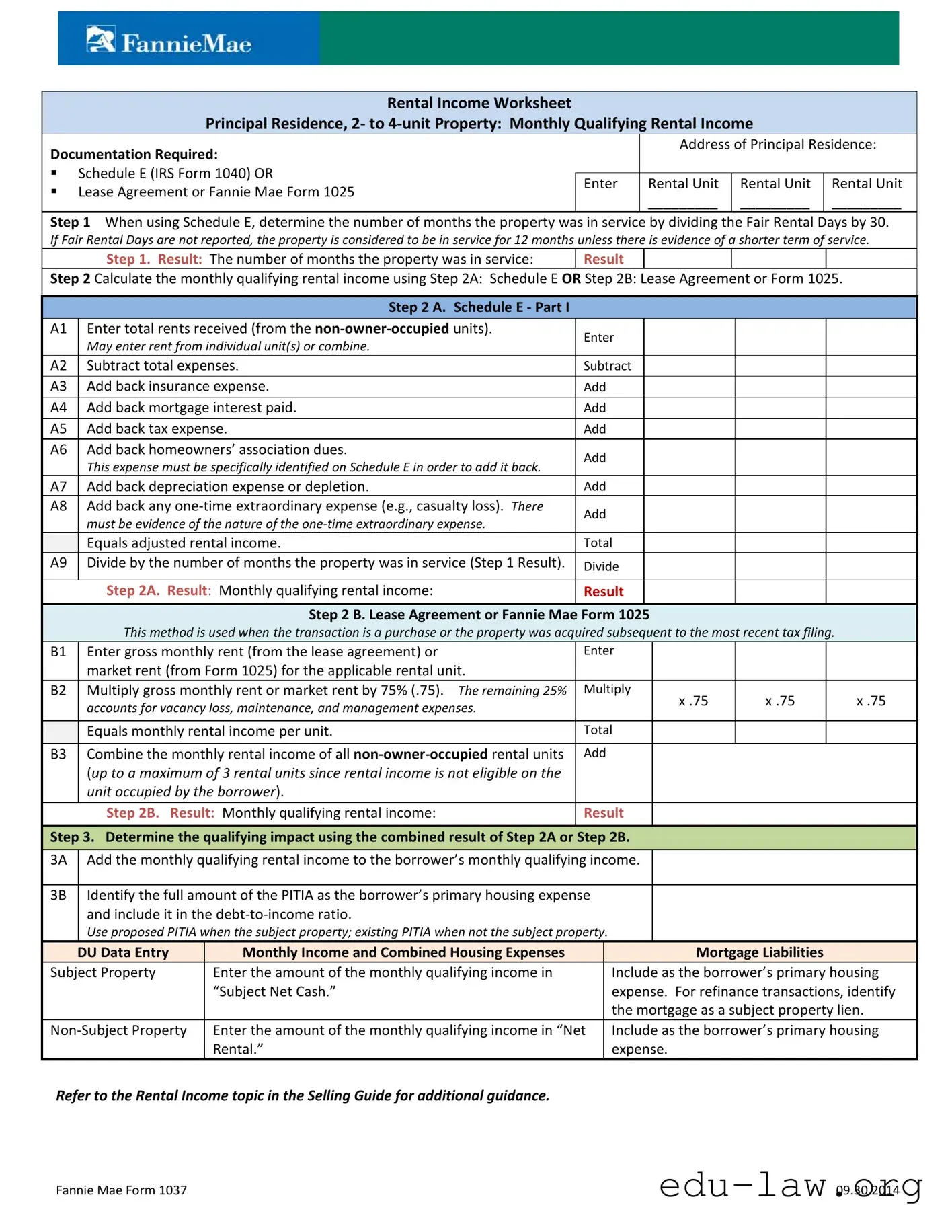

The Fannie Mae 1037 form serves as a crucial tool for documenting rental income associated with a principal residence or a 2- to 4-unit property. This form is essential for borrowers looking to qualify for a mortgage based on rental income. It outlines the necessary documentation required, which includes either Schedule E from IRS Form 1040 or a lease agreement, along with the Fannie Mae Form 1025. The process begins with determining how long the property has been in service, which can be calculated by dividing the Fair Rental Days by 30. If Fair Rental Days are unavailable, the property is assumed to have been in service for a full year, barring evidence to the contrary. Following this, the form provides detailed steps for calculating the monthly qualifying rental income, either through an analysis of the Schedule E or by utilizing a lease agreement. Each method requires specific calculations, such as adjusting total rents received by subtracting expenses and adding back certain costs like insurance, mortgage interest, and taxes. Ultimately, the Fannie Mae 1037 form not only assists in determining the qualifying rental income but also integrates this figure into the borrower’s overall financial assessment, impacting their debt-to-income ratio and qualifying income for mortgage applications.

Rental Income Worksheet

Principal Residence, 2- to

Documentation Required: |

|

Address of Principal Residence: |

||||

|

|

|

|

|||

Schedule E (IRS Form 1040) OR |

|

|

|

|

||

Enter |

Rental Unit |

Rental Unit |

Rental Unit |

|||

|

Lease Agreement or Fannie Mae Form 1025 |

|||||

|

_________ |

_________ |

_________ |

|||

|

|

|

||||

Step 1 When using Schedule E, determine the number of months the property was in service by dividing the Fair Rental Days by 30. If Fair Rental Days are not reported, the property is considered to be in service for 12 months unless there is evidence of a shorter term of service.

Step 1. Result: The number of months the property was in service: |

Result |

|

|

|

Step 2 Calculate the monthly qualifying rental income using Step 2A: Schedule E OR Step 2B: Lease Agreement or Form 1025.

|

|

|

Step 2 A. Schedule E - Part I |

|

|

|

|

|

|

|

|

A1 |

Enter total rents received (from the |

Enter |

|

|

|

|

|

|

|

|

May enter rent from individual unit(s) or combine. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2 |

Subtract total expenses. |

Subtract |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A3 |

Add back insurance expense. |

Add |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A4 |

Add back mortgage interest paid. |

Add |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A5 |

Add back tax expense. |

Add |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A6 |

Add back homeowners’ association dues. |

Add |

|

|

|

|

|

|

|

|

This expense must be specifically identified on Schedule E in order to add it back. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A7 |

Add back depreciation expense or depletion. |

Add |

|

|

|

|

|

|

|

A8 |

Add back any |

Add |

|

|

|

|

|

|

|

|

must be evidence of the nature of the |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equals adjusted rental income. |

Total |

|

|

|

|

|

|

|

A9 |

Divide by the number of months the property was in service (Step 1 Result). |

Divide |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 2A. Result: Monthly qualifying rental income: |

Result |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 2 B. Lease Agreement or Fannie Mae Form 1025 |

|

|

|

|

||

|

|

|

This method is used when the transaction is a purchase or the property was acquired subsequent to the most recent tax filing. |

|

|

||||

|

|

B1 |

Enter gross monthly rent (from the lease agreement) or |

Enter |

|

|

|

|

|

|

|

|

market rent (from Form 1025) for the applicable rental unit. |

|

|

|

|

|

|

|

|

B2 |

Multiply gross monthly rent or market rent by 75% (.75). The remaining 25% |

Multiply |

x .75 |

|

x .75 |

|

|

|

|

|

accounts for vacancy loss, maintenance, and management expenses. |

|

x .75 |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equals monthly rental income per unit. |

Total |

|

|

|

|

|

|

|

B3 |

Combine the monthly rental income of all |

Add |

|

|

|

|

|

|

|

|

(up to a maximum of 3 rental units since rental income is not eligible on the |

|

|

|

|

|

|

|

|

|

unit occupied by the borrower). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Step 2B. Result: Monthly qualifying rental income: |

Result |

|

|

|

|

|

Step 3. Determine the qualifying impact using the combined result of Step 2A or Step 2B.

3A Add the monthly qualifying rental income to the borrower’s monthly qualifying income.

3B Identify the full amount of the PITIA as the borrower’s primary housing expense and include it in the

Use proposed PITIA when the subject property; existing PITIA when not the subject property.

|

|

DU Data Entry |

Monthly Income and Combined Housing Expenses |

|

Mortgage Liabilities |

|

|

|

|

|

|||

|

|

Subject Property |

Enter the amount of the monthly qualifying income in |

|

Include as the borrower’s primary housing |

|

|

|

|

“Subject Net Cash.” |

|

expense. For refinance transactions, identify |

|

|

|

|

|

|

the mortgage as a subject property lien. |

|

|

|

|

|

|

|

|

|

|

Enter the amount of the monthly qualifying income in “Net |

|

Include as the borrower’s primary housing |

|

|

|

|

|

Rental.” |

|

expense. |

|

Refer to the Rental Income topic in the Selling Guide for additional guidance.

Fannie Mae Form 1037 |

09.30.2014 |

| Fact Name | Description |

|---|---|

| Form Purpose | The Fannie Mae 1037 form is a Rental Income Worksheet used to calculate monthly qualifying rental income for properties with 2 to 4 units. |

| Documentation Required | Users must provide either Schedule E (IRS Form 1040) or a Lease Agreement, along with Fannie Mae Form 1025 if applicable. |

| Service Duration Calculation | To determine how long the property was in service, divide the Fair Rental Days by 30. If no Fair Rental Days are reported, assume the property was in service for 12 months. |

| Monthly Income Calculation - Schedule E | Using Schedule E, calculate the adjusted rental income by accounting for total rents, expenses, and allowable add-backs, then divide by the number of months in service. |

| Monthly Income Calculation - Lease Agreement | When using a Lease Agreement or Form 1025, enter the gross monthly rent and multiply by 75% to account for vacancy and maintenance costs. |

| Qualifying Impact | The monthly qualifying rental income is added to the borrower’s monthly qualifying income to assess the overall financial impact. |

| PITIA Inclusion | The full amount of the PITIA (Principal, Interest, Taxes, Insurance, and Association dues) must be included in the debt-to-income ratio for qualifying purposes. |

| State-Specific Forms | While the Fannie Mae 1037 form is standardized, states may have specific requirements or additional forms governed by their respective real estate laws. |

Completing the Fannie Mae 1037 form involves several key steps to accurately report rental income. This process is essential for determining qualifying rental income for a principal residence with 2 to 4 units. Follow these steps carefully to ensure all necessary information is included.

What is the Fannie Mae 1037 form used for?

The Fannie Mae 1037 form is a Rental Income Worksheet specifically designed for principal residences that are 2- to 4-unit properties. It helps lenders assess the monthly qualifying rental income generated from these properties. By accurately documenting rental income, the form aids in determining a borrower’s financial eligibility for a mortgage.

What documentation is required to complete the Fannie Mae 1037 form?

To complete the Fannie Mae 1037 form, you will need either Schedule E from IRS Form 1040 or a lease agreement. If using Schedule E, ensure it reflects the total rents received from non-owner-occupied units. Alternatively, if you are using a lease agreement or Fannie Mae Form 1025, this information will also be necessary to calculate the rental income.

How do I calculate the number of months the property was in service?

To determine how many months the property was in service, divide the Fair Rental Days reported on Schedule E by 30. If Fair Rental Days are not provided, the property will be considered in service for 12 months, unless there is evidence to suggest a shorter period. This step is essential for accurate income calculations.

What steps are involved in calculating monthly qualifying rental income?

There are two main methods for calculating monthly qualifying rental income. The first method involves using Schedule E, where you will adjust the total rents received by subtracting total expenses and adding back specific costs such as insurance, mortgage interest, and homeowners’ association dues. The second method uses either a lease agreement or Form 1025, where you take the gross monthly rent and multiply it by 75% to account for vacancy and maintenance costs. The resulting amounts from both methods will help determine the monthly qualifying rental income.

What is the significance of the PITIA in the rental income calculation?

PITIA stands for Principal, Interest, Taxes, Insurance, and Association dues. It represents the total monthly housing expense for the borrower. When calculating the qualifying impact of rental income, the monthly qualifying rental income is added to the borrower’s qualifying income, and the full amount of PITIA is included in the debt-to-income ratio. This helps lenders assess the borrower’s overall financial health.

Can I include rental income from all units in a multi-unit property?

Yes, you can include rental income from all non-owner-occupied units in a multi-unit property. However, keep in mind that rental income is not eligible from the unit occupied by the borrower. The Fannie Mae 1037 form allows for a maximum of three rental units to be considered when calculating the qualifying rental income.

Where can I find additional guidance on rental income documentation?

For more detailed guidance on rental income documentation and calculations, you can refer to the Rental Income topic in the Fannie Mae Selling Guide. This resource provides comprehensive information to ensure compliance with Fannie Mae's requirements and to facilitate the mortgage process.

Not providing the correct address of the principal residence. Ensure the address matches official records to avoid confusion.

Failing to include all required documentation. Either Schedule E or a lease agreement is necessary for proper evaluation.

Miscalculating the number of months the property was in service. Use Fair Rental Days correctly or assume a 12-month period only when appropriate.

Omitting total rents received from non-owner-occupied units. Ensure all income sources are accurately reported.

Incorrectly subtracting total expenses from the rental income. Double-check calculations to ensure accuracy.

Not adding back specific expenses, such as insurance or mortgage interest, that are eligible for inclusion. Review Schedule E guidelines carefully.

Ignoring the need for evidence of one-time extraordinary expenses. Document all claims to support your entries.

Using gross monthly rent without applying the 75% rule for vacancy and maintenance. Remember to adjust for these factors.

Combining rental income from more than three units. Only include income from up to three non-owner-occupied units.

Not accurately reflecting the PITIA in the debt-to-income ratio. Use the correct figures based on whether the property is subject or non-subject.

The Fannie Mae 1037 form is a critical document used for calculating rental income from a principal residence, particularly for properties with 2 to 4 units. To ensure a comprehensive understanding of the rental income, several other forms and documents are often utilized alongside the 1037 form. Below is a list of these documents, each serving a unique purpose in the rental income assessment process.

Understanding these documents can help streamline the rental income verification process. Each form plays a vital role in ensuring that the rental income reported is accurate and reliable. Proper documentation can facilitate smoother transactions and contribute to informed decision-making.

The Fannie Mae 1037 form is similar to the IRS Schedule E, which is used by taxpayers to report rental income and expenses. Both documents require the reporting of total rents received and allow for the deduction of various expenses related to rental properties. Schedule E provides a detailed breakdown of income and expenses, enabling property owners to calculate their net rental income. This net income is then used to assess the financial viability of a rental property, similar to how the 1037 form calculates qualifying rental income for mortgage purposes.

Another document similar to the Fannie Mae 1037 form is the Lease Agreement. This legal contract outlines the terms under which a tenant rents a property from a landlord. Like the 1037 form, it specifies the rental amount and duration of the lease, which are essential for determining rental income. The lease agreement provides concrete evidence of rental terms, which can be used to verify income when filling out the 1037 form, especially when assessing monthly qualifying rental income based on the lease terms.

The Fannie Mae Form 1025 is also comparable to the 1037 form. This form is specifically designed to evaluate the market rent of a property that is not owner-occupied. Both documents focus on determining rental income but approach it from different angles. While the 1037 form allows for adjustments based on actual expenses, the Form 1025 provides a standardized method to assess market rent, which can be crucial for qualifying income calculations.

The HUD-1 Settlement Statement shares similarities with the Fannie Mae 1037 form in that it provides a comprehensive overview of financial transactions related to a property. While the HUD-1 is primarily used for closing costs and settlement details, it also includes information on rental income if applicable. This can help lenders understand the financial context of a property, much like how the 1037 form assesses rental income for mortgage qualification.

The Cash Flow Statement is another document that parallels the Fannie Mae 1037 form. This financial statement summarizes the cash inflows and outflows of a property, including rental income. Both documents aim to provide a clear picture of a property's financial performance. The Cash Flow Statement offers a broader view of financial health, while the 1037 focuses specifically on qualifying rental income for mortgage purposes.

Additionally, the Profit and Loss Statement (P&L) is similar to the Fannie Mae 1037 form as it outlines income and expenses for a specific period. Both documents are used to assess financial performance. The P&L provides a detailed account of all income sources and expenses, allowing property owners to evaluate profitability. This information can be crucial when determining qualifying rental income on the 1037 form.

Lastly, the Bank Statements can be considered similar to the Fannie Mae 1037 form in that they provide evidence of rental income. Lenders often review bank statements to verify deposits related to rental payments. This information supports the calculations made on the 1037 form regarding qualifying rental income. Both documents aim to establish a clear financial picture, ensuring that the rental income reported is accurate and reliable.

When filling out the Fannie Mae 1037 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below is a list of things to do and avoid.

Misconception 1: The Fannie Mae 1037 form is only for single-family homes.

This form is applicable to 2- to 4-unit properties as well. It is designed to assess rental income from these types of properties, not just single-family residences.

Misconception 2: You cannot use both Schedule E and a lease agreement.

In fact, the form allows for both methods. Borrowers can choose to calculate rental income using either Schedule E or a lease agreement, depending on their specific situation.

Misconception 3: The number of months a property has been in service is always 12.

This is not true. If Fair Rental Days are not reported, the property is considered to be in service for 12 months only if there is no evidence suggesting a shorter term. If there is evidence, the months in service may be less than 12.

Misconception 4: All expenses can be deducted without documentation.

Documentation is crucial. Certain expenses, such as homeowners’ association dues, must be specifically identified on Schedule E in order to be added back to the rental income.

Misconception 5: Rental income is always fully counted in debt-to-income calculations.

Only a portion of the rental income is considered. For instance, when using a lease agreement, only 75% of the gross monthly rent is counted to account for vacancy loss and other expenses.

Understanding the Fannie Mae 1037 form is crucial for accurately documenting rental income for a principal residence. Here are key takeaways to help you navigate the process:

Using the Fannie Mae 1037 form correctly can significantly impact your loan application process. Ensure all calculations are accurate and supported by proper documentation to facilitate a smoother experience.