

Page 4 |

|

|

| Fact Name | Description |

|---|---|

| Form Purpose | The Inventory Tax 50-246 form is used by motor vehicle dealers in Texas to report and pay unit property taxes on vehicles sold in the previous month. |

| Governing Law | This form is governed by Texas Tax Code Section 23.122, which outlines the requirements for filing and paying inventory taxes. |

| Filing Frequency | Dealers must file the form by the 10th day of each month, reporting sales from the previous month. |

| Alternative Election | Since January 1, 2014, certain dealers may elect to file under Tax Code Chapter 22 instead of Chapter 23, provided they meet specific criteria. |

| Penalties for Non-Compliance | Failure to file can result in a misdemeanor offense and penalties up to $500 for each month the form is late. |

| Documentation Retention | Dealers must retain documentation regarding the disposition of each vehicle sold, which supports the information reported on the form. |

| Signature Requirement | A signature is required on the last page of the form to validate the information provided. |

| Contact Information | Dealers must send the original form to the county tax office and a copy to the appraisal district office. |

| Unit Property Tax Calculation | The unit property tax is calculated by multiplying the sales price of each vehicle by the unit property tax factor, which is based on the prior year's aggregate tax rate. |

Completing the Inventory Tax 50-246 form requires careful attention to detail. Each section must be filled out accurately to ensure compliance with tax regulations. Follow these steps to fill out the form correctly.

Once the form is completed, submit it along with any required documentation to the appropriate appraisal district and county tax assessor-collector offices. Ensure that all information is accurate to avoid penalties or delays in processing.

What is the Inventory Tax 50-246 form and who needs to file it?

The Inventory Tax 50-246 form, officially known as the Dealer’s Motor Vehicle Inventory Tax Statement, is a document required by Texas law for motor vehicle dealers. If you operate a business that sells motor vehicles, you must file this form each month to report the total unit property tax on vehicles sold in the previous month. This helps ensure that you are paying the correct taxes based on your inventory sales. Each business location requires a separate form, so it's essential to keep accurate records for each site.

What are the deadlines for filing the Inventory Tax 50-246 form?

Timeliness is crucial when it comes to filing the Inventory Tax 50-246 form. You must submit the form and any associated tax payments by the 10th day of each month. If you miss this deadline, you may face penalties, including fines for late filing. Staying organized and setting reminders can help you avoid these costly mistakes.

What happens if I fail to file the Inventory Tax 50-246 form on time?

Failing to file the Inventory Tax 50-246 form on time can lead to significant penalties. Not only could you face a misdemeanor offense with a fine up to $100, but you may also incur additional penalties of $500 for each month the statement is not filed or is filed late. Each day of non-compliance is treated as a separate violation. Furthermore, a tax lien could be placed on your business personal property to secure payment of these penalties, making it critical to adhere to filing deadlines.

Can motor vehicle dealers elect to file under a different tax code?

Yes, certain motor vehicle dealers have the option to file under a different tax code. Effective January 1, 2014, if you meet specific criteria, you can elect to file renditions under Tax Code Chapter 22 instead of the traditional declarations and tax statements under Chapter 23. This alternative election is available if you do not sell self-propelled vehicles or if your motor vehicle sales constitute 25% or less of your total revenue. To make this election, you must file a declaration with the chief appraiser and tax collector by August 31 of the preceding tax year. This option can simplify your reporting process, but it requires careful consideration of your business's sales activities.

Incomplete Dealer Information: Failing to provide all necessary details, such as the dealer's name, mailing address, and contact information, can lead to processing delays. Ensure every section is fully completed.

Incorrect Vehicle Inventory Reporting: Errors in reporting vehicle sales, such as missing sales dates, incorrect model years, or inaccurate identification numbers, can result in penalties. Double-check all vehicle information before submission.

Missing Signature: Not signing the form can invalidate the submission. The signature is required on the last page, so ensure it is included before sending.

Late Filing: Submitting the statement after the deadline can incur significant penalties. Remember, the statement and payment are due by the 10th of each month. Timely filing is crucial.

The Inventory Tax 50-246 form is essential for motor vehicle dealers in Texas, but it is often accompanied by other important documents. Each of these forms plays a crucial role in ensuring compliance with state tax regulations. Below is a list of related documents that dealers may need to file or maintain alongside the Inventory Tax 50-246 form.

These documents collectively support the accurate reporting and compliance of motor vehicle dealers with Texas tax laws. Keeping them organized and readily available can simplify the filing process and help avoid potential penalties.

The Texas Property Tax Rendition Form is similar to the Inventory Tax 50-246 form in that both documents are used by businesses to report property tax information to local authorities. The rendition form is specifically for reporting personal property owned by businesses, including machinery and equipment, while the Inventory Tax 50-246 focuses solely on motor vehicle inventory. Both forms require detailed information about the assets held, including values and descriptions, and must be filed annually with the appropriate appraisal district and tax collector. Failure to file either form can result in penalties, emphasizing the importance of timely and accurate reporting.

The Texas Franchise Tax Report serves a similar purpose in terms of tax reporting but applies to businesses as a whole rather than specific inventory. While the Inventory Tax 50-246 requires information on motor vehicle sales and inventory, the Franchise Tax Report necessitates details about the business's revenue and financial performance. Both forms are essential for compliance with state tax laws and must be submitted to the Texas Comptroller's office. They share a common goal of ensuring businesses contribute their fair share to state revenue, albeit through different mechanisms.

The Texas Sales and Use Tax Permit Application also parallels the Inventory Tax 50-246 in its requirement for businesses to report specific information to the state. This application is necessary for businesses that sell tangible goods, including motor vehicles. Like the Inventory Tax form, it requires detailed information about the business and its operations. Both documents are crucial for tax compliance, and businesses must ensure they are accurately completed and submitted to avoid penalties.

The Texas Business Personal Property Report is akin to the Inventory Tax 50-246 because it is also a means for businesses to report property they own. This report encompasses all types of personal property, including furniture, equipment, and inventory. While the Inventory Tax form is specifically tailored for motor vehicles, the Business Personal Property Report serves a broader scope. Both documents require detailed asset descriptions and values, and timely submission is critical to avoid fines.

The Texas Vehicle Title Application shares similarities with the Inventory Tax 50-246 in that both involve the sale and transfer of motor vehicles. The Vehicle Title Application is used to document the ownership transfer of a vehicle, while the Inventory Tax form is focused on reporting sales and inventory levels for tax purposes. Both documents are essential in the vehicle sales process and must be accurately completed to ensure compliance with state regulations.

The Texas Dealer's License Application is another document that aligns with the Inventory Tax 50-246. This application is required for individuals or businesses that wish to operate as motor vehicle dealers in Texas. While the Inventory Tax form deals with tax obligations, the Dealer's License Application ensures that the dealer is authorized to conduct business. Both documents play a critical role in the regulatory framework governing motor vehicle sales and require detailed information about the dealer's operations.

The Texas Appraisal District Property Tax Statement is similar to the Inventory Tax 50-246 in that both are used to report property for tax assessment purposes. The Appraisal District Property Tax Statement encompasses various property types, while the Inventory Tax form is specific to motor vehicle inventory. Both documents aim to ensure that property is accurately assessed for taxation, and timely submission is crucial to avoid penalties.

Finally, the Texas Tax Exemption Application is comparable to the Inventory Tax 50-246 as both involve tax reporting and compliance. The Tax Exemption Application is used by businesses seeking exemptions from certain taxes, including property taxes. While the Inventory Tax form focuses on reporting taxable inventory, both documents require detailed information about the business's operations and assets. Ensuring accuracy in these applications is vital for maintaining compliance with state tax laws.

When filling out the Inventory Tax 50-246 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below is a list of things to do and avoid during this process.

Following these guidelines will help ensure that your filing is accurate and timely, reducing the risk of penalties and complications.

Understanding the Inventory Tax 50-246 form can be challenging. Here are some common misconceptions that people have about it:

Being aware of these misconceptions can help ensure compliance and avoid unnecessary penalties. Always consult the official guidelines or a tax professional if unsure about any aspect of the form.