The Indiana Promissory Note form serves as a crucial financial instrument in various lending scenarios, facilitating agreements between borrowers and lenders. This form outlines the terms of a loan, including the principal amount, interest rate, repayment schedule, and any applicable fees. It establishes the legal obligations of the borrower to repay the loan under specified conditions. Additionally, the form may include provisions for late payments and default, ensuring that both parties understand their rights and responsibilities. By clearly documenting the agreement, the Indiana Promissory Note promotes transparency and accountability, making it an essential tool for personal loans, business financing, and real estate transactions. Understanding the components of this form is vital for anyone involved in lending or borrowing, as it helps prevent misunderstandings and disputes down the line.

Indiana Promissory Note Template

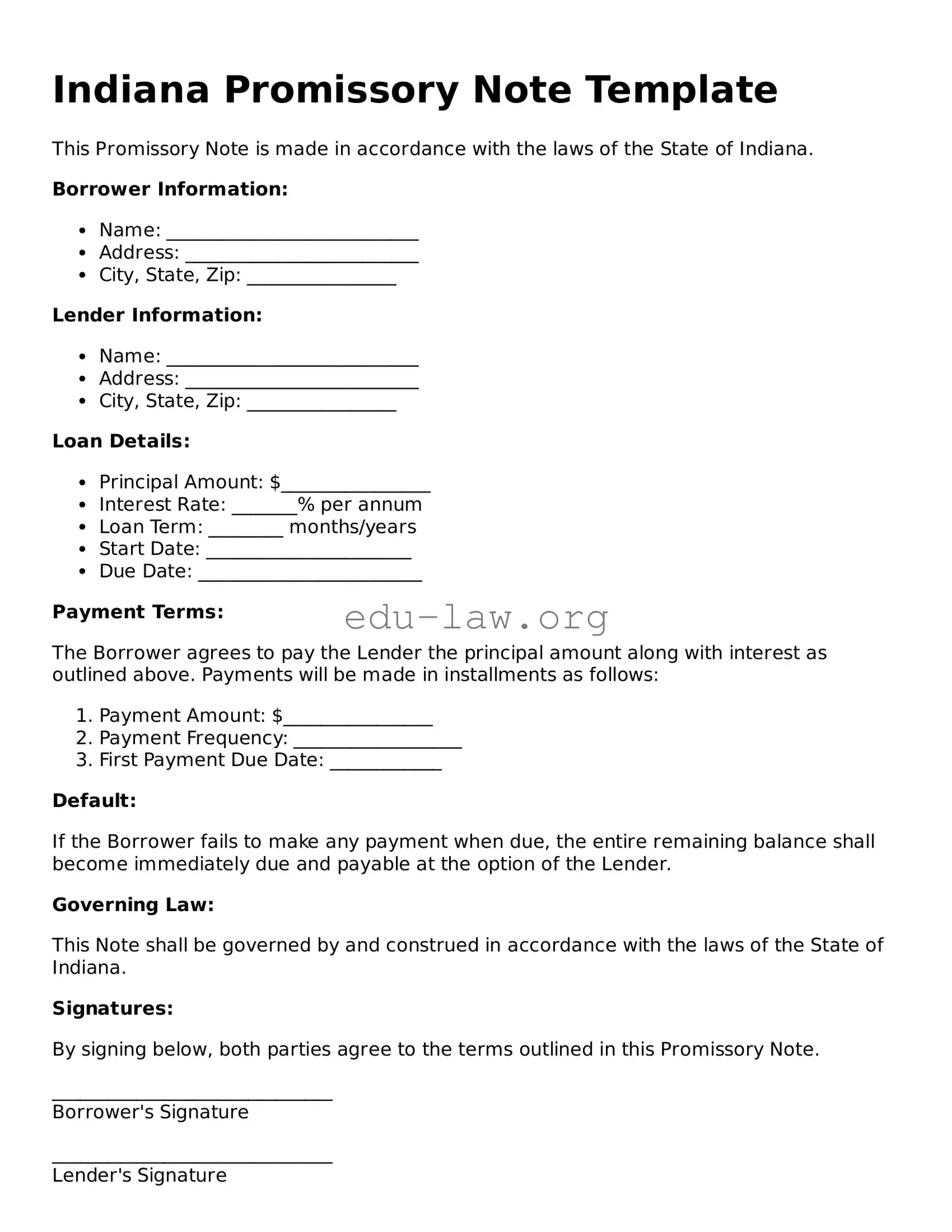

This Promissory Note is made in accordance with the laws of the State of Indiana.

Borrower Information:

Lender Information:

Loan Details:

Payment Terms:

The Borrower agrees to pay the Lender the principal amount along with interest as outlined above. Payments will be made in installments as follows:

Default:

If the Borrower fails to make any payment when due, the entire remaining balance shall become immediately due and payable at the option of the Lender.

Governing Law:

This Note shall be governed by and construed in accordance with the laws of the State of Indiana.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

______________________________

Borrower's Signature

______________________________

Lender's Signature

Date: __________________________

| Fact Name | Description |

|---|---|

| Definition | An Indiana Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time. |

| Governing Law | The Indiana Promissory Note is governed by Indiana Code Title 26, Article 3, which covers negotiable instruments. |

| Parties Involved | Typically, the note involves two parties: the borrower (maker) and the lender (payee). |

| Interest Rates | The note can specify an interest rate, which must comply with Indiana's usury laws. |

| Payment Terms | Payment terms should clearly outline when and how payments will be made, including any grace periods. |

| Default Conditions | The note should detail what constitutes a default, such as missed payments or bankruptcy. |

| Amendments | Any changes to the note must be made in writing and agreed upon by both parties. |

| Signatures | The note must be signed by the borrower to be enforceable, and it is advisable for the lender to sign as well. |

| Witnesses and Notarization | While not required, having witnesses or notarization can add an extra layer of validity to the document. |

| Record Keeping | Both parties should keep a copy of the signed promissory note for their records. |

Once you have the Indiana Promissory Note form in front of you, it’s time to fill it out carefully. This document will require specific information about the loan agreement between the lender and the borrower. Make sure to have all necessary details on hand to complete the form accurately.

After completing the form, ensure that both parties retain a copy for their records. This will help in maintaining clarity and accountability throughout the loan period.

What is a Promissory Note in Indiana?

A Promissory Note is a legal document that outlines a borrower's promise to repay a specified amount of money to a lender under agreed-upon terms. In Indiana, this document typically includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments. It serves as a record of the debt and can be enforced in court if necessary.

What information is required on the Indiana Promissory Note form?

The Indiana Promissory Note form should include several key pieces of information. This includes the names and addresses of both the borrower and lender, the principal amount of the loan, the interest rate, the repayment schedule, and any collateral securing the loan. Additionally, it may outline the consequences of defaulting on the loan, ensuring both parties understand their rights and obligations.

Is a Promissory Note legally binding in Indiana?

Yes, a Promissory Note is legally binding in Indiana as long as it meets certain requirements. The document must be signed by the borrower and, ideally, should be witnessed or notarized to enhance its enforceability. If the terms are clear and both parties agree, the note can be upheld in a court of law if disputes arise.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It’s best to document any modifications in writing and have both parties sign the amended note. This helps prevent misunderstandings and ensures that the terms remain clear and enforceable.

Not including all necessary parties. Ensure that both the borrower and lender are clearly identified, including their full names and addresses.

Failing to specify the loan amount. Clearly state the total amount being borrowed. This avoids confusion later on.

Ignoring the interest rate. If applicable, include the interest rate to be charged on the loan. This should be clearly defined to prevent disputes.

Omitting the repayment terms. Specify how and when the borrower will repay the loan. Include details like payment frequency and due dates.

Not considering late fees. If there are penalties for late payments, make sure to outline these fees in the note.

Neglecting to sign and date the document. Both parties must sign and date the promissory note for it to be legally binding.

Using vague language. Be clear and precise in wording. Ambiguities can lead to misunderstandings and legal issues.

Not keeping copies. Always make copies of the signed promissory note for both parties. This ensures that everyone has access to the same information.

When entering into a financial agreement, a promissory note is often just one part of the overall documentation needed. In Indiana, several other forms and documents commonly accompany a promissory note to ensure clarity and legal enforceability. Below is a list of these important documents, each serving a unique purpose in the lending process.

Understanding these documents can significantly enhance the borrowing experience. Each form plays a vital role in protecting the interests of both the lender and the borrower, ensuring that the terms of the loan are clear and enforceable. Always consider consulting with a legal professional when navigating these agreements to ensure compliance with state laws and regulations.

The Indiana Promissory Note is similar to a Loan Agreement. Both documents outline the terms of a loan, including the amount borrowed, interest rates, and repayment schedules. However, a Loan Agreement tends to be more comprehensive, often detailing additional clauses about collateral, default conditions, and the rights of both parties. While a Promissory Note focuses primarily on the borrower's promise to repay, a Loan Agreement provides a broader framework for the entire lending relationship.

Another document that shares similarities with the Indiana Promissory Note is the Mortgage. A Mortgage is a specific type of loan document that involves real property. While the Promissory Note represents the borrower's commitment to repay the loan, the Mortgage secures that loan against the property. If the borrower defaults, the lender has the right to foreclose on the property. In essence, the Mortgage complements the Promissory Note by adding a layer of security for the lender.

The Indiana Promissory Note also resembles an IOU, which is a simpler acknowledgment of debt. An IOU typically includes the amount owed and a promise to pay but lacks the formal structure and legal enforceability of a Promissory Note. While both documents indicate a debt, an IOU may not specify repayment terms or interest rates, making it less detailed than a Promissory Note.

A Credit Agreement is another document that parallels the Indiana Promissory Note. This agreement outlines the terms under which credit is extended to a borrower. Like a Promissory Note, it specifies the amount borrowed and repayment terms. However, Credit Agreements often cover revolving credit lines and may include terms related to fees and credit limits, making them more complex than a standard Promissory Note.

Similar to the Promissory Note is a Secured Note. A Secured Note is a promise to pay that is backed by collateral. This collateral could be an asset, such as a car or real estate. While both documents involve a promise to repay, a Secured Note offers the lender additional security in case of default, unlike a standard Promissory Note, which is unsecured.

The Indiana Promissory Note is also akin to a Personal Loan Agreement. Both documents outline the terms of a personal loan, including repayment schedules and interest rates. However, a Personal Loan Agreement might include more detailed terms regarding the borrower's obligations and the lender's rights, making it a bit more formal than a straightforward Promissory Note.

Another similar document is a Business Loan Agreement. This document serves a similar purpose as the Promissory Note but is tailored for business transactions. It includes terms for business loans, such as interest rates, repayment schedules, and specific business-related clauses. While a Promissory Note is often used for personal loans, a Business Loan Agreement is more suited for commercial purposes.

A Lease Agreement can also be compared to the Indiana Promissory Note in certain contexts. While primarily used for renting property, a Lease Agreement often includes a payment schedule similar to that of a Promissory Note. In situations where a lease involves significant payments over time, the payment terms can resemble those found in a Promissory Note, although the purpose and legal implications differ.

Lastly, a Payment Plan Agreement shares characteristics with the Indiana Promissory Note. Both documents outline the terms for repayment of a debt, including the amount owed and the schedule for payments. A Payment Plan Agreement is typically used in situations where a debtor is unable to pay a debt in full upfront. It provides a structured way for the debtor to repay the amount over time, similar to the repayment terms found in a Promissory Note.

When filling out the Indiana Promissory Note form, it is important to follow certain guidelines to ensure the document is valid and enforceable. Here’s a list of things you should and shouldn’t do:

By adhering to these guidelines, you can help ensure that your Indiana Promissory Note is properly completed and legally binding.

Understanding the Indiana Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Below is a list of common misunderstandings regarding this legal document.

Addressing these misconceptions can help individuals better understand their rights and responsibilities when engaging with promissory notes in Indiana.

When filling out and using the Indiana Promissory Note form, consider the following key takeaways: