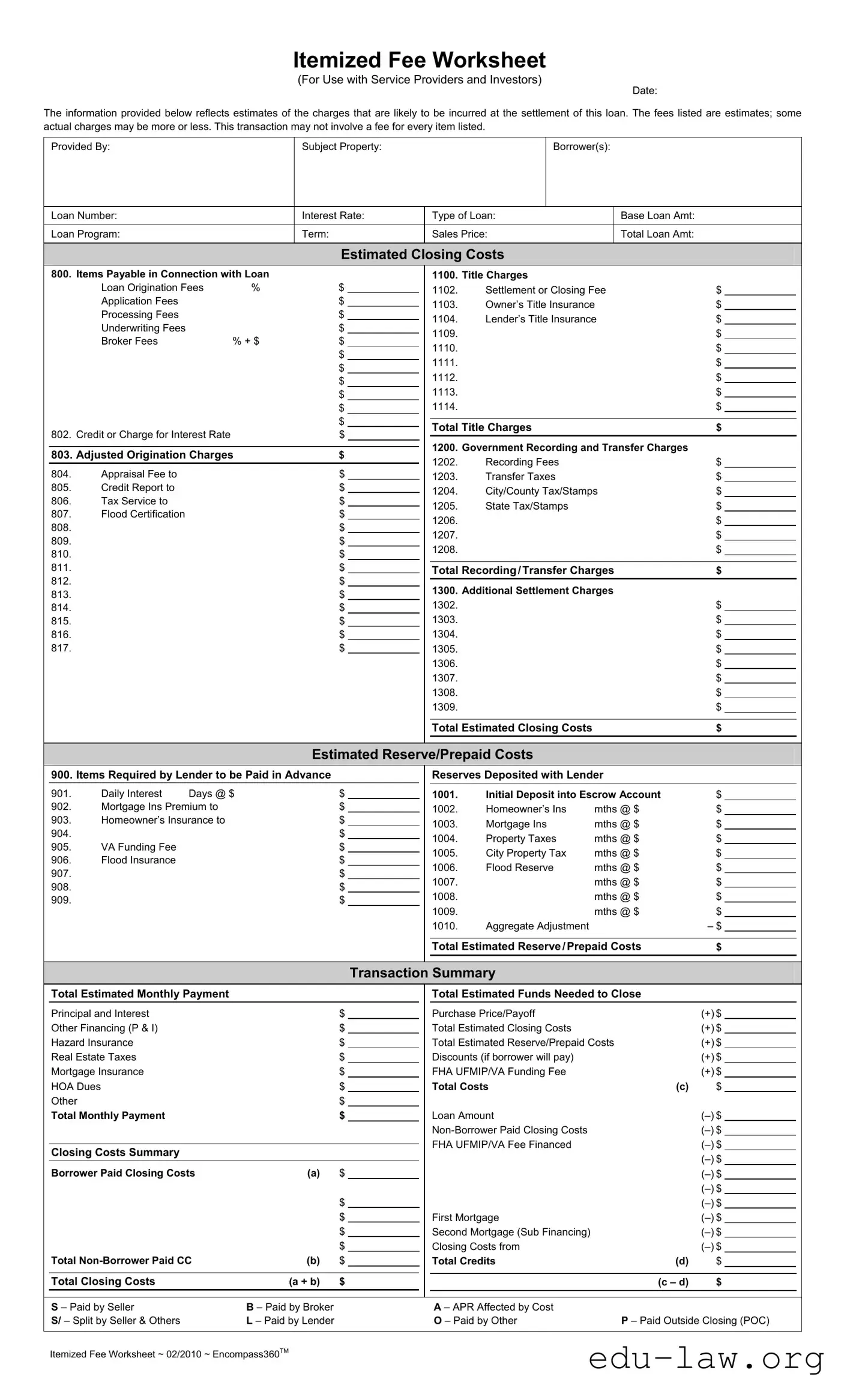

The Fee Worksheet form serves as a critical tool for both service providers and investors involved in real estate transactions. This comprehensive document outlines the estimated charges that borrowers can expect to encounter at the closing of a loan. It meticulously details various categories of fees, such as title charges, government recording and transfer charges, and additional settlement costs. Each section provides space for itemizing specific fees, including loan origination fees, appraisal fees, and insurance premiums, among others. The form also allows for the estimation of closing costs, reserves, and prepaid costs, giving borrowers a clearer picture of their financial obligations. By providing a structured format, the Fee Worksheet helps ensure that all parties have a transparent understanding of the costs associated with the transaction. Furthermore, it emphasizes the importance of estimates, as actual charges may vary, thus encouraging careful review and consideration prior to closing. This document not only aids in financial planning but also enhances communication between borrowers, lenders, and other involved parties, fostering a smoother transaction process.

Itemized Fee Worksheet

(For Use with Service Providers and Investors)

Date:

The information provided below reflects estimates of the charges that are likely to be incurred at the settlement of this loan. The fees listed are estimates; some actual charges may be more or less. This transaction may not involve a fee for every item listed.

|

Provided By: |

|

|

Subject Property: |

|

|

|

Borrower(s): |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Loan Number: |

|

|

Interest Rate: |

|

Type of Loan: |

|

Base Loan Amt: |

|

|

|

||||||

|

Loan Program: |

|

|

Term: |

|

|

|

|

Sales Price: |

|

Total Loan Amt: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

Estimated Closing Costs |

|

|

|

|

|

||||||

800. |

Items Payable in Connection with Loan |

|

|

|

1100. |

Title Charges |

|

|

|

|

|

||||||

|

|

Loan Origination Fees |

% |

|

$ |

|

|

1102. |

Settlement or Closing Fee |

$ |

|

|

|||||

|

|

|

|

|

|||||||||||||

|

|

Application Fees |

|

|

|

$ |

|

|

1103. |

Owner’s Title Insurance |

$ |

|

|

||||

|

|

|

|

|

|

|

|||||||||||

|

|

Processing Fees |

|

|

|

$ |

|

|

1104. |

Lender’s Title Insurance |

$ |

|

|

||||

|

|

Underwriting Fees |

|

|

|

$ |

|

|

|

|

|||||||

|

|

|

|

|

|

|

1109. |

|

|

|

|

$ |

|

|

|||

|

|

Broker Fees |

|

% + $ |

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

1110. |

|

|

|

|

$ |

|

|

||||

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

1111. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

1112. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

1113. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

$ |

|

|

1114. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Title Charges |

|

|

$ |

|

|

|||

802. |

Credit or Charge for Interest Rate |

|

|

$ |

|

|

|

|

|

|

|

||||||

|

|

|

|

1200. |

Government Recording and Transfer Charges |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

803. Adjusted Origination Charges |

$ |

|

|

|

|

|

||||||||||

|

|

|

1202. |

Recording Fees |

|

|

$ |

|

|

||||||||

804. |

Appraisal Fee to |

|

|

|

$ |

|

|

|

|

|

|

||||||

|

|

|

|

|

1203. |

Transfer Taxes |

|

|

$ |

|

|

||||||

|

|

|

|

|

|

|

|||||||||||

805. |

Credit Report to |

|

|

|

$ |

|

|

1204. |

City/County Tax/Stamps |

$ |

|

|

|||||

806. |

Tax Service to |

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

1205. |

State Tax/Stamps |

|

|

$ |

|

|

||||||

807. |

Flood Certification |

|

|

|

$ |

|

|

|

|

|

|

||||||

|

|

|

|

|

1206. |

|

|

|

|

$ |

|

|

|||||

808. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

1207. |

|

|

|

|

$ |

|

|

||||

809. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

1208. |

|

|

|

|

$ |

|

|

||||

810. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

811. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

Total Recording/Transfer Charges |

$ |

|

|

|||||||

|

|

|

|

|

|

||||||||||||

812. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1300. |

Additional Settlement Charges |

|

|

|

|||||||

813. |

|

|

|

|

$ |

|

|

|

|

|

|||||||

814. |

|

|

|

|

$ |

|

|

1302. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

815. |

|

|

|

|

$ |

|

|

1303. |

|

|

|

|

$ |

|

|

||

816. |

|

|

|

|

$ |

|

|

1304. |

|

|

|

|

$ |

|

|

||

817. |

|

|

|

|

$ |

|

|

1305. |

|

|

|

|

$ |

|

|

||

|

|

|

|

|

|

|

|

|

1306. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

1307. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

1308. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

1309. |

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Total Estimated Closing Costs |

|

|

$ |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

Estimated Reserve/Prepaid Costs |

|

|

|

|

|

|||||||

|

900. Items Required by Lender to be Paid in Advance |

|

|

|

|

Reserves Deposited with Lender |

|

|

|

||||||||

901. |

Daily Interest |

Days @ $ |

$ |

|

|

1001. |

Initial Deposit into Escrow Account |

$ |

|

|

|||||||

902. |

Mortgage Ins Premium to |

|

|

$ |

|

|

1002. |

Homeowner’s Ins |

mths @ $ |

$ |

|

|

|||||

|

|

|

|

|

|

||||||||||||

903. |

Homeowner’s Insurance to |

|

|

$ |

|

|

1003. |

Mortgage Ins |

mths @ $ |

$ |

|

|

|||||

904. |

|

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

|

1004. |

Property Taxes |

mths @ $ |

$ |

|

|

||||||

905. |

VA Funding Fee |

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

1005. |

City Property Tax |

mths @ $ |

$ |

|

|

|||||||

906. |

Flood Insurance |

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

1006. |

Flood Reserve |

mths @ $ |

$ |

|

|

|||||||

907. |

|

|

|

|

$ |

|

|

|

|

||||||||

|

|

|

|

|

|

1007. |

|

|

mths @ $ |

$ |

|

|

|||||

908. |

|

|

|

|

$ |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

1008. |

|

|

mths @ $ |

$ |

|

|

|||||

909. |

|

|

|

|

$ |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

1009. |

|

|

mths @ $ |

$ |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

1010. |

Aggregate Adjustment |

|

|

– $ |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

Total Estimated Reserve/Prepaid Costs |

$ |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

Transaction Summary |

|

|

|

|

|

|||||

|

Total Estimated Monthly Payment |

|

|

|

|

|

|

Total Estimated Funds Needed to Close |

|

|

|

||||||

|

Principal and Interest |

|

|

|

$ |

|

|

|

Purchase Price/Payoff |

|

|

(+) $ |

|

|

|||

|

Other Financing (P & I) |

|

|

|

$ |

|

|

|

Total Estimated Closing Costs |

|

|

(+) $ |

|

|

|||

|

Hazard Insurance |

|

|

|

$ |

|

|

|

Total Estimated Reserve/Prepaid Costs |

(+) $ |

|

|

|||||

|

Real Estate Taxes |

|

|

|

$ |

|

|

|

Discounts (if borrower will pay) |

|

|

(+) $ |

|

|

|||

|

Mortgage Insurance |

|

|

|

$ |

|

|

|

FHA UFMIP/VA Funding Fee |

|

|

(+) $ |

|

|

|||

|

HOA Dues |

|

|

|

$ |

|

|

|

Total Costs |

|

(c) |

$ |

|

|

|||

|

Other |

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Monthly Payment |

|

|

|

$ |

|

|

|

Loan Amount |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

FHA UFMIP/VA Fee Financed |

|

|

|

|

|||

|

Closing Costs Summary |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Borrower Paid Closing Costs |

|

(a) |

$ |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

First Mortgage |

|

|

|

|

|||

|

|

|

|

|

|

$ |

|

|

|

Second Mortgage (Sub Financing) |

|

|

|

|

|||

|

Total |

|

(b) |

$ |

|

|

|

Closing Costs from |

|

|

|||||||

|

|

$ |

|

|

|

Total Credits |

|

(d) |

$ |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Total Closing Costs |

|

(a + b) |

$ |

|

|

|

|

|

|

|

(c – d) |

$ |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

S – Paid by Seller |

|

B – Paid by Broker |

|

|

|

|

A – APR Affected by Cost |

|

|

|

|

|

||||

|

S/ – Split by Seller & Others |

|

L – Paid by Lender |

|

|

|

|

O – Paid by Other |

|

P – Paid Outside Closing (POC) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Itemized Fee Worksheet ~ 02/2010 ~ Encompass360TM

| Fact Name | Description |

|---|---|

| Purpose | The Fee Worksheet is designed to provide an itemized estimate of charges associated with a loan settlement, helping borrowers understand potential costs. |

| Estimates | All fees listed on the worksheet are estimates. Actual charges may vary, meaning some fees could be higher or lower than those presented. |

| Provided By | This form is typically filled out by the lender or service provider involved in the loan process, ensuring transparency for the borrower. |

| Governing Laws | In the United States, the use of the Fee Worksheet is governed by the Real Estate Settlement Procedures Act (RESPA), which mandates clear disclosures of settlement costs. |

| Components | The worksheet includes various categories such as title charges, government recording fees, and additional settlement charges, providing a comprehensive view of costs. |

| Closing Costs Summary | A summary at the end of the worksheet consolidates all estimated costs, helping borrowers understand their total financial obligation at closing. |

Once you have gathered all the necessary information, you can begin filling out the Fee Worksheet form. This form will help you estimate the various costs associated with your loan transaction. Follow the steps below to ensure that you complete the form accurately.

What is the purpose of the Fee Worksheet form?

The Fee Worksheet form serves as a detailed estimate of the charges that may be incurred at the settlement of a loan. It provides a breakdown of various fees, including those related to title services, loan origination, and government recording. By using this form, borrowers can better understand the potential costs associated with their loan, helping them prepare financially for the closing process.

How are the fees listed on the Fee Worksheet determined?

The fees on the Fee Worksheet are estimates based on typical charges associated with the type of loan being processed. These estimates are influenced by various factors, including the lender's policies, the property's location, and the specific services required. It is important to note that actual charges may vary, and not all items listed may apply to every transaction.

What should I do if I see a fee on the worksheet that I do not understand?

If you encounter a fee on the Fee Worksheet that is unclear, it is advisable to reach out to your lender or service provider for clarification. They can provide detailed explanations about each fee and how it relates to your loan. Understanding these fees is crucial, as it allows you to make informed decisions regarding your loan and the overall transaction.

Can the estimated closing costs change after I receive the Fee Worksheet?

Yes, the estimated closing costs can change after you receive the Fee Worksheet. Since the fees listed are estimates, actual costs may be higher or lower at the time of closing. It is essential to keep open communication with your lender throughout the process to stay informed about any changes that may arise.

What are some common fees included in the Fee Worksheet?

The Fee Worksheet includes a variety of common fees, such as loan origination fees, title insurance, appraisal fees, and government recording fees. Additionally, it may list costs related to mortgage insurance, homeowner’s insurance, and property taxes. Each of these fees contributes to the overall cost of obtaining a loan and completing the transaction.

Is it possible to negotiate any of the fees listed on the Fee Worksheet?

In many cases, borrowers can negotiate certain fees listed on the Fee Worksheet. It may be possible to discuss loan origination fees, closing costs, or other charges with your lender or service provider. Open dialogue about these fees can lead to potential savings and a more favorable financial outcome for your loan.

Failing to include the date on the Fee Worksheet can lead to confusion about the timeline of the transaction.

Omitting the subject property information can result in miscommunication regarding the property being financed.

Not specifying the loan number can complicate the tracking of the loan throughout the process.

Incorrectly entering the interest rate may lead to inaccurate calculations of monthly payments.

Using incorrect fees for title charges, such as the settlement or closing fee, can cause discrepancies at closing.

Leaving out the total loan amount can prevent a complete understanding of the financial obligations.

Failing to list all estimated closing costs can lead to unexpected expenses for the borrower.

Not including the daily interest days can result in miscalculating the interest owed at closing.

Neglecting to fill in the initial deposit into the escrow account can affect the overall funding needed.

Forgetting to calculate total costs correctly can lead to confusion and disputes at the time of closing.

When preparing for a loan settlement, several documents are commonly used alongside the Fee Worksheet form. Each of these documents serves a specific purpose in ensuring a smooth transaction. Understanding their roles can help borrowers and service providers navigate the closing process more effectively.

Each of these documents plays a vital role in the loan settlement process. Ensuring that they are completed accurately and submitted on time can prevent delays and complications. Borrowers should be proactive in gathering these documents to facilitate a smooth closing experience.

The Good Faith Estimate (GFE) is a document that provides borrowers with a summary of the estimated costs associated with their mortgage. Like the Fee Worksheet, it outlines various charges, including loan origination fees, title insurance, and closing costs. The GFE helps borrowers understand the financial obligations they will face at closing, allowing them to compare offers from different lenders. This transparency aims to empower consumers to make informed decisions regarding their mortgage options.

The Loan Estimate (LE) is another key document that shares similarities with the Fee Worksheet. Issued after a borrower applies for a mortgage, the LE presents a detailed breakdown of loan terms, projected payments, and closing costs. It is designed to be clear and easy to understand, helping borrowers compare costs across different lenders. Both the LE and the Fee Worksheet emphasize transparency in the lending process, ensuring that borrowers are aware of their financial responsibilities.

The Closing Disclosure (CD) serves as a final statement of the actual costs associated with a mortgage transaction. Similar to the Fee Worksheet, the CD itemizes all fees and charges that the borrower will incur at closing. It is provided to borrowers three days before closing, allowing them to review the final costs and address any discrepancies. This document ensures that borrowers are fully informed of their financial commitments, promoting a smoother closing experience.

The HUD-1 Settlement Statement is a document used in real estate transactions that outlines the final costs of the sale. Like the Fee Worksheet, it details various fees, including title charges and closing costs. Although the HUD-1 has largely been replaced by the Closing Disclosure, it still serves as a useful reference for understanding how fees are calculated and allocated in a real estate transaction. Both documents aim to provide clarity and transparency to borrowers and sellers alike.

The Itemized List of Fees is often provided by lenders to give borrowers a clear view of all potential charges. This document is similar to the Fee Worksheet in that it breaks down costs into specific categories, such as processing fees and underwriting fees. By itemizing these fees, borrowers can better understand the costs associated with their loan and make informed decisions regarding their financing options.

The Estimated Closing Costs document is another important resource for borrowers. It outlines the anticipated expenses they will face when finalizing their mortgage. Like the Fee Worksheet, this document includes a variety of fees, such as appraisal fees and title insurance. Providing borrowers with a clear estimate of these costs helps them prepare financially for the closing process and avoid surprises on closing day.

The Pre-Closing Disclosure is a document that lenders may provide to borrowers before the final Closing Disclosure. It serves a similar purpose to the Fee Worksheet by summarizing the estimated costs associated with the mortgage. This document allows borrowers to review and confirm their understanding of the fees before the actual closing, ensuring they are fully prepared for their financial obligations. Both documents prioritize transparency and clarity in the lending process.

When filling out the Fee Worksheet form, follow these guidelines to ensure accuracy and compliance.

Following these steps will help streamline the process and avoid delays. Your diligence is key to a successful transaction.

Misconceptions about the Fee Worksheet form can lead to confusion during the loan process. Here are six common misunderstandings:

Here are some key takeaways about filling out and using the Fee Worksheet form: