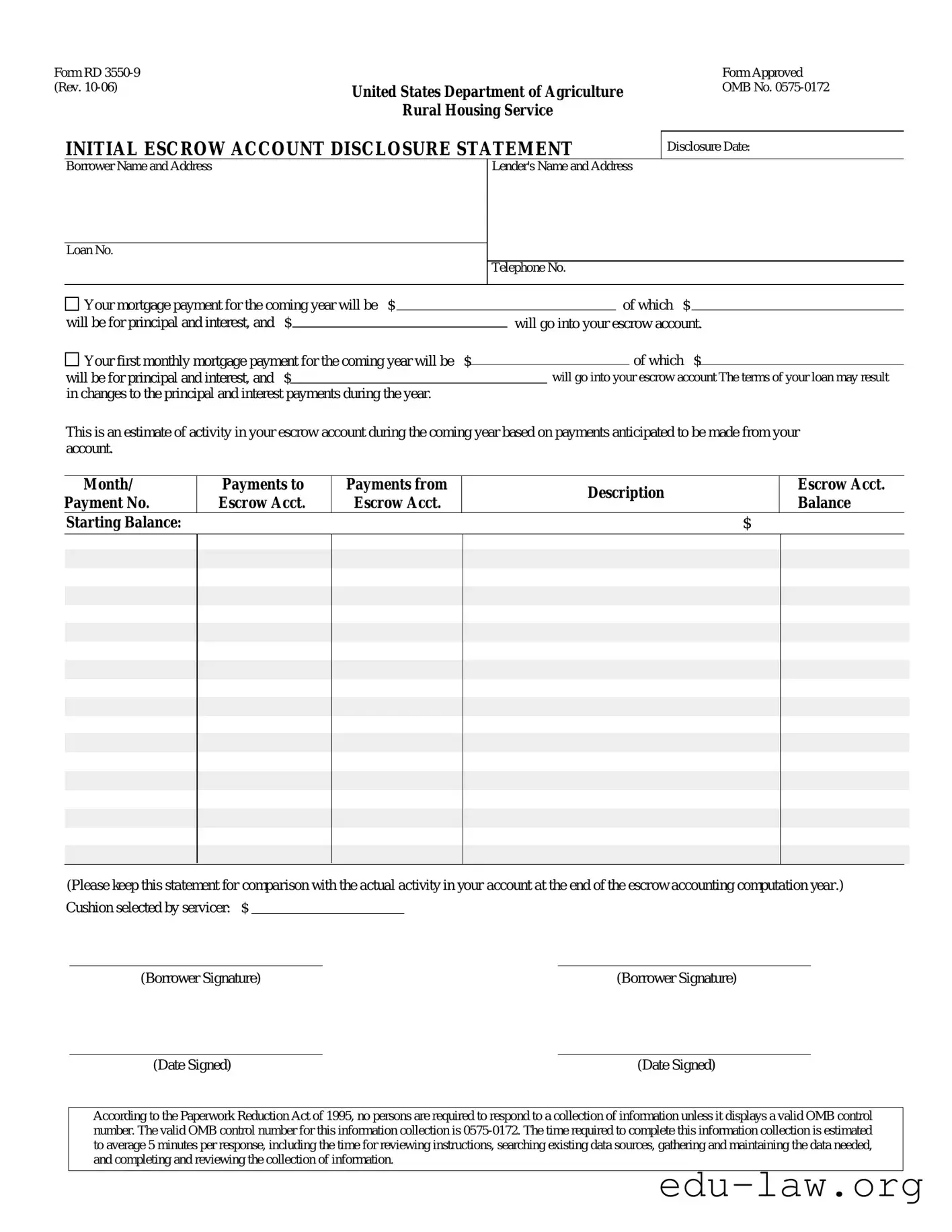

The Escrow Disclosure form, specifically Form RD 3550-9, plays a crucial role in the home financing process for borrowers. This document outlines important financial details related to the escrow account associated with a mortgage loan. It provides a clear breakdown of the anticipated monthly mortgage payment, including how much will go toward principal and interest and how much will be allocated to the escrow account. The form also highlights potential changes in principal and interest payments throughout the year, ensuring borrowers are well-informed about their financial obligations. Additionally, it estimates the activity in the escrow account, detailing expected payments into and out of the account on a monthly basis. The starting balance of the escrow account is noted, along with a cushion selected by the servicer to account for fluctuations in expenses. Borrowers are advised to keep this statement for future reference, allowing them to compare it with the actual activity in their account at the end of the escrow accounting computation year. Overall, the Escrow Disclosure form serves as a vital tool for transparency and financial planning in the mortgage process.

Form RD

(Rev.

Rural Housing Service

INITIAL ESCROW ACCOUNT DISCLOSURE STATEMENT

Form Approved

OMB No.

Disclosure Date:

Borrower Name and Address

Lender's Name and Address

Loan No.

Telephone No.

Your mortgage payment for the coming year will be $ |

|

|

|

of which $ |

|

|

||||

will be for principal and interest, and |

$ |

|

|

will go into your escrow account. |

||||||

|

|

|||||||||

Your first monthly mortgage payment for the coming year will be $ |

|

|

|

of which $ |

|

|||||

|

|

|

|

|

|

|||||

will be for principal and interest, and |

$ |

|

|

|

|

will go into your escrow account The terms of your loan may result |

||||

in changes to the principal and interest payments during the year. |

|

|

|

|

|

|

||||

This is an estimate of activity in your escrow account during the coming year based on payments anticipated to be made from your account.

Month/ |

Payments to |

Payments from |

Description |

|

Escrow Acct. |

|

Payment No. |

Escrow Acct. |

Escrow Acct. |

|

Balance |

||

|

|

|||||

Starting Balance: |

|

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Please keep this statement for comparison with the actual activity in your account at the end of the escrow accounting computation year.)

Cushion selected by servicer: $

(Borrower Signature)

(Date Signed)

(Borrower Signature)

(Date Signed)

According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a valid OMB control number. The valid OMB control number for this information collection is

| Fact Name | Details |

|---|---|

| Form Identifier | This is known as Form RD 3550-9 (Rev. 10-06). |

| Governing Body | The form is issued by the United States Department of Agriculture Rural Housing Service. |

| Disclosure Date | The form includes a section for the disclosure date, which must be filled out by the lender. |

| OMB Approval | The form has been approved by the Office of Management and Budget under control number 0575-0172. |

| Escrow Account Purpose | Funds in the escrow account are used for property taxes, insurance, and other related costs. |

| Initial Payment Breakdown | It details the breakdown of the first monthly mortgage payment, including principal, interest, and escrow contributions. |

| Annual Estimate | The form provides an estimate of escrow account activity for the upcoming year. |

| Borrower Signature | Borrowers must sign and date the form to acknowledge receipt and understanding of the escrow disclosure. |

Completing the Escrow Disclosure form is an important step in understanding your mortgage payments and how your escrow account will be managed. This form outlines the estimated activity in your escrow account for the coming year. Follow the steps below to fill out the form accurately.

Once completed, keep this form for your records. It will help you compare the estimated activity with the actual activity in your escrow account at the end of the accounting year.

What is the purpose of the Escrow Disclosure form?

The Escrow Disclosure form serves to inform borrowers about the details of their escrow account related to their mortgage. It outlines how much of the monthly mortgage payment will be allocated to principal, interest, and escrow. This transparency helps borrowers understand their financial obligations and anticipate future payments, ensuring they are prepared for any changes that may occur throughout the year.

What information is included in the Escrow Disclosure form?

The form includes several key pieces of information. It lists the borrower's name and address, the lender's name and address, and the loan number. Additionally, it details the total monthly mortgage payment, the breakdown of that payment into principal, interest, and escrow contributions. The form also provides an estimate of the escrow account's activity for the coming year, including anticipated payments into and out of the account, and the starting balance. Lastly, it mentions any cushion selected by the servicer, which is an extra amount held in the account to cover potential fluctuations in expenses.

How does the escrow account work?

An escrow account is a financial arrangement where funds are held by a third party on behalf of the borrower and lender. In the context of a mortgage, the borrower pays a portion of their monthly payment into the escrow account. These funds are then used to pay property taxes, homeowners insurance, and sometimes other related expenses. This system helps ensure that these important bills are paid on time, preventing potential penalties or lapses in coverage.

Why might my escrow payments change over time?

Escrow payments can fluctuate due to changes in property taxes, homeowners insurance premiums, or other costs covered by the escrow account. For instance, if your local government raises property taxes, your escrow payment may increase to accommodate the higher tax bill. The lender will periodically review the escrow account to ensure there are sufficient funds to cover these expenses and may adjust the monthly payment accordingly.

What should I do if I have questions about my escrow account?

If you have questions or concerns about your escrow account, it is important to reach out to your lender or loan servicer. They can provide specific information regarding your account, explain any changes in payments, and assist with any discrepancies you may notice. Keeping open lines of communication with your lender can help ensure that you stay informed about your financial obligations.

Is there a specific time frame for reviewing the escrow account?

Typically, lenders review escrow accounts annually. During this review, they assess the account's balance and the anticipated payments for the upcoming year. This is when any necessary adjustments to your monthly escrow payment will be made. It is advisable to keep the Escrow Disclosure form for comparison with the actual activity in your account at the end of the escrow accounting computation year. This will help you understand any discrepancies and address them with your lender.

Missing Information: One of the most common mistakes is failing to provide all required information. This includes the borrower's name, address, and loan number. Ensure every section is filled out completely.

Incorrect Payment Amounts: Entering the wrong amounts for principal, interest, or escrow contributions can lead to confusion. Double-check these figures to avoid discrepancies later.

Neglecting to Review Changes: The terms of the loan may change throughout the year. Failing to account for potential fluctuations in payments can impact your budgeting.

Ignoring the Cushion: The cushion amount selected by the servicer is crucial for maintaining the escrow account. Not understanding or disregarding this cushion can lead to insufficient funds when payments are due.

Not Keeping a Copy: After filling out the form, some forget to keep a copy for personal records. Retaining this document is essential for tracking your escrow account's activity over time.

Overlooking Signatures: Missing signatures can delay the processing of your escrow account. Ensure that all required signatures are provided and dated appropriately.

The Escrow Disclosure form is an essential document in the mortgage process, providing borrowers with a detailed overview of their escrow account. Several other forms and documents are commonly used alongside this disclosure to ensure a comprehensive understanding of the mortgage terms and obligations. Below is a list of these related documents.

Understanding these documents is crucial for borrowers as they navigate the mortgage process. Each form plays a significant role in ensuring transparency and protecting the rights of all parties involved.

The Good Faith Estimate (GFE) is a document that outlines the estimated costs associated with a mortgage loan. Similar to the Escrow Disclosure form, it provides borrowers with a clear understanding of their financial obligations. The GFE includes details about loan terms, interest rates, and other fees, allowing borrowers to compare different loan offers. Both documents aim to enhance transparency in the borrowing process, helping borrowers make informed decisions.

The Loan Estimate (LE) serves a similar purpose to the Escrow Disclosure form by providing borrowers with a breakdown of loan costs. It includes information on monthly payments, interest rates, and estimated closing costs. Like the Escrow Disclosure, the LE is designed to give borrowers a comprehensive view of their financial commitments. This document must be provided within three days of applying for a loan, ensuring that borrowers have timely access to critical information.

The Closing Disclosure (CD) is another important document that shares similarities with the Escrow Disclosure form. It details the final terms of the loan, including the actual costs of closing. Both documents aim to provide clarity and ensure that borrowers understand their financial responsibilities. The CD is provided to borrowers three days before closing, allowing them to review and confirm the accuracy of their loan terms and costs.

The Annual Escrow Account Disclosure is a document that summarizes the activity in an escrow account over the previous year. This document is similar to the Escrow Disclosure form as it provides a detailed account of payments made into and out of the escrow account. Borrowers can use this information to verify that their escrow account is being managed correctly and to anticipate future payments. It reinforces the importance of transparency in managing escrow funds.

The Mortgage Servicing Disclosure Statement outlines the lender's policies regarding the servicing of the loan. This document is akin to the Escrow Disclosure form in that it informs borrowers about how their loan will be managed. It includes information about potential changes in loan servicing and provides reassurance to borrowers about the handling of their mortgage. Both documents emphasize the importance of clear communication between borrowers and lenders.

The Property Insurance Disclosure is a document that informs borrowers about the insurance requirements for their property. Similar to the Escrow Disclosure form, it outlines the costs associated with maintaining adequate insurance coverage. This document ensures that borrowers understand their responsibilities regarding property insurance and how it relates to their escrow account. It plays a crucial role in protecting both the borrower and the lender's investment.

The Homeowners Association (HOA) Disclosure is another document that may be similar to the Escrow Disclosure form. It provides information about any fees or assessments associated with living in a community governed by an HOA. Like the Escrow Disclosure, it outlines financial obligations that borrowers need to be aware of. Understanding these fees is essential for borrowers to accurately budget their monthly payments and avoid surprises down the road.

When filling out the Escrow Disclosure form, there are important practices to keep in mind. Here’s a list of what you should and shouldn’t do:

There are several misconceptions about the Escrow Disclosure form that can lead to confusion for borrowers. Understanding these can help clarify the purpose and function of this important document.

This form is relevant for any borrower who has an escrow account, regardless of whether they are purchasing their first home or refinancing an existing mortgage.

The figures provided are estimates based on anticipated payments. They may vary throughout the year due to changes in property taxes or insurance costs.

In many cases, lenders require an escrow account as part of the mortgage agreement to ensure that property taxes and insurance are paid on time.

While the lender manages the account, borrowers can inquire about the balance and request adjustments if necessary.

This form provides critical information about how the escrow account will function, helping borrowers to budget for their total mortgage payment.

Different lenders may have variations in their forms and disclosures, but they all serve the same fundamental purpose of informing borrowers about their escrow accounts.

Understanding the Escrow Disclosure form is crucial for any borrower. Here are some key takeaways to keep in mind when filling out and using this important document:

By paying attention to these key points, you can navigate the escrow process with greater confidence and clarity.