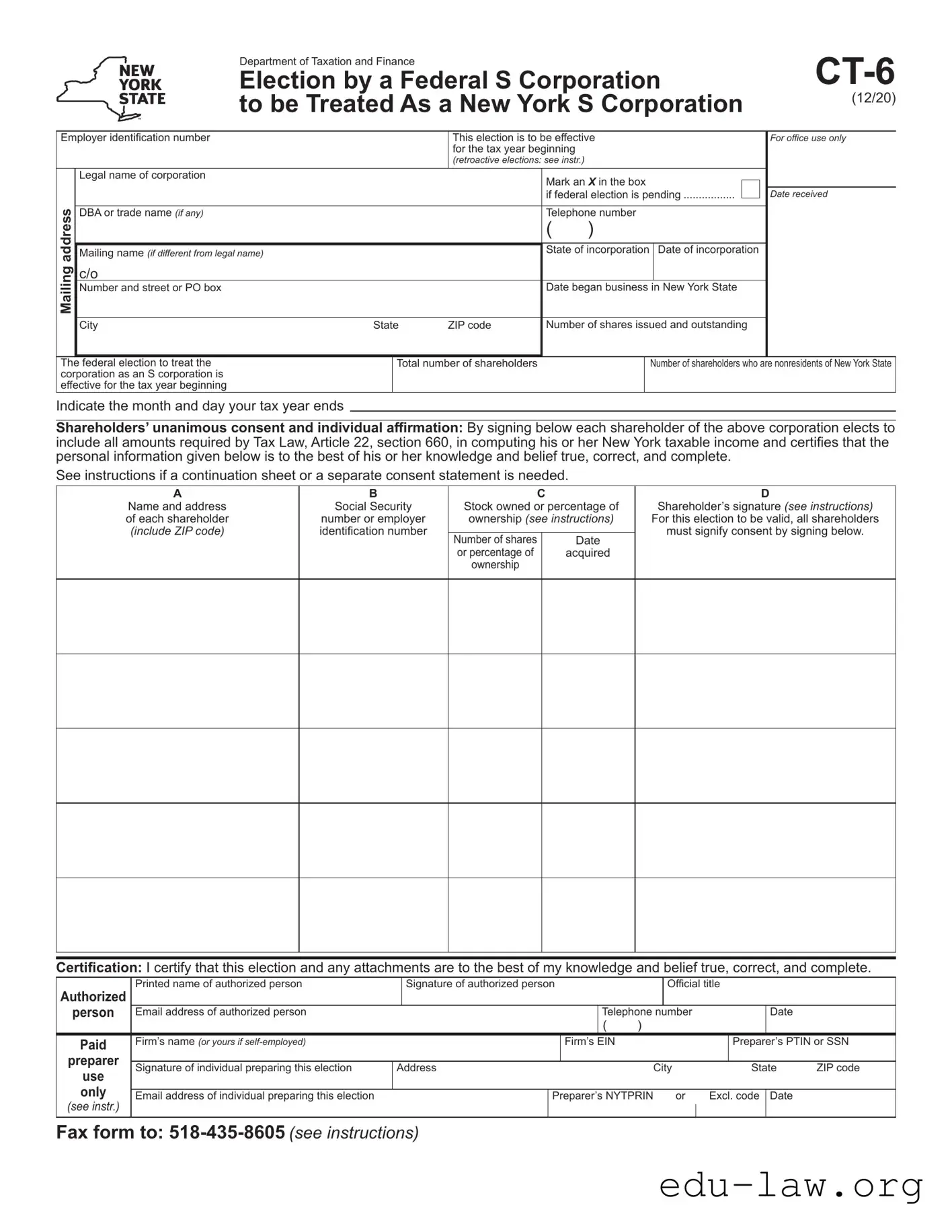

The CT-6 form is a crucial document for corporations seeking to elect S Corporation status in New York. This form allows a federal S Corporation to be recognized as an S Corporation under New York State law. It requires detailed information, including the corporation's legal name, employer identification number, and the date the business began operations in New York. Additionally, it asks for the total number of shares issued and outstanding, as well as the number of shareholders, particularly noting those who are nonresidents of New York State. Shareholder consent is a vital component; all shareholders must affirm their agreement by signing the form, thereby certifying the accuracy of the information provided. The form also includes sections for an authorized person's certification and the preparer's information, ensuring that all submissions are properly documented. Completing the CT-6 form accurately is essential for compliance with state tax laws and for securing the desired tax treatment for the corporation.

Department of Taxation and Finance |

|

Election by a Federal S Corporation |

|

to be Treated As a New York S Corporation |

(12/20) |

|

Employer identification number |

||

address |

|

Legal name of corporation |

|

||

|

DBA or trade name (if any) |

|

|

Mailing name (if different from legal name) |

|

|

||

|

|

|

Mailing |

|

c/o |

|

Number and street or PO box |

|

|

|

|

City

This election is to be effective for the tax year beginning

(retroactive elections: see instr.)

|

|

Mark an X in the box |

|

|

|

|

|

|

|

||

|

|

if federal election is pending |

|

|

|

|

|

|

|||

|

|

Telephone number |

|||

|

|

( ) |

|||

|

|

State of incorporation |

Date of incorporation |

||

|

|

Date began business |

|

|

|

|

|

in New York State |

|||

State |

ZIP code |

Number of shares issued and outstanding |

|||

For office use only

Date received

The federal election to treat the corporation as an S corporation is effective for the tax year beginning

Total number of shareholders |

Number of shareholders who are nonresidents of New York State |

Indicate the month and day your tax year ends

Shareholders’ unanimous consent and individual affirmation: By signing below each shareholder of the above corporation elects to include all amounts required by Tax Law, Article 22, section 660, in computing his or her New York taxable income and certifies that the personal information given below is to the best of his or her knowledge and belief true, correct, and complete.

See instructions if a continuation sheet or a separate consent statement is needed.

A |

B |

|

C |

D |

|

Name and address |

Social Security |

Stock owned or percentage of |

Shareholder’s signature (see instructions) |

||

of each shareholder |

number or employer |

ownership (see instructions) |

For this election to be valid, all shareholders |

||

(include ZIP code) |

identification number |

|

|

|

must signify consent by signing below. |

Number of shares |

|

Date |

|||

|

|

|

|

||

|

|

or percentage of |

|

acquired |

|

|

|

ownership |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Certification: I certify that this election and any attachments are to the best of my knowledge and belief true, correct, and complete.

Authorized |

Printed name of authorized person |

|

Signature of authorized person |

|

|

Official title |

|

||||||

person |

Email address of authorized person |

|

|

|

|

Telephone number |

|

|

Date |

|

|||

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

Paid |

Firm’s name (or yours if |

|

|

|

Firm’s |

EIN |

|

|

|

|

Preparer’s PTIN or SSN |

||

preparer |

|

|

|

|

|

|

|

|

|

||||

Signature of individual preparing this election |

Address |

|

City |

|

State |

ZIP code |

|||||||

use |

|

|

|

|

|

|

|

|

|

|

|

|

|

only |

|

|

|

|

|

|

|

|

|

|

|||

Email address of individual preparing this election |

|

|

Preparer’s NYTPRIN |

|

or |

Excl. code |

Date |

|

|||||

(see instr.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fax form to:

| Fact Name | Description |

|---|---|

| Purpose | The CT-6 form allows a federal S corporation to elect to be treated as a New York S corporation for state tax purposes. |

| Eligibility | Only corporations that are federally recognized as S corporations can file this form to gain New York S corporation status. |

| Effective Date | The election is effective for the tax year beginning on the date specified in the form. Retroactive elections are permitted under certain conditions. |

| Shareholder Consent | All shareholders must provide their consent by signing the form, indicating their agreement to include required amounts in their New York taxable income. |

| Governing Law | This form is governed by New York Tax Law, Article 22, section 660. |

| Submission Method | The completed form can be faxed to 518-435-8605, as specified in the instructions provided with the form. |

Once the CT-6 form is filled out, it must be submitted to the appropriate tax authority for processing. Make sure to review all entries for accuracy before sending. Keep a copy for your records.

What is the purpose of the CT-6 form?

The CT-6 form allows a federal S corporation to elect to be treated as a New York S corporation for tax purposes. This election enables the corporation to benefit from certain tax treatments specific to New York State. It is essential for corporations wishing to align their federal and state tax statuses.

Who needs to file the CT-6 form?

This form must be filed by corporations that have elected federal S corporation status and want to extend that status to New York State. If a corporation is incorporated in New York and has shareholders who are residents or non-residents, it should consider filing this form to ensure compliance with state tax laws.

What information is required to complete the CT-6 form?

To complete the CT-6 form, you will need to provide various details about the corporation, including its legal name, address, employer identification number, and date of incorporation. Additionally, the form requires information about shareholders, such as their names, addresses, Social Security numbers, and the percentage of stock owned. It is also necessary to indicate the tax year end and obtain unanimous consent from all shareholders.

Is there a deadline for filing the CT-6 form?

The CT-6 form should be filed by the 15th day of the third month of the tax year for which the election is to be effective. If you are making a retroactive election, specific instructions must be followed to ensure compliance. It is crucial to adhere to this timeline to avoid any issues with your corporation’s tax status.

What happens if all shareholders do not consent to the election?

If all shareholders do not provide their consent by signing the CT-6 form, the election will not be valid. It is essential that every shareholder agrees to the election for it to take effect. Without unanimous consent, the corporation will not be treated as a New York S corporation, which could lead to different tax implications.

How can I submit the CT-6 form?

The completed CT-6 form can be submitted via fax to the New York Department of Taxation and Finance at 518-435-8605. Ensure that all required information is filled out accurately before submission to avoid delays or rejections. If you prefer, you may also consult with a tax professional for assistance in preparing and filing the form.

Missing Employer Identification Number (EIN): Many people forget to include the EIN, which is essential for identifying the corporation.

Incorrect Legal Name: It’s crucial to provide the exact legal name of the corporation as registered. Any discrepancies can lead to delays.

Failure to Indicate the Effective Date: Not specifying the tax year for which the election is effective can create confusion and may invalidate the election.

Omitting Shareholder Consent: All shareholders must sign to indicate their consent. Missing signatures can jeopardize the validity of the form.

Incorrect Number of Shares: Providing an inaccurate count of shares issued and outstanding can lead to complications in processing.

Not Including Contact Information: Failing to provide a telephone number or email address for the authorized person can hinder communication with tax authorities.

Inaccurate Tax Year End Date: Indicating the wrong month and day for the tax year end can result in misalignment with tax obligations.

Neglecting to Review Instructions: Skipping the instructions may lead to missing important details that ensure the form is filled out correctly.

The CT-6 form is essential for corporations seeking to elect S corporation status in New York. However, several other documents are often required or beneficial to accompany this form. Below is a list of these documents, each serving a specific purpose in the election process.

Gathering these documents can streamline the process of electing S corporation status in New York. Each plays a crucial role in ensuring that the election is valid and compliant with both state and federal regulations.

The CT-6 form is similar to the IRS Form 2553, which is used by corporations to elect S corporation status at the federal level. Both forms require information about the corporation, including its legal name, address, and the number of shareholders. Just like the CT-6, Form 2553 requires unanimous consent from all shareholders, ensuring that everyone is on board with the election. This parallel highlights the importance of shareholder agreement in both state and federal processes.

Another document that shares similarities with the CT-6 is the New York State Form CT-3, which is the general business corporation franchise tax return. While CT-3 is primarily focused on tax reporting, it also requires detailed information about the corporation's structure, including its shareholders and financial status. Both forms aim to ensure compliance with New York tax law, making it essential for corporations to maintain accurate records and transparency.

The IRS Form 1120S is another related document. This form is the annual tax return for S corporations, similar to how the CT-6 is a declaration of intent to be treated as an S corporation in New York. Both forms require information about the corporation's income, deductions, and credits, and they serve to inform the respective tax authorities about the corporation's financial activities and status.

The CT-6 also resembles the New York State Form CT-4, which is an application for a New York S corporation election. Like the CT-6, Form CT-4 requires the corporation to provide information about its shareholders and their consent to the election. Both forms facilitate the process of becoming recognized as an S corporation in New York, ensuring that the corporation can take advantage of the associated tax benefits.

Similar to the CT-6 is the IRS Form 941, which is the employer's quarterly federal tax return. While the focus of Form 941 is on payroll taxes, both forms require accurate reporting of corporate information and compliance with tax obligations. Each form necessitates that corporations keep precise records and submit them in a timely manner to avoid penalties.

The New York State Form CT-5 is another document akin to the CT-6. This form is used for a New York corporation to apply for a sales tax exemption. Both forms involve corporate structure and require consent from shareholders. They also ensure that the corporation complies with state regulations while taking advantage of specific tax benefits.

The IRS Form 1065, which is used for partnerships, shares some similarities with the CT-6 as well. Both forms require detailed information about the business structure and ownership. While the CT-6 focuses on S corporations, the 1065 emphasizes partnerships, yet both emphasize transparency and the necessity of obtaining consent from all owners or shareholders involved.

Another similar document is the New York State Form IT-201, which is the resident income tax return. While it serves individual taxpayers, it also requires information about income sources and tax obligations similar to the CT-6. Both forms are essential for ensuring that taxpayers, whether corporations or individuals, fulfill their state tax responsibilities.

The CT-6 form also has parallels with the New York State Form IT-203, which is the non-resident and part-year resident income tax return. Like the CT-6, it requires information about income sources and the consent of shareholders or partners. Both forms help ensure that the respective tax authorities have the necessary information to assess tax liabilities accurately.

Lastly, the CT-6 is similar to the New York State Form CT-3-A, which is an annual report for corporations. This form requires details about the corporation's financial performance and ownership structure, much like the CT-6. Both documents are vital for maintaining compliance with New York State regulations and ensuring accurate reporting of corporate activities.

When filling out the CT-6 form, it’s important to approach the task with care. Here’s a helpful list of things to do and avoid:

By following these guidelines, you can navigate the CT-6 form with confidence and clarity. Good luck!

Here are five common misconceptions about the Fill Out CT-6 form, which is used for the election by a federal S corporation to be treated as a New York S corporation:

Filling out the CT-6 form is an important step for a federal S corporation seeking to be recognized as a New York S corporation. Here are some key takeaways to keep in mind:

Completing the CT-6 form accurately will help ensure your corporation's compliance with New York State tax regulations. Take your time to review each section carefully before submission.