The Hawaii Promissory Note form is an important document that outlines the terms of a loan between a borrower and a lender. This form serves to protect both parties by clearly stating the amount borrowed, the interest rate, and the repayment schedule. It includes essential details such as the names and addresses of both the borrower and lender, ensuring that all parties are properly identified. The document also specifies the consequences of default, which helps set clear expectations for repayment. By using this form, individuals can establish a legal record of the loan, making it easier to address any disputes that may arise in the future. Understanding the key components of the Hawaii Promissory Note is crucial for anyone looking to lend or borrow money in the state, as it lays the groundwork for a transparent financial agreement.

Hawaii Promissory Note Template

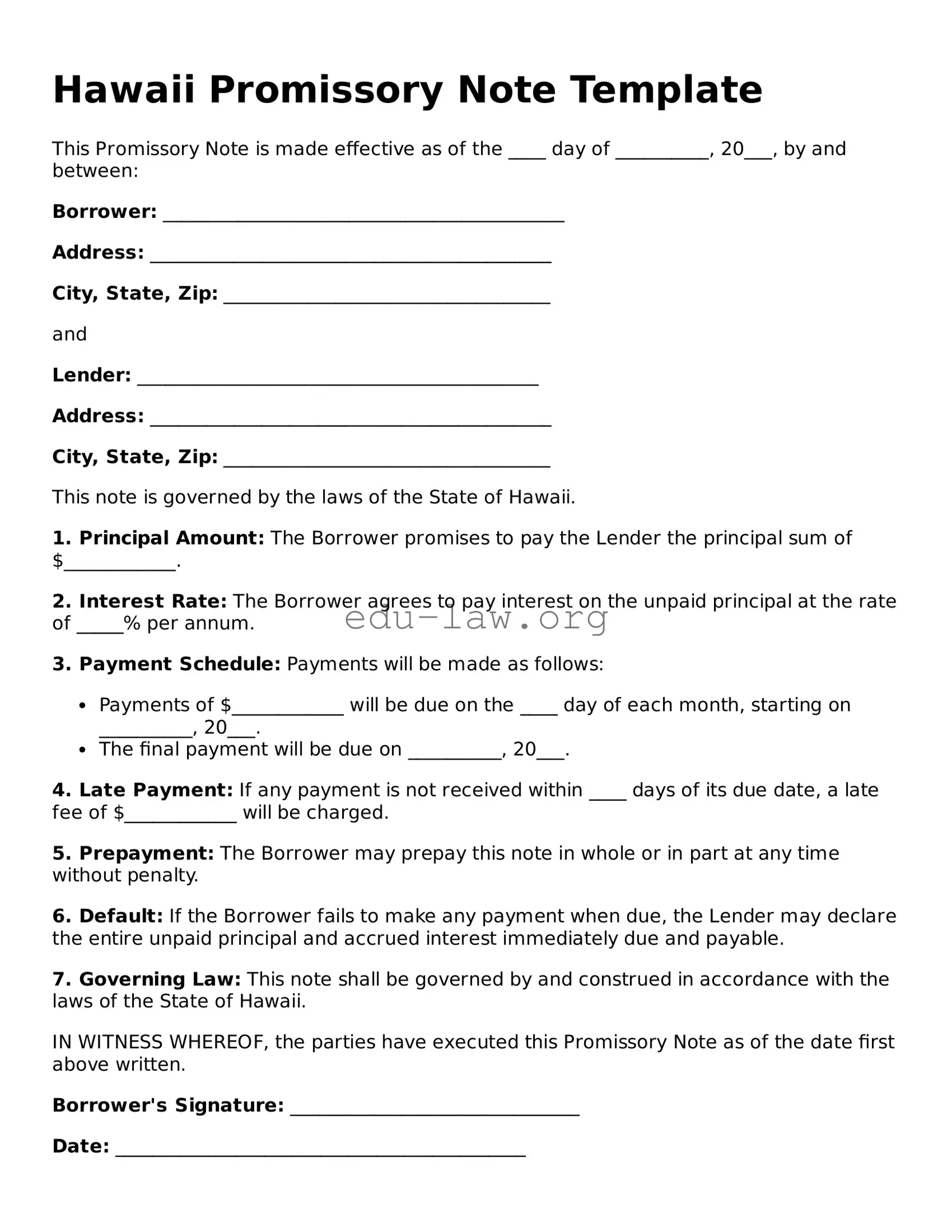

This Promissory Note is made effective as of the ____ day of __________, 20___, by and between:

Borrower: ___________________________________________

Address: ___________________________________________

City, State, Zip: ___________________________________

and

Lender: ___________________________________________

Address: ___________________________________________

City, State, Zip: ___________________________________

This note is governed by the laws of the State of Hawaii.

1. Principal Amount: The Borrower promises to pay the Lender the principal sum of $____________.

2. Interest Rate: The Borrower agrees to pay interest on the unpaid principal at the rate of _____% per annum.

3. Payment Schedule: Payments will be made as follows:

4. Late Payment: If any payment is not received within ____ days of its due date, a late fee of $____________ will be charged.

5. Prepayment: The Borrower may prepay this note in whole or in part at any time without penalty.

6. Default: If the Borrower fails to make any payment when due, the Lender may declare the entire unpaid principal and accrued interest immediately due and payable.

7. Governing Law: This note shall be governed by and construed in accordance with the laws of the State of Hawaii.

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the date first above written.

Borrower's Signature: _______________________________

Date: ____________________________________________

Lender's Signature: ________________________________

Date: ____________________________________________

| Fact Name | Details |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a specified time. |

| Governing Law | The Hawaii Promissory Note is governed by Hawaii Revised Statutes, Chapter 478. |

| Parties Involved | The note involves at least two parties: the borrower (maker) and the lender (payee). |

| Interest Rate | The interest rate can be fixed or variable, and it must be clearly stated in the note. |

| Payment Terms | Payment terms, including the due date and payment frequency, should be explicitly outlined. |

| Enforceability | A properly executed promissory note is legally enforceable in a court of law if it meets all necessary requirements. |

Filling out the Hawaii Promissory Note form is an important step in formalizing a loan agreement. After completing the form, it will need to be signed and dated by all parties involved. Make sure to keep a copy for your records and provide copies to the other parties as well.

What is a Hawaii Promissory Note?

A Hawaii Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. It specifies the amount borrowed, the interest rate, repayment schedule, and any other terms agreed upon by both parties.

Who typically uses a Promissory Note in Hawaii?

Individuals, businesses, and financial institutions often use Promissory Notes. They are common in personal loans, business financing, and real estate transactions. Both lenders and borrowers benefit from having a clear record of the loan terms.

What are the key components of a Hawaii Promissory Note?

Essential components include the names of the borrower and lender, the loan amount, interest rate, repayment terms, maturity date, and any collateral involved. It may also include provisions for late payments and default.

Is a Promissory Note legally binding in Hawaii?

Yes, a properly executed Promissory Note is legally binding in Hawaii. It creates an enforceable obligation for the borrower to repay the loan as outlined in the document.

Do I need a lawyer to create a Promissory Note in Hawaii?

While it's not required to have a lawyer, consulting one can be beneficial, especially for complex loans. A legal professional can ensure that the document complies with state laws and protects your interests.

Can a Promissory Note be modified after it's signed?

Yes, a Promissory Note can be modified if both parties agree to the changes. It's advisable to document any modifications in writing and have both parties sign the amended note to avoid future disputes.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has the right to take legal action to recover the owed amount. This may include filing a lawsuit or pursuing collections, depending on the terms outlined in the note.

Are there any specific state laws governing Promissory Notes in Hawaii?

Hawaii follows general contract law principles regarding Promissory Notes. It’s important to ensure that the note complies with both state and federal regulations, particularly regarding interest rates and disclosures.

Can a Promissory Note be secured or unsecured?

A Promissory Note can be either secured or unsecured. A secured note is backed by collateral, while an unsecured note is not. The choice depends on the agreement between the lender and borrower.

Where can I find a template for a Hawaii Promissory Note?

Templates for Hawaii Promissory Notes can be found online through legal websites or office supply stores. However, it’s advisable to review any template with a legal professional to ensure it meets your specific needs.

Incorrect Borrower Information: One common mistake is failing to provide accurate details about the borrower. This includes the full name, address, and contact information. Inaccuracies can lead to complications in repayment or enforcement.

Missing Lender Information: Just as with the borrower, it's crucial to include complete and correct information for the lender. Omitting this can create confusion about who is entitled to receive payments.

Not Specifying the Loan Amount: Clearly stating the loan amount is essential. Some people forget to include this or write it ambiguously, which can lead to disputes later on.

Failure to State Interest Rate: If the loan includes an interest rate, it must be clearly defined. Leaving this out can result in misunderstandings regarding how much the borrower owes over time.

Omitting Payment Terms: The payment schedule should be detailed. This includes the frequency of payments, due dates, and any grace periods. Not specifying these terms can lead to confusion about when payments are expected.

Not Including Default Terms: It's important to outline what happens in the event of a default. Failing to include this information can leave both parties unprotected if a payment is missed.

Neglecting Signatures: Both parties must sign the document for it to be legally binding. Forgetting to obtain signatures can render the note unenforceable.

Ignoring State-Specific Requirements: Hawaii may have specific laws regarding promissory notes. Not adhering to these can lead to complications, so it's essential to be aware of local regulations.

When engaging in financial transactions in Hawaii, a Promissory Note is often a key document. However, it is typically accompanied by several other forms and documents that help clarify the terms and protect the interests of all parties involved. Here’s a list of essential documents that may be used alongside the Hawaii Promissory Note.

Understanding these documents can significantly enhance your experience in financial transactions. Each form plays a crucial role in ensuring clarity and protection for both lenders and borrowers, fostering a more secure lending environment.

The first document similar to the Hawaii Promissory Note is a Loan Agreement. Like the Promissory Note, a Loan Agreement outlines the terms of borrowing money. It specifies the amount borrowed, the interest rate, and the repayment schedule. Both documents create a legal obligation for the borrower to repay the lender. However, a Loan Agreement often includes more detailed terms and conditions, such as collateral and default consequences, making it more comprehensive than a Promissory Note.

Another similar document is the Mortgage. A Mortgage secures a loan with real property. While the Promissory Note serves as a promise to repay the loan, the Mortgage acts as collateral for that promise. If the borrower fails to repay, the lender can foreclose on the property. Both documents work together, but the Mortgage focuses on the security aspect, while the Promissory Note emphasizes the repayment obligation.

The Deed of Trust is also comparable to the Hawaii Promissory Note. In a Deed of Trust, a borrower transfers property to a trustee as security for a loan. Similar to a Mortgage, it provides the lender with a way to secure the loan. The Promissory Note, on the other hand, is the document that outlines the borrower's promise to repay. Both documents are essential in real estate transactions, but they serve different purposes in the lending process.

A Credit Agreement is another document that shares similarities with the Promissory Note. This agreement outlines the terms under which a lender extends credit to a borrower. It specifies the credit limit, interest rates, and repayment terms. Like the Promissory Note, it establishes a legal obligation. However, a Credit Agreement typically covers ongoing credit relationships, while a Promissory Note is often used for a specific loan amount.

The Security Agreement is also akin to the Hawaii Promissory Note. This document allows a borrower to use personal property as collateral for a loan. While the Promissory Note focuses on the borrower's promise to repay, the Security Agreement details the collateral and the lender's rights if the borrower defaults. Both documents are crucial for protecting the lender's interests, but they address different aspects of the borrowing process.

Lastly, the Personal Guarantee is similar to the Promissory Note in that it involves a promise to repay. In this document, an individual agrees to be responsible for another person's debt. This is particularly relevant in business loans. While the Promissory Note is a direct promise from the borrower, a Personal Guarantee adds an extra layer of security for the lender by holding a third party accountable for the debt.

When filling out the Hawaii Promissory Note form, it's essential to approach the task with care. Here are some key points to consider:

When it comes to the Hawaii Promissory Note form, several misconceptions can lead to confusion and missteps. Understanding these common misunderstandings can help individuals navigate their financial agreements more effectively.

While both documents pertain to borrowing money, a Promissory Note is a simpler, more straightforward promise to repay a specific amount. A loan agreement, on the other hand, often includes detailed terms and conditions, such as collateral and repayment schedules.

Though it is not always mandatory, having a witness or notary can add an extra layer of security and legitimacy to the document. This can be especially important in case of disputes.

In Hawaii, as in many states, interest rates must comply with state laws. Borrowers should be aware of the maximum allowable rates to avoid potential legal issues.

In fact, parties can agree to modify the terms of a Promissory Note. However, any changes should be documented in writing and signed by all parties involved to ensure clarity and enforceability.

Promissory Notes can be used for loans of any size, whether it’s a small personal loan between friends or a larger business transaction. The key is that both parties agree to the terms.

While a Promissory Note is a formal commitment to repay, it does not guarantee that the borrower will fulfill that obligation. It is essential for lenders to assess the borrower's creditworthiness before entering into an agreement.

Filling out and using the Hawaii Promissory Note form requires attention to detail and understanding of its components. Here are key takeaways to keep in mind:

By following these guidelines, you can ensure that the Promissory Note is completed accurately and serves its intended purpose effectively.