The Florida Promissory Note serves as a vital legal document within the realm of personal and business finance. It outlines the agreement between a borrower and a lender, detailing the amount borrowed, the interest rates, and the repayment terms. This form ensures that both parties understand their obligations and rights. Typically, it includes critical elements such as the repayment schedule, any collateral involved, and provisions for late payment or default. Furthermore, the document is often signed in the presence of a witness or a notary, adding a layer of authenticity. Utilizing a Florida Promissory Note helps protect the interests of all involved parties, providing clarity and reducing potential disputes related to loan agreements. This form not only promotes accountability but also fosters trust between borrowers and lenders.

Florida Promissory Note Template

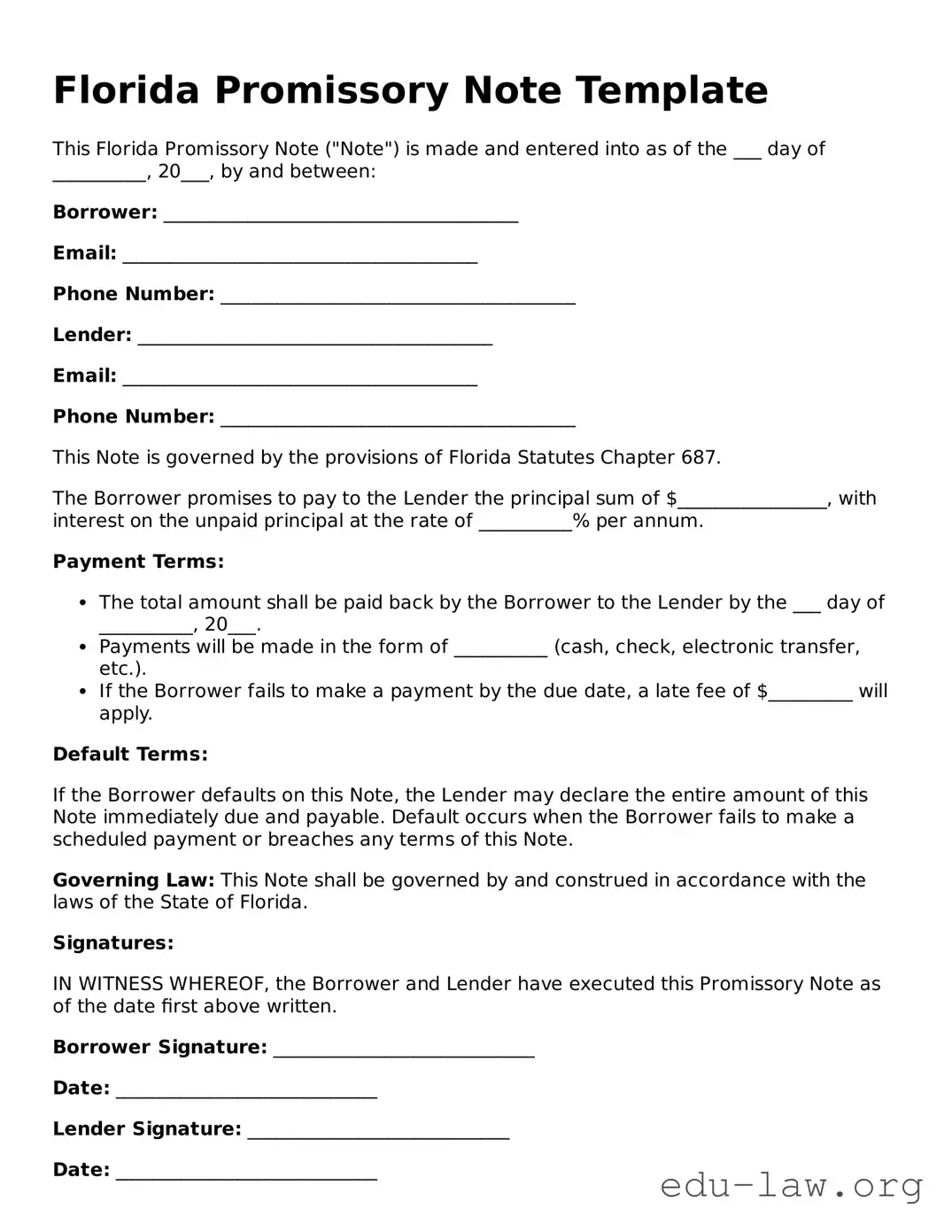

This Florida Promissory Note ("Note") is made and entered into as of the ___ day of __________, 20___, by and between:

Borrower: ______________________________________

Email: ______________________________________

Phone Number: ______________________________________

Lender: ______________________________________

Email: ______________________________________

Phone Number: ______________________________________

This Note is governed by the provisions of Florida Statutes Chapter 687.

The Borrower promises to pay to the Lender the principal sum of $________________, with interest on the unpaid principal at the rate of __________% per annum.

Payment Terms:

Default Terms:

If the Borrower defaults on this Note, the Lender may declare the entire amount of this Note immediately due and payable. Default occurs when the Borrower fails to make a scheduled payment or breaches any terms of this Note.

Governing Law: This Note shall be governed by and construed in accordance with the laws of the State of Florida.

Signatures:

IN WITNESS WHEREOF, the Borrower and Lender have executed this Promissory Note as of the date first above written.

Borrower Signature: ____________________________

Date: ____________________________

Lender Signature: ____________________________

Date: ____________________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money on demand or at a predetermined date. |

| Governing Law | Florida Statutes, Chapter 673 (Uniform Commercial Code – Negotiable Instruments). |

| Parties Involved | The document involves at least two parties: the borrower (maker) and the lender (payee). |

| Enforceability | A properly executed promissory note is legally enforceable in Florida, provided it contains the necessary elements. |

Once you've gathered the necessary information, you can begin filling out the Florida Promissory Note form. Carefully follow the steps outlined below to ensure accuracy and completeness.

After the form is completed and signed, make copies for both the lender and borrower. This ensures both parties have a record of the agreement. It’s advisable to store the original in a safe place to maintain its integrity and your legal rights.

What is a Florida Promissory Note?

A Florida Promissory Note is a legally binding document in which one party, known as the borrower, promises to pay a specific amount of money to another party, referred to as the lender. This note outlines the loan’s details, such as the amount borrowed, interest rate, payment schedule, and maturity date. It serves as a clear record of the borrowing agreement and can be used in court if necessary. The form helps ensure all parties understand their obligations and rights under the agreement.

Why is a Promissory Note important?

A Promissory Note is essential for several reasons. First, it provides a written record of the transaction, ensuring that both parties are on the same page regarding the terms of the loan. This clarity can help avoid misunderstandings or disputes later on. Additionally, a properly executed Promissory Note can aid in collecting the debt if the borrower fails to repay. It essentially offers legal protection for both the lender and the borrower, promoting transparency and accountability in the lending process.

How should a Promissory Note be executed in Florida?

To execute a Promissory Note in Florida, both parties need to agree to its terms. The note must be signed by the borrower, and it is also advisable for the lender to sign it. While notarization is not required for the note to be valid, having it notarized can enhance its credibility and may be necessary for certain legal processes. It is critical that all the details, including the repayment terms and interest rate, are clear and unambiguous to avoid future complications.

What happens if the borrower fails to repay the Promissory Note?

If a borrower fails to repay the amount due on the Promissory Note, the lender has several options. First, they may pursue informal methods of collection, such as contacting the borrower to resolve the issue. If this does not yield results, the lender might consider legal action to collect the debt. This could involve filing a lawsuit to seek a judgment against the borrower. If successful, the lender may have the right to garnish wages or place liens on property owned by the borrower. It’s important for both parties to communicate openly and honestly to avoid such situations.

Incorrect Amount: Many individuals fail to enter the correct loan amount. This figure must match the agreed-upon terms between the lender and borrower.

Missing Signatures: It is crucial that all parties involved sign the document. Omitting a signature can render the agreement unenforceable.

Inaccurate Date: The date of execution should be clearly noted. An incorrect or missing date can lead to confusion about when the terms begin.

Failure to Specify Terms: A common error is not providing detailed repayment terms. Interest rates, payment schedules, and consequences for late payments must all be clearly articulated.

When dealing with the Florida Promissory Note, several other forms and documents may also be necessary to ensure a smooth transaction. Below are some commonly used documents that accompany a promissory note in Florida.

Understanding these additional documents can help ensure all parties involved are well-informed and protected throughout the lending process. Each document plays a crucial role in providing clarity and establishing mutual agreement between the lender and borrower.

A mortgage is a document that establishes a loan agreement between a borrower and lender, secured by real property. Like a promissory note, it outlines repayment terms, including interest and payment schedules. However, a mortgage also grants the lender a security interest in the property, allowing repossession if the borrower defaults on payments. In essence, while a promissory note is primarily a promise to repay, a mortgage provides a layer of protection for the lender through the collateral of real estate.

A loan agreement is often used for personal loans, business loans, or other types of financing. Similar to a promissory note, it details the amount borrowed, the repayment schedule, and the interest rate. However, a loan agreement can encompass multiple loans and may contain additional terms regarding fees, responsibilities, and default consequences. The key difference lies in the comprehensive nature of the loan agreement, which can cover a variety of lending scenarios beyond a single promise to repay.

A deed of trust is used in some states as an alternative to a mortgage. It involves three parties: the borrower, the lender, and a third-party trustee. This document outlines the terms of the loan as well as the rights of all parties. Like a promissory note, a deed of trust includes repayment details, but it also specifies what happens in the event of default, such as the process for foreclosure. Both documents are related to borrowing, but a deed of trust introduces an additional party for security purposes.

A demand note is a specific type of promissory note that allows the lender to request repayment at any time. While both documents contain a promise to pay, the key difference is in the repayment terms. A demand note lacks a fixed schedule for repayment, often allowing flexibility for the lender. This can be beneficial for those needing immediate repayment options but may pose challenges to borrowers who may not be prepared for unplanned payments.

A personal guarantee is a document that provides assurance from an individual that a debt will be repaid, often used in business loans. While it functions similarly to a promissory note in that it creates a promise regarding debt repayment, it usually accompanies a larger loan agreement. The key aspect of a personal guarantee is that it holds an individual liable for the debt if the original borrower fails to pay. Thus, it extends the financial responsibility beyond the primary borrower.

A conditional sale agreement allows the seller to retain ownership of an item until the buyer has paid the total purchase price. Similar to a promissory note, it specifies payment arrangements and consequences for default. However, the conditional sale agreement includes specific terms for possession and ownership transfer. The borrower is granted use of the item while payment is being made, transitioning to ownership upon fulfilling the agreement’s conditions.

A rental agreement outlines the terms of renting property. This document is similar to a promissory note in that it specifies payment terms; however, it generally involves recurring payments such as monthly rent. The rental agreement also includes specifics about the property, duration of lease, and responsibilities of both parties. While a promissory note focuses on debt repayment, a rental agreement centers on the leasing of property and the associated obligations.

An installment agreement is commonly used for structured repayments on a larger debt. Comparable to a promissory note, it breaks down the total amount into smaller, manageable payments over time. This type of agreement supports both individuals and businesses looking to repay debts systematically. The primary difference lies in its application to debts that require a step-by-step repayment approach, allowing flexibility and financial planning for borrowers.

A rebate agreement establishes terms for a return payment or discount provided after a product purchase. While not directly a borrowing instrument, it shares similarities with promissory notes regarding financial transactions. Both documents outline specific conditions to be met for payments to be made. The rebate agreement often serves in sales contexts, leveraging agreements to encourage consumer purchases, while promissory notes primarily deal with debt obligations.

Lastly, an investment agreement defines the terms of an investment arrangement between individuals or entities. Like a promissory note, it includes financial obligations and detailed terms. However, it often covers broader expectations regarding returns, timelines, and responsibilities of the parties involved. While promissory notes focus on loan repayments, investment agreements delve into shared risks and rewards within an investment context.

When completing the Florida Promissory Note form, certain practices can ensure your document is valid and enforceable. Here’s a list of dos and don’ts to consider:

These actions contribute to the clarity and effectiveness of the Promissory Note, providing a stronger legal foundation for the agreement between parties.

This is not true. While notarization can provide an additional layer of authenticity, it is not a requirement for a Promissory Note to be enforceable in Florida.

Many believe that such documents are necessary only for significant sums. In fact, a Promissory Note is useful for any loan, regardless of the amount, as it helps establish clear terms.

This is misleading. Parties involved can amend a Promissory Note by mutual agreement, but it should be documented properly to avoid any future disputes.

Relying solely on verbal agreements can lead to misunderstandings. A written Promissory Note provides clarity and proof of the loan terms.

While both documents deal with loans, a Promissory Note specifically outlines the borrower's promise to repay, whereas a loan agreement may include additional terms and conditions.

This is incorrect. Individuals, businesses, and organizations can create and issue Promissory Notes to formalize loan transactions among private parties.

This misunderstanding can be problematic. A Promissory Note does not inherently secure collateral unless it explicitly states that security is involved. Additional documents may be needed for that purpose.

Some assume all Promissory Notes must have fixed interest rates. However, they can be either fixed or variable, depending on the agreement between the parties involved.

This is false. A Promissory Note can be contested under certain circumstances, such as if fraud or undue influence was involved in the signing.

When filling out and using a Florida Promissory Note form, it’s important to keep several key points in mind.

By paying attention to these key details, you can ensure that your Florida Promissory Note serves its intended purpose effectively.

Texas Promissory Note Requirements - This document can streamline financial transactions and improve clarity in communications.

Promissory Note Georgia - A promissory note typically contains the borrower's name and contact information.

Sample Promissory Note California - The borrower usually agrees to repay the loan in installments over a set period.

Create a Promissory Note - The promissory note can be modified if both parties agree in writing.