The Fannie Mae 194 form, known as the Hardship Affidavit, plays a crucial role in the process of seeking foreclosure prevention alternatives. This form is designed for borrowers facing financial difficulties that hinder their ability to make mortgage payments. It requires essential borrower information, including names, dates of birth, and property details. The form prompts borrowers to identify specific hardships affecting their financial situation, such as reduced income, excessive debt, increased expenses, or insufficient cash reserves. Additionally, it includes an acknowledgment section where borrowers certify the truthfulness of their statements and agree to cooperate with their servicer's requirements. By submitting the Fannie Mae 194 form, borrowers take an important step toward exploring options that may help them avoid foreclosure. Understanding its components and implications is vital for anyone navigating this challenging process.

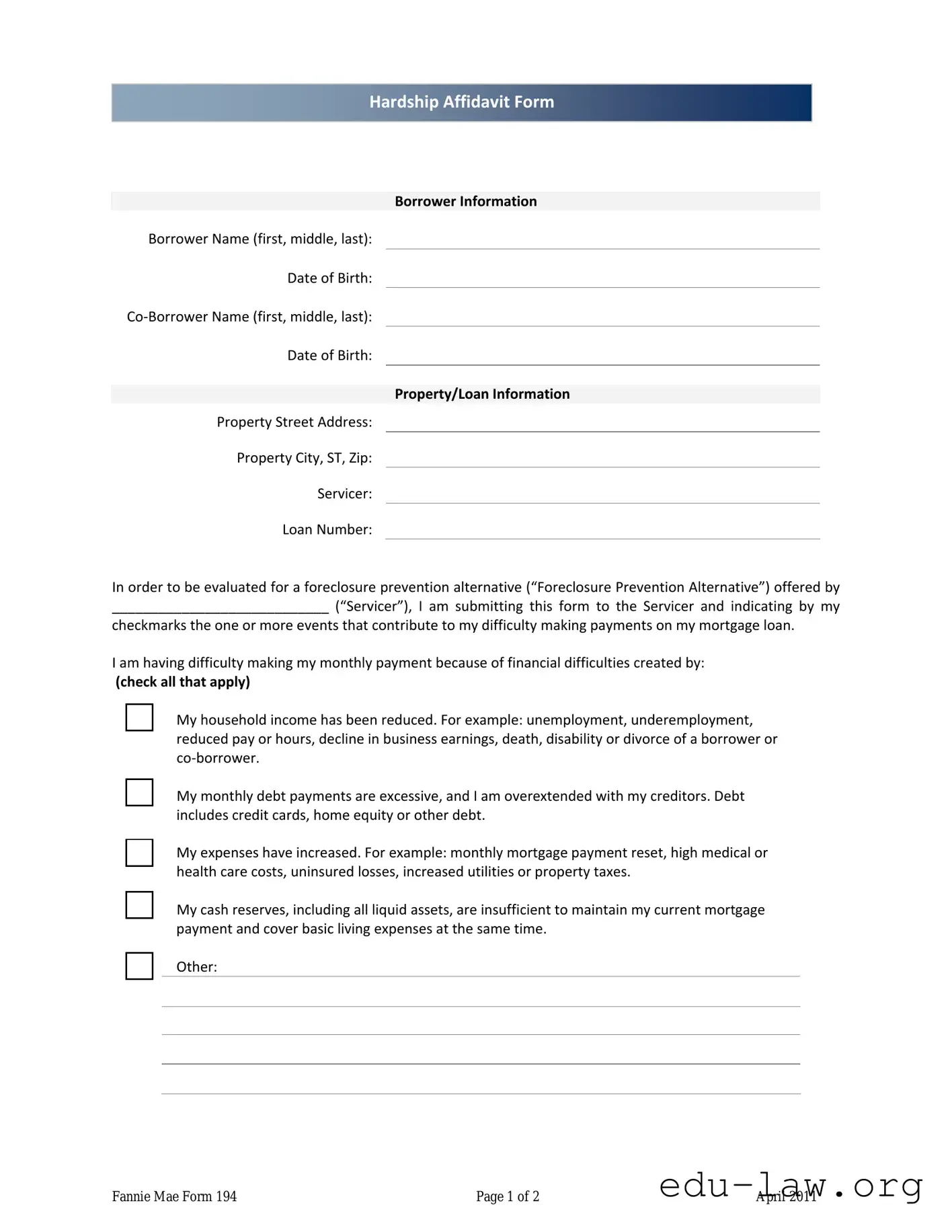

Hardship Affidavit Form

Borrower Information

Borrower Name (first, middle, last):

Date of Birth:

Co‐Borrower Name (first, middle, last):

Date of Birth:

Property/Loan Information

Property Street Address:

Property City, ST, Zip:

Servicer:

Loan Number:

In order to be evaluated for a foreclosure prevention alternative (“Foreclosure Prevention Alternative”) offered by

____________________________ (“Servicer”), I am submitting this form to the Servicer and indicating by my

checkmarks the one or more events that contribute to my difficulty making payments on my mortgage loan.

I am having difficulty making my monthly payment because of financial difficulties created by:

(check all that apply)

My household income has been reduced. For example: unemployment, underemployment, reduced pay or hours, decline in business earnings, death, disability or divorce of a borrower or co‐borrower.

My monthly debt payments are excessive, and I am overextended with my creditors. Debt includes credit cards, home equity or other debt.

My expenses have increased. For example: monthly mortgage payment reset, high medical or health care costs, uninsured losses, increased utilities or property taxes.

My cash reserves, including all liquid assets, are insufficient to maintain my current mortgage payment and cover basic living expenses at the same time.

Other:

Fannie Mae Form 194 |

Page 1 of 2 |

April 2011 |

Hardship Affidavit Form

Borrower/Co‐Borrower Acknowledgement and Agreement

1.I certify that all of the information in this Hardship Affidavit is truthful and the event(s) identified above has/have contributed to my need for a Foreclosure Prevention Alternative relating to my mortgage loan.

2.I understand and acknowledge the Servicer may investigate the accuracy of my statements, may require me to provide supporting documentation, and that knowingly submitting false information may violate Federal law.

3.I understand the Servicer may pull a current credit report on all borrowers obligated on the note relating to my mortgage loan.

4.I understand that if I have intentionally defaulted on my existing mortgage, engaged in fraud or misrepresented any fact(s) in connection with this Hardship Affidavit, or if I do not provide all of the required documentation, the Servicer may cancel a Foreclosure Prevention Alternative and may pursue foreclosure on my home.

5.I certify that I have not received a condemnation notice on my property.

6.I certify that I am willing to provide all requested documents and to respond to all Servicer communication in a timely manner. I understand that time is of the essence.

7.I understand that the Servicer may use this information to evaluate my eligibility for a Foreclosure Prevention Alternative, but the Servicer is not obligated to offer me assistance based solely on the representations in this Hardship Affidavit.

8.I understand that the Servicer may collect and record personal information, including, but not limited to, my name, address, telephone number, social security number, credit score, income, payment history, and information about account balances and activity. I understand and consent to the disclosure of my personal information and the terms of any Foreclosure Prevention Alternative offered by the Servicer to any investor, insurer, guarantor or servicer that owns, insures, guarantees or services my first lien or subordinate lien (if applicable) mortgage loan(s).

_________________________ ___________ |

_________________________ ____________ |

||

Borrower Signature |

Date |

Co‐Borrower Signature |

Date |

Fannie Mae Form 194 |

Page 2 of 2 |

April 2011 |

| Fact Name | Details |

|---|---|

| Purpose | The Fannie Mae 194 form is a Hardship Affidavit used to evaluate a borrower's eligibility for foreclosure prevention alternatives. |

| Borrower Information | The form collects essential borrower information, including names and dates of birth for both the borrower and co-borrower. |

| Property Information | Details about the property, such as the street address, city, state, and zip code, are required. |

| Servicer Role | The servicer is the entity that evaluates the submitted form and offers foreclosure prevention alternatives. |

| Financial Hardship | Borrowers must indicate specific events contributing to their financial difficulties, such as reduced income or increased expenses. |

| Certification | Borrowers certify the truthfulness of the information provided and acknowledge the servicer's right to verify it. |

| Credit Report | The servicer may pull a current credit report for all borrowers obligated on the mortgage note. |

| Consequences of Fraud | Submitting false information can lead to cancellation of any foreclosure prevention alternatives and potential foreclosure actions. |

| Required Documentation | Borrowers must be willing to provide all requested documentation in a timely manner to support their application. |

| Data Privacy | Personal information collected may be shared with investors, insurers, or servicers involved with the mortgage loan. |

Filling out the Fannie Mae 194 form is a critical step for homeowners seeking assistance with their mortgage payments. This form helps convey your financial situation to your loan servicer, allowing them to evaluate your eligibility for foreclosure prevention alternatives. Follow these steps carefully to ensure your information is accurate and complete.

After completing the form, ensure you keep a copy for your records. Submitting it to your servicer promptly can help facilitate a quicker response regarding potential assistance options. Stay proactive and maintain communication with your servicer as you navigate this process.

What is the Fannie Mae 194 form?

The Fannie Mae 194 form, also known as the Hardship Affidavit, is a document used by borrowers experiencing financial difficulties to communicate their situation to their mortgage servicer. It helps the servicer evaluate the borrower's eligibility for foreclosure prevention alternatives.

Who should fill out the Fannie Mae 194 form?

Both borrowers and co-borrowers facing challenges in making mortgage payments should complete the form. It is essential for anyone involved in the mortgage to provide accurate information regarding their financial hardships.

What information is required on the form?

The form requires personal information such as the names and dates of birth of the borrower and co-borrower. Additionally, it asks for property details, loan number, and a checklist of financial difficulties contributing to the inability to make payments.

What types of financial difficulties can I report?

You can indicate various hardships, such as a reduction in household income, excessive monthly debt payments, increased expenses, or insufficient cash reserves. There is also an option to specify other hardships not listed.

What happens after I submit the Fannie Mae 194 form?

After submission, the servicer will review the information provided. They may reach out for additional documentation and will assess your eligibility for a foreclosure prevention alternative. However, submitting the form does not guarantee assistance.

What are the consequences of providing false information?

Providing false information on the form can lead to serious consequences, including the cancellation of any foreclosure prevention alternatives and potential foreclosure proceedings. It is crucial to be truthful and accurate when filling out the form.

How can I ensure my application is processed quickly?

To facilitate a swift review, respond promptly to any requests from the servicer for additional documentation or information. Timeliness is important in these situations, so maintaining open communication is key.

Is my personal information secure when I submit this form?

Yes, the servicer is required to handle your personal information with care. They may share your information with relevant parties involved in your mortgage, but this is done to evaluate your eligibility for assistance and ensure compliance with regulations.

Incomplete Personal Information: Many people forget to fill out all required fields, such as the full names and dates of birth for both the borrower and co-borrower. Missing this information can delay the process.

Failure to Specify Hardship: Some individuals do not check any of the boxes indicating their specific financial difficulties. It's crucial to clearly identify the reasons for payment difficulties to ensure proper evaluation.

Not Providing Supporting Documentation: People often neglect to include necessary documents that support their claims. This oversight can lead to delays or denials of assistance.

Ignoring Signature Requirements: Skipping signatures or forgetting to date the form is a common mistake. Both the borrower and co-borrower must sign and date the affidavit for it to be valid.

Misunderstanding the Consequences: Some individuals do not fully grasp the implications of submitting false information. Misrepresentation can lead to serious legal issues, including foreclosure.

When dealing with mortgage difficulties, several forms and documents may accompany the Fannie Mae 194 form. Each document serves a specific purpose in the process of seeking assistance for foreclosure prevention. Below are some of the key documents that are often used alongside the Fannie Mae 194 form.

Having these documents ready can streamline the process of seeking help with your mortgage. Each one plays a crucial role in demonstrating your financial situation and your need for a foreclosure prevention alternative. Be prepared to provide accurate and complete information to improve your chances of receiving assistance.

The Fannie Mae Form 194 is similar to the Hardship Declaration Form used by various lenders. This document allows borrowers to outline their financial difficulties and request assistance. Like the Fannie Mae 194 form, it typically requires borrowers to specify the events that led to their financial struggles, such as job loss or increased expenses. Both forms aim to collect essential information that can help the lender evaluate the borrower's situation and explore options for foreclosure prevention.

Another comparable document is the Mortgage Assistance Application. This form is often used by homeowners seeking relief from their mortgage payments. Similar to the Fannie Mae 194, it gathers information about the borrower's financial status and hardship circumstances. The Mortgage Assistance Application also emphasizes the importance of providing accurate information and may require supporting documentation to substantiate the claims made by the borrower.

The Uniform Borrower Assistance Form is another document that serves a similar purpose. It is designed to assist borrowers in communicating their financial difficulties to lenders. Like the Fannie Mae 194 form, it includes sections for borrowers to describe their hardships and the reasons behind their inability to make payments. The Uniform Borrower Assistance Form also facilitates a streamlined process for lenders to assess the borrower's eligibility for various assistance programs.

The Loan Modification Request Form is also relevant in this context. Borrowers use this form to formally request changes to their mortgage terms due to financial hardship. Similar to the Fannie Mae 194, it requires detailed information about the borrower's current financial situation and the specific hardships faced. Both forms aim to initiate a conversation between the borrower and lender regarding potential modifications that could alleviate the financial burden.

Additionally, the Forbearance Agreement is a document that shares similarities with the Fannie Mae 194 form. This agreement allows borrowers to temporarily reduce or suspend their mortgage payments due to financial hardship. Like the Fannie Mae 194, it requires the borrower to explain their circumstances and often necessitates supporting documentation. Both documents serve as critical tools in negotiating temporary relief from mortgage obligations.

The Financial Hardship Form is another document that aligns with the Fannie Mae 194 form's purpose. This form collects information about a borrower’s financial difficulties and is used to assess eligibility for various relief options. Similar to the Fannie Mae 194, it asks borrowers to detail the events that have led to their financial struggles, ensuring that lenders have a comprehensive understanding of the situation before making decisions regarding assistance.

The Loss Mitigation Application is also comparable to the Fannie Mae 194 form. This application is utilized by borrowers to seek various loss mitigation options, including loan modifications and repayment plans. Like the Fannie Mae 194, it requires borrowers to provide detailed information about their financial hardships and may necessitate supporting documentation to support their claims. Both documents aim to facilitate a process that helps borrowers avoid foreclosure.

Finally, the Borrower Information Form is similar in that it collects essential personal and financial details from the borrower. While it may not focus specifically on hardship, it often accompanies other forms like the Fannie Mae 194 to provide a complete picture of the borrower’s financial status. Both forms are critical in the assessment process, as they help lenders understand the borrower's overall situation and the potential need for assistance.

When filling out the Fannie Mae 194 form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are five things to do and five things to avoid:

Misconceptions about the Fannie Mae 194 form can lead to confusion and misunderstandings. Here are six common misconceptions, along with clarifications:

Understanding these misconceptions can help borrowers navigate the process more effectively. Clarity can lead to better decisions regarding mortgage assistance.

When filling out and utilizing the Fannie Mae 194 form, there are several important considerations to keep in mind. This form serves as a hardship affidavit, allowing borrowers to communicate their financial difficulties to their mortgage servicer. Here are four key takeaways: