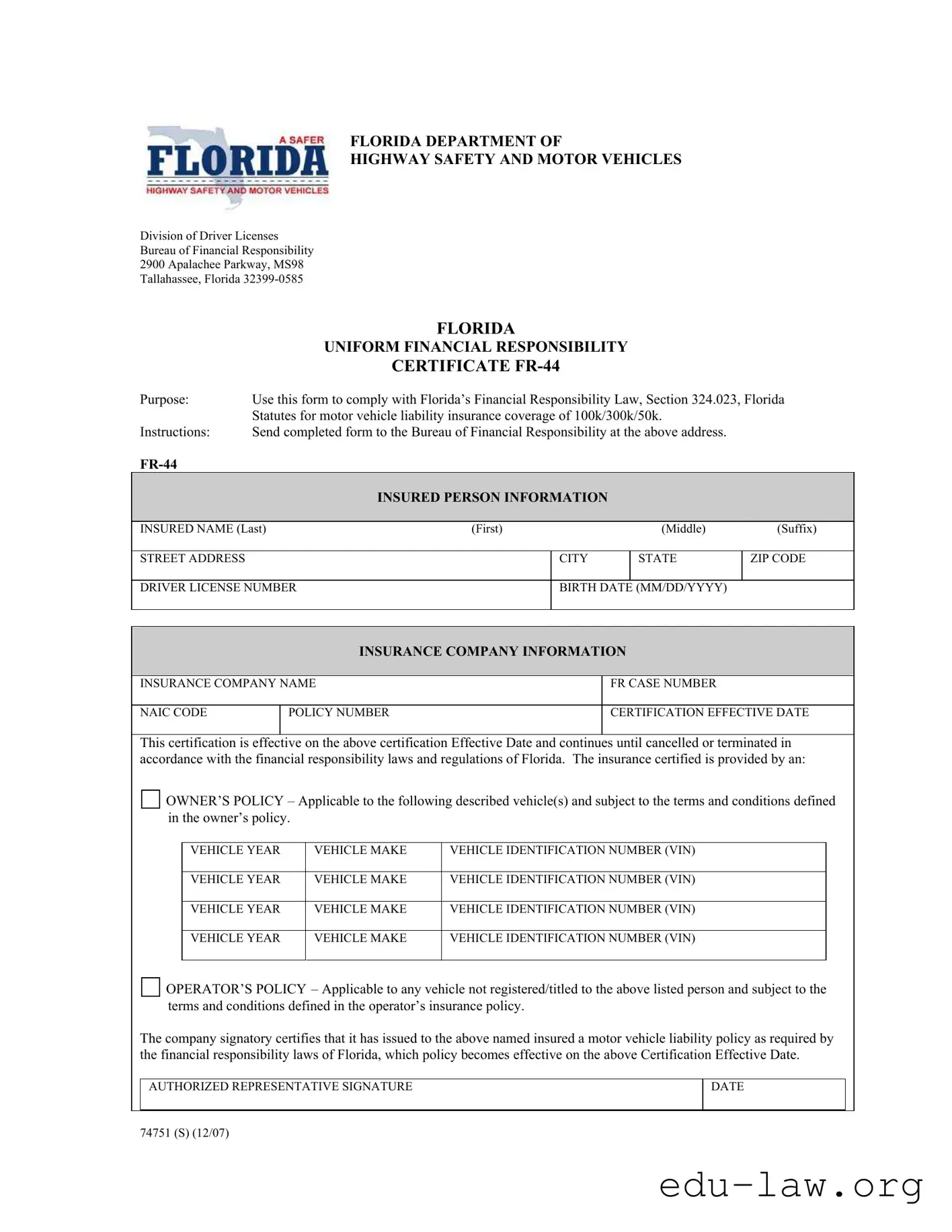

The FR44 form is an essential document for Florida drivers who need to demonstrate compliance with the state's Financial Responsibility Law. This law mandates specific motor vehicle liability insurance coverage amounts of $100,000 for bodily injury per person, $300,000 for bodily injury per accident, and $50,000 for property damage. The form serves as a certification that an individual has obtained the required insurance coverage, which is crucial for those who have had certain legal violations related to driving. Completing the FR44 involves providing personal information, including the insured person's name, address, and driver license number, along with details about the insurance company, such as the policy number and effective date. It is important to submit the completed form to the Bureau of Financial Responsibility, ensuring that it is sent to the correct address in Tallahassee. The FR44 is valid until it is canceled or terminated according to Florida's financial responsibility laws. Whether it pertains to an owner's policy for a registered vehicle or an operator's policy for vehicles not titled to the insured, this form plays a pivotal role in maintaining legal driving status in Florida.

FLORIDA DEPARTMENT OF

HIGHWAY SAFETY AND MOTOR VEHICLES

Division of Driver Licenses

Bureau of Financial Responsibility

2900 Apalachee Parkway, MS98

Tallahassee, Florida

|

|

|

FLORIDA |

|

|

|

|

||

|

|

UNIFORM FINANCIAL RESPONSIBILITY |

|

|

|||||

|

|

|

CERTIFICATE |

|

|

|

|

||

Purpose: |

Use this form to comply with Florida’s Financial Responsibility Law, Section 324.023, Florida |

|

|||||||

|

Statutes for motor vehicle liability insurance coverage of 100k/300k/50k. |

|

|

||||||

Instructions: |

Send completed form to the Bureau of Financial Responsibility at the above address. |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INSURED PERSON INFORMATION |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

INSURED NAME (Last) |

(First) |

|

(Middle) |

(Suffix) |

|

||||

|

|

|

|

|

|

|

|

|

|

STREET ADDRESS |

|

|

|

CITY |

|

STATE |

ZIP CODE |

|

|

|

|

|

|

|

|

|

|

||

DRIVER LICENSE NUMBER |

|

BIRTH DATE (MM/DD/YYYY) |

|

|

|||||

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

||||

|

|

INSURANCE COMPANY INFORMATION |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

INSURANCE COMPANY NAME |

|

|

|

FR CASE NUMBER |

|

|

|||

|

|

|

|

|

|

|

|

||

NAIC CODE |

|

POLICY NUMBER |

|

|

|

CERTIFICATION EFFECTIVE DATE |

|

||

|

|

|

|

|

|

|

|

|

|

This certification is effective on the above certification Effective Date and continues until cancelled or terminated in accordance with the financial responsibility laws and regulations of Florida. The insurance certified is provided by an:

OWNER’S POLICY – Applicable to the following described vehicle(s) and subject to the terms and conditions defined in the owner’s policy.

VEHICLE YEAR |

VEHICLE MAKE |

VEHICLE IDENTIFICATION NUMBER (VIN) |

|

|

|

VEHICLE YEAR |

VEHICLE MAKE |

VEHICLE IDENTIFICATION NUMBER (VIN) |

|

|

|

VEHICLE YEAR |

VEHICLE MAKE |

VEHICLE IDENTIFICATION NUMBER (VIN) |

|

|

|

VEHICLE YEAR |

VEHICLE MAKE |

VEHICLE IDENTIFICATION NUMBER (VIN) |

|

|

|

OPERATOR’S POLICY – Applicable to any vehicle not registered/titled to the above listed person and subject to the terms and conditions defined in the operator’s insurance policy.

The company signatory certifies that it has issued to the above named insured a motor vehicle liability policy as required by the financial responsibility laws of Florida, which policy becomes effective on the above Certification Effective Date.

|

AUTHORIZED REPRESENTATIVE SIGNATURE |

DATE |

|

|

|

|

|

74751 (S) (12/07)

| Fact Name | Details |

|---|---|

| Purpose | The FR-44 form is used to comply with Florida's Financial Responsibility Law, ensuring motor vehicle liability insurance coverage of at least $100,000 for bodily injury per person, $300,000 for bodily injury per accident, and $50,000 for property damage. |

| Governing Law | This form is governed by Section 324.023 of the Florida Statutes, which outlines the requirements for financial responsibility in motor vehicle insurance. |

| Submission Instructions | Completed forms must be sent to the Bureau of Financial Responsibility at the address provided: 2900 Apalachee Parkway, MS98, Tallahassee, Florida 32399-0585. |

| Effective Date | The certification on the FR-44 form becomes effective on the specified Certification Effective Date and remains valid until it is canceled or terminated according to Florida's financial responsibility laws. |

| Types of Policies | The FR-44 can certify either an owner's policy, which applies to specific vehicles, or an operator's policy, which covers any vehicle not registered to the insured individual. |

| Insured Information | The form requires detailed information about the insured person, including their name, address, driver license number, and birth date. |

| Insurance Company Details | Insurers must provide their name, FR case number, NAIC code, and policy number, ensuring transparency and accountability in the coverage provided. |

Filling out the FR44 form is an essential step for individuals seeking to comply with Florida's financial responsibility laws. This form requires specific information about the insured person and their insurance coverage. Once you have completed the form, it must be sent to the Bureau of Financial Responsibility to ensure that your vehicle liability insurance meets state requirements.

After you have filled out all sections of the form, double-check your entries for accuracy. Once confirmed, send the completed FR44 form to the Bureau of Financial Responsibility at the address provided at the top of the form. This step is crucial to ensure compliance with Florida's financial responsibility laws.

What is the purpose of the FR44 form in Florida?

The FR44 form is used to comply with Florida's Financial Responsibility Law. This law mandates specific motor vehicle liability insurance coverage amounts of $100,000 for bodily injury per person, $300,000 for total bodily injury per accident, and $50,000 for property damage. The form serves as a certification that the insured has the required coverage.

Who needs to file an FR44 form?

How does one complete the FR44 form?

Where should the completed FR44 form be sent?

What happens if the FR44 form is not filed?

How long is the FR44 certification effective?

Can the FR44 form be canceled?

What information is required about the vehicle on the FR44 form?

Is there a difference between an owner’s policy and an operator’s policy on the FR44 form?

What should I do if I have questions about the FR44 form?

Not providing complete insurer information. Ensure that the insurance company name, case number, NAIC code, and policy number are all filled out correctly.

Missing the certification effective date. This date is crucial, as it indicates when the insurance coverage begins.

Failing to sign the form. The authorized representative must sign and date the form for it to be valid.

Incorrectly entering the insured person's information. Double-check the name, address, and driver license number for accuracy.

Omitting vehicle details. Make sure to list all vehicles covered under the policy, including the year, make, and VIN.

Using an outdated version of the form. Always ensure you have the latest version to avoid any compliance issues.

Not understanding the difference between an owner's policy and an operator's policy. Choose the correct option based on your situation.

Providing incorrect birth date format. Use the MM/DD/YYYY format to avoid confusion.

Neglecting to check for spelling errors. Even small mistakes can lead to significant delays in processing.

Submitting the form to the wrong address. Always send it to the Bureau of Financial Responsibility at the specified address.

The FR44 form is essential for complying with Florida's Financial Responsibility Law, but it is often accompanied by other important documents. Each of these documents plays a role in ensuring that drivers meet the necessary insurance requirements and maintain their driving privileges. Here are some commonly used forms related to the FR44:

Understanding these documents can help drivers navigate the complexities of Florida's insurance requirements. Each form has its own purpose, but together they create a comprehensive framework for ensuring that drivers remain compliant and protected on the road.

The FR-44 form in Florida is similar to the SR-22 form, which is another type of financial responsibility certificate. Both documents serve to demonstrate that a driver has the required liability insurance coverage mandated by state law. The SR-22 is often required for drivers who have had certain violations, such as DUIs or serious traffic offenses, while the FR-44 specifically applies to those who need to prove higher coverage limits after similar infractions. The key difference lies in the coverage amounts, with the FR-44 requiring $100,000 per person, $300,000 per accident, and $50,000 for property damage.

The FR-44 form also resembles the Certificate of Insurance (COI), which is a document provided by an insurance company to verify that a policyholder has active insurance coverage. Both the FR-44 and COI serve as proof of insurance, but the FR-44 is specifically tailored for compliance with Florida's Financial Responsibility Law. A COI may not specify the same minimum coverage limits required by the FR-44, making the latter a more stringent requirement for certain drivers.

Another similar document is the Financial Responsibility Certificate (FR-19). This form is used to show that a driver has met the minimum insurance requirements after a traffic violation. While the FR-19 is generally less comprehensive than the FR-44, both documents are intended to ensure that drivers maintain adequate insurance coverage. The FR-44’s higher coverage limits make it a more robust option for those facing serious violations.

The FR-44 can also be compared to the Proof of Insurance Card, which is a simpler document that drivers must carry to demonstrate they have insurance. While a Proof of Insurance Card provides basic information about coverage, the FR-44 includes specific details about the required liability limits and is submitted to the state for regulatory purposes. Thus, the FR-44 serves a more formal role in compliance with state laws.

Another document with similarities is the Non-Owner SR-22. This form is for individuals who do not own a vehicle but still need to provide proof of liability insurance. Like the FR-44, the Non-Owner SR-22 is often required after a traffic violation. However, the FR-44 mandates higher coverage limits than what might be required for a standard Non-Owner SR-22, making it a more stringent option for those with specific legal requirements.

The FR-44 is also akin to the Motor Vehicle Liability Insurance Policy itself. This policy outlines the coverage a driver has in case of an accident. While the FR-44 serves as a certification of this coverage, the actual insurance policy details the terms and conditions under which coverage is provided. Therefore, the FR-44 acts as a summary document for regulatory compliance, while the insurance policy contains the full legal agreement between the insurer and the insured.

Another document that shares similarities with the FR-44 is the Certificate of Financial Responsibility. This certificate is issued by an insurance company to confirm that a driver meets the state’s minimum insurance requirements. Both documents aim to establish proof of financial responsibility, but the FR-44 specifically outlines higher coverage limits, making it a more specialized requirement for certain drivers.

Lastly, the FR-44 can be compared to the Commercial Auto Insurance Policy. While primarily aimed at businesses, this policy also requires proof of financial responsibility. Both documents ensure that adequate insurance coverage is in place; however, the FR-44 is specifically designed for individual drivers who have faced legal issues, while the Commercial Auto Insurance Policy is more comprehensive and tailored for business use.

When filling out the FR44 Florida form, it is crucial to follow specific guidelines to ensure accuracy and compliance. Here is a list of things to do and avoid:

By adhering to these guidelines, you can help ensure that your FR44 form is processed smoothly and efficiently.

Understanding the FR44 form in Florida can be challenging, especially with the various misconceptions surrounding it. Here are four common misunderstandings about the FR44 form:

By clearing up these misconceptions, individuals can better navigate their responsibilities regarding the FR44 form and ensure compliance with Florida's financial responsibility laws.

The FR44 form is an important document for compliance with Florida’s Financial Responsibility Law. Below are key takeaways to consider when filling out and using this form: