The Illinois Promissory Note form serves as a crucial document in financial transactions, outlining the terms of a loan agreement between a borrower and a lender. This form typically includes essential details such as the principal amount, interest rate, payment schedule, and the maturity date, ensuring both parties have a clear understanding of their obligations. Additionally, it may specify the consequences of default, including late fees or legal actions, providing a framework for resolution should issues arise. The form can be tailored to meet specific needs, allowing for flexibility in terms of repayment and interest structures. By using this standardized document, individuals and businesses can facilitate secure and transparent lending practices, fostering trust and accountability in financial dealings.

Illinois Promissory Note Template

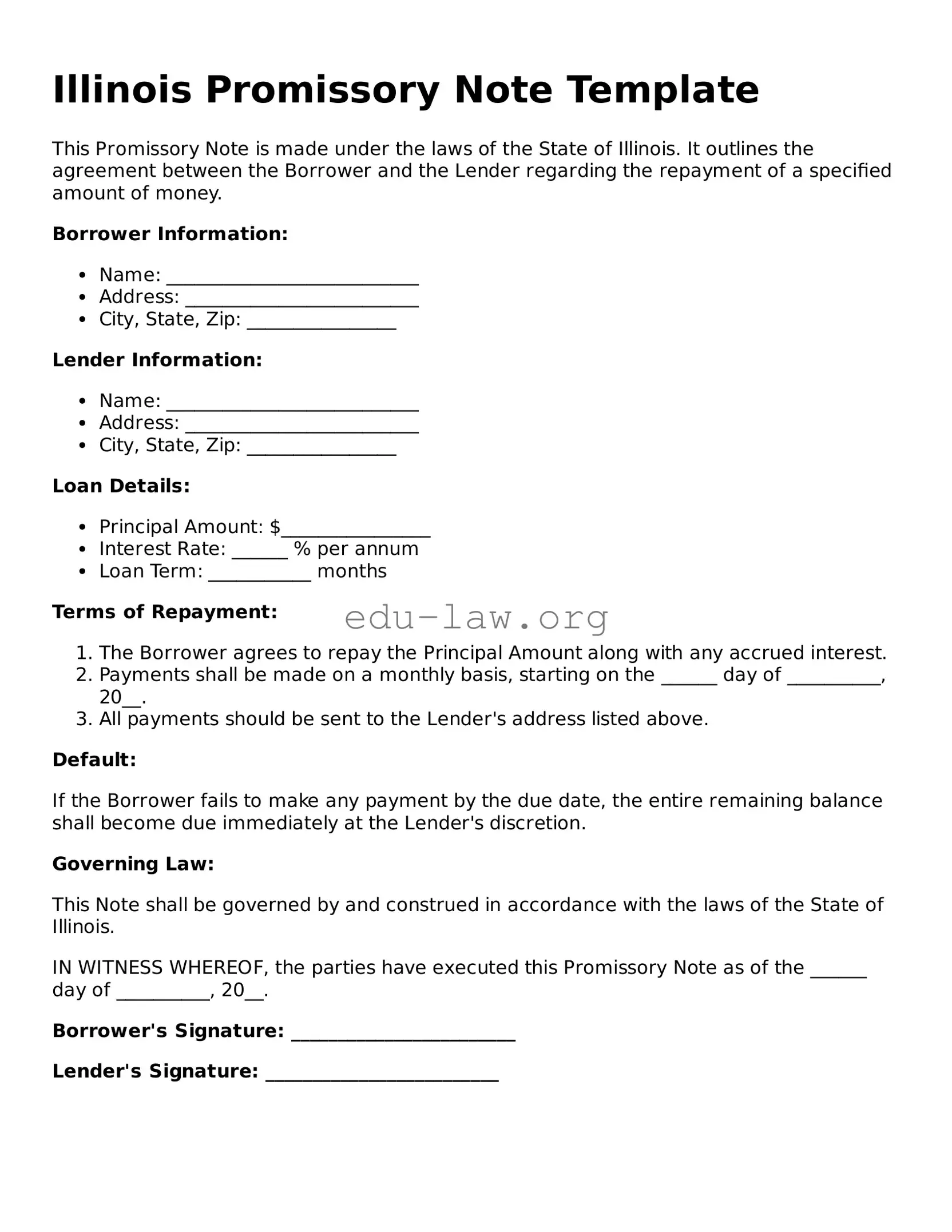

This Promissory Note is made under the laws of the State of Illinois. It outlines the agreement between the Borrower and the Lender regarding the repayment of a specified amount of money.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

Default:

If the Borrower fails to make any payment by the due date, the entire remaining balance shall become due immediately at the Lender's discretion.

Governing Law:

This Note shall be governed by and construed in accordance with the laws of the State of Illinois.

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the ______ day of __________, 20__.

Borrower's Signature: ________________________

Lender's Signature: _________________________

| Fact Name | Description |

|---|---|

| Definition | An Illinois Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. |

| Governing Law | The Illinois Uniform Commercial Code (UCC), specifically Article 3, governs promissory notes in Illinois. |

| Parties Involved | The note involves two primary parties: the maker (the person who promises to pay) and the payee (the person who receives the payment). |

| Interest Rates | Interest can be included in the note, and it must be clearly stated whether it is fixed or variable. |

| Signature Requirement | The maker's signature is required for the note to be legally binding, confirming their commitment to repay the specified amount. |

| Enforceability | Promissory notes are legally enforceable documents, provided they meet certain requirements under Illinois law. |

After obtaining the Illinois Promissory Note form, you will need to complete it accurately to ensure it is legally binding. Follow the steps below to fill out the form correctly.

Once the form is completed, ensure that both parties retain a copy for their records. This will help in maintaining clarity and accountability throughout the loan period.

What is a Promissory Note in Illinois?

A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. In Illinois, this document serves as a legal instrument that outlines the terms of the loan, including the interest rate, payment schedule, and any penalties for late payments. It is essential for both lenders and borrowers, as it provides clear evidence of the debt and the obligations of each party.

What are the key components of an Illinois Promissory Note?

An Illinois Promissory Note typically includes several important components. First, it identifies the borrower and lender, providing their names and addresses. Next, it specifies the principal amount borrowed, the interest rate, and the repayment schedule. Additionally, it may outline any late fees or penalties for missed payments. Finally, the document should include a signature line for both parties, indicating their agreement to the terms. Clear and precise language helps avoid misunderstandings later on.

Is a Promissory Note legally binding in Illinois?

Yes, a promissory note is legally binding in Illinois, provided it meets certain requirements. The note must be in writing and signed by the borrower. It should also include clear terms regarding the amount owed and the repayment schedule. If these conditions are met, the lender has the right to enforce the note in court if the borrower fails to repay the loan as agreed. This legal enforceability is what makes promissory notes a popular choice for personal and business loans.

Do I need a lawyer to create a Promissory Note in Illinois?

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, meaning they fail to make payments as specified in the note, the lender has several options. First, they can attempt to resolve the issue through communication, possibly renegotiating the terms or setting up a payment plan. If that fails, the lender may choose to take legal action to recover the owed amount. This could involve filing a lawsuit, which may lead to a judgment against the borrower, allowing the lender to pursue collection methods such as wage garnishment or bank levies.

Can a Promissory Note be modified after it is signed?

Yes, a promissory note can be modified after it is signed, but both parties must agree to the changes. This typically involves drafting a written amendment that outlines the new terms. It is crucial that both the lender and borrower sign this amendment to ensure its enforceability. Verbal agreements for modifications are generally not considered legally binding, so having a written record is essential for clarity and protection for both parties involved.

Failing to include the date of the agreement. It is crucial to establish when the note was created, as this affects the timeline for repayment.

Not clearly identifying the borrower and the lender. Full names and addresses should be provided to avoid confusion later on.

Omitting the amount of money being borrowed. This figure must be stated clearly to ensure both parties understand the financial obligation.

Neglecting to specify the interest rate. If applicable, the interest rate should be explicitly stated to avoid misunderstandings about the total repayment amount.

Not detailing the repayment schedule. It is important to outline when payments are due, whether they are monthly, quarterly, or in a lump sum.

Failing to include any late fees or penalties for missed payments. Clear terms regarding late fees can prevent disputes in the future.

Not signing the document. Both parties must sign the promissory note for it to be legally binding.

Forgetting to have the document witnessed or notarized, if required. This step adds an extra layer of authenticity and can be important in legal situations.

Using vague or ambiguous language. Clarity is key; all terms should be straightforward to ensure that both parties fully understand their obligations.

When dealing with a promissory note in Illinois, several additional documents may be necessary to ensure clarity and legal compliance. Each of these forms serves a specific purpose in the lending process, and understanding them can help streamline transactions.

Having these documents prepared and understood can facilitate a smoother lending process. It's essential to ensure that all parties are aware of their rights and responsibilities to avoid potential disputes in the future.

A loan agreement is a formal document that outlines the terms and conditions of a loan between a lender and a borrower. Similar to a promissory note, it specifies the amount borrowed, the interest rate, repayment schedule, and any collateral involved. However, a loan agreement often includes more detailed terms, such as default clauses and the responsibilities of both parties, making it a more comprehensive document for larger or more complex loans.

A mortgage is another document that shares similarities with a promissory note. While a promissory note serves as a promise to repay a loan, a mortgage secures that loan against real property. The borrower agrees to repay the loan while granting the lender a lien on the property. Both documents include terms related to repayment, but a mortgage also details what happens if the borrower defaults, including foreclosure procedures.

A secured note is akin to a promissory note but includes specific collateral that backs the loan. This means that if the borrower fails to repay, the lender has the right to take possession of the collateral. Like a promissory note, a secured note includes the amount borrowed and repayment terms, but it adds an extra layer of security for the lender, making it a common choice for personal loans involving valuable assets.

A personal guarantee is similar in that it involves a promise to repay a debt, but it typically applies when a business borrows money. In this case, an individual agrees to be personally responsible for the debt if the business defaults. This document reinforces the lender's position, much like a promissory note does, but it emphasizes personal accountability rather than just the business's creditworthiness.

An IOU, or "I owe you," is a simpler form of a promissory note. It acknowledges a debt and the amount owed but usually lacks the formal structure and detailed terms found in a promissory note. While an IOU may not be legally binding in the same way, it serves as a basic acknowledgment of debt, making it useful for informal loans between friends or family.

A bond is a formal contract where the issuer promises to pay back borrowed money at a specified date, along with interest. Similar to a promissory note, it represents a debt obligation. However, bonds are typically issued by corporations or governments and are sold to investors, making them more complex and regulated. Both documents involve repayment promises, but bonds are often part of larger financial markets.

A lease agreement can resemble a promissory note in that it outlines a payment obligation. When renting property, a tenant agrees to pay rent over a specified period, much like a borrower agrees to repay a loan. While a lease focuses on the rental terms and conditions, the underlying principle of a financial commitment connects it to the concept of a promissory note.

A credit agreement is a detailed document that outlines the terms under which credit is extended to a borrower. Similar to a promissory note, it specifies the loan amount, interest rates, and repayment schedule. However, credit agreements often include provisions for fees, penalties, and other terms related to the credit relationship, making them more complex and tailored to specific lending situations.

An installment agreement is a payment plan that allows a borrower to repay a debt in smaller, manageable amounts over time. Like a promissory note, it outlines the total amount owed and the terms of repayment. However, installment agreements often apply to debts that are being settled in phases, making them a practical option for those who may not be able to pay a lump sum immediately.

A debt settlement agreement is similar to a promissory note in that it represents an agreement between a debtor and creditor about how a debt will be resolved. This document outlines the terms under which the debtor will pay a reduced amount to settle the debt. While a promissory note focuses on repayment of the full amount borrowed, a debt settlement agreement aims to provide a solution when full repayment is not feasible.

When filling out the Illinois Promissory Note form, it’s important to pay attention to details. Here are some guidelines to help ensure that the process goes smoothly.

By following these guidelines, you can create a clear and enforceable Promissory Note that protects the interests of both parties involved.

Understanding the Illinois Promissory Note form can be challenging due to various misconceptions. Here are nine common misunderstandings about this important financial document:

By clarifying these misconceptions, individuals can better understand the importance and utility of the Illinois Promissory Note form.

When filling out and using the Illinois Promissory Note form, it is essential to understand several key aspects to ensure clarity and legality. Here are some important takeaways:

By following these key points, individuals can effectively use the Illinois Promissory Note form to formalize their lending agreements.