Understanding your credit report is essential for maintaining financial health, and when inaccuracies arise, the Credit Report Dispute form serves as a critical tool for consumers. This form allows individuals to formally challenge errors or misleading information found in their credit reports, which can significantly impact credit scores and borrowing capabilities. It typically requires personal identification details, a description of the disputed information, and supporting documentation to substantiate the claim. By submitting this form, consumers initiate a process that compels credit reporting agencies to investigate the discrepancies. Timeliness is crucial, as there are specific deadlines for submitting disputes, and the outcome can influence future financial opportunities. Knowing how to effectively utilize this form can empower individuals to take control of their credit histories and ensure that their reports accurately reflect their financial behavior.

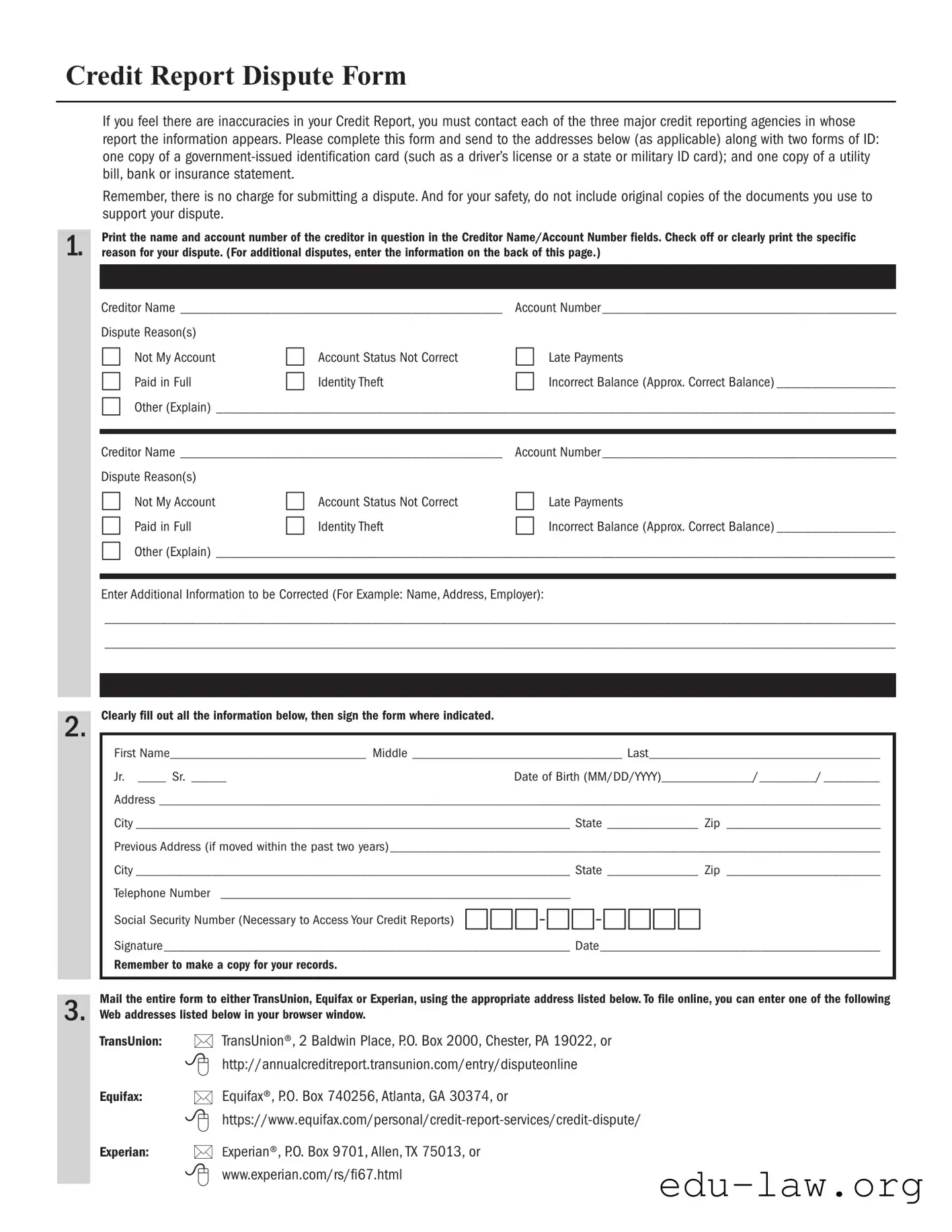

Credit Report Dispute Form

If you feel there are inaccuracies in your Credit Report, you must contact each of the three major credit reporting agencies in whose report the information appears. Please complete this form and send to the addresses below (as applicable) along with two forms of ID: one copy of a

Remember, there is no charge for submitting a dispute. And for your safety, do not include original copies of the documents you use to support your dispute.

Print the name and account number of the creditor in question in the Creditor Name/Account Number fields. Check off or clearly print the specific

1. reason for your dispute. (For additional disputes, enter the information on the back of this page.)

2.

Creditor Name ______________________________________________ |

Account Number __________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) _________________ |

□Other (Explain) _________________________________________________________________________________________________

Creditor Name ______________________________________________ |

Account Number __________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) _________________ |

□Other (Explain) _________________________________________________________________________________________________

Enter Additional Information to be Corrected (For Example: Name, Address, Employer):

_________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________

Clearly fill out all the information below, then sign the form where indicated.

First Name____________________________ Middle ______________________________ Last_________________________________

Jr. ____ Sr. _____Date of Birth (MM/DD/YYYY)_____________/________/ ________

Address _______________________________________________________________________________________________________

City ______________________________________________________________ State _____________ Zip ______________________

Previous Address (if moved within the past two years) ______________________________________________________________________

City ______________________________________________________________ State _____________ Zip ______________________

Telephone Number __________________________________________________

Social Security Number (Necessary to Access Your Credit Reports)

Signature __________________________________________________________ Date________________________________________

Remember to make a copy for your records.

Mail the entire form to either TransUnion, Equifax or Experian, using the appropriate address listed below. To file online, you can enter one of the following

3. Web addresses listed below in your browser window.

TransUnion:

Equifax:

Experian:

•TransUnion®, 2 Baldwin Place, P.O. Box 2000, Chester, PA 19022, or

•http://annualcreditreport.transunion.com/entry/disputeonline

•Equifax®, P.O. Box 740256, Atlanta, GA 30374, or

•

•Experian®, P.O. Box 9701, Allen, TX 75013, or

•www.experian.com/rs/fi67.html

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

| Fact Name | Description |

|---|---|

| Purpose | The Credit Report Dispute form allows individuals to challenge inaccuracies in their credit reports. |

| Eligibility | Any consumer who believes their credit report contains errors can use this form to initiate a dispute. |

| Required Information | Personal identification details, account numbers, and a description of the disputed information must be provided. |

| Submission Methods | The form can typically be submitted online, via mail, or by fax, depending on the credit reporting agency. |

| Response Time | Credit reporting agencies are required to investigate disputes and respond within 30 days. |

| State-Specific Forms | Some states may have specific forms or additional requirements based on local laws. |

| Governing Laws | The Fair Credit Reporting Act (FCRA) governs the dispute process at the federal level. |

| Consumer Rights | Consumers have the right to receive a free copy of their credit report if a dispute results in a change. |

After you complete the Credit Report Dispute form, you will submit it to the credit reporting agency. They will review your dispute and respond accordingly. Be sure to keep a copy for your records.

What is a Credit Report Dispute form?

A Credit Report Dispute form is a document that individuals can use to challenge inaccuracies or errors found in their credit reports. These reports, which are compiled by credit reporting agencies, contain detailed information about a person's credit history, including accounts, payment history, and any public records. If you find any discrepancies, such as incorrect account balances or accounts that do not belong to you, this form allows you to formally dispute those errors and seek corrections.

How do I fill out the Credit Report Dispute form?

Filling out the Credit Report Dispute form is a straightforward process. Start by providing your personal information, including your name, address, and Social Security number. Next, clearly identify the items you are disputing by including specific details such as account numbers and the nature of the dispute. Be concise but thorough in your explanation. Finally, sign and date the form before submitting it to the relevant credit reporting agency. Always keep a copy for your records.

Where do I send my Credit Report Dispute form?

The Credit Report Dispute form should be sent directly to the credit reporting agency that issued the report containing the errors. Major agencies include Equifax, Experian, and TransUnion. Each agency has its own procedures for handling disputes, so it’s important to check their websites for specific mailing addresses or electronic submission options. Sending your dispute via certified mail can provide proof of your submission.

How long does it take to resolve a dispute?

Once a Credit Report Dispute form is submitted, the credit reporting agency typically has 30 days to investigate the claim. During this period, they will review the information provided, contact the creditor involved, and determine whether the disputed information is accurate. After the investigation is complete, you will receive a written response detailing the outcome. If the dispute is resolved in your favor, the agency will update your credit report accordingly.

What if my dispute is not resolved in my favor?

If your dispute is not resolved in your favor, you still have options. You can request a copy of the investigation results, which may provide insight into why the agency upheld the information. Additionally, you can add a statement of dispute to your credit report, explaining your position regarding the contested information. This statement will be visible to anyone who checks your credit report in the future, providing context for potential lenders.

Not Including Sufficient Details: When filling out the Credit Report Dispute form, many people fail to provide enough information about the error. This can include missing account numbers, incorrect dates, or vague descriptions of the issue. Providing specific details helps the credit bureau investigate the claim effectively.

Neglecting to Attach Supporting Documents: Some individuals forget to include necessary documentation that supports their dispute. This might involve copies of bills, payment confirmations, or previous correspondence. Without these documents, the dispute may be harder to resolve.

Using Inappropriate Language: It's common for people to express frustration in their disputes. However, using harsh or accusatory language can detract from the professionalism of the request. A calm and factual tone is more likely to yield positive results.

Failing to Follow Up: After submitting a dispute, many assume the matter is resolved. However, it’s crucial to follow up. Checking in on the status of the dispute can ensure that it is being addressed and can help prevent delays.

When disputing inaccuracies on a credit report, several forms and documents can assist in the process. These documents help provide clarity, support your claims, and ensure that your dispute is processed efficiently. Below is a list of common forms and documents that may accompany a Credit Report Dispute form.

Understanding these forms and documents can significantly enhance your ability to navigate the dispute process effectively. By gathering the necessary paperwork, you can present a strong case and work toward correcting any inaccuracies on your credit report.

The Credit Report Dispute form is similar to the Identity Theft Report. This document serves as a formal declaration that your personal information has been misused. Just like the Credit Report Dispute form, it allows you to provide details about the fraudulent activity. Both forms aim to protect your financial standing and rectify inaccuracies that may arise from identity theft. Completing an Identity Theft Report can also bolster your case when disputing charges or accounts that are not yours, much like the Credit Report Dispute form helps address errors in your credit report.

Another document that shares similarities is the Consumer Complaint Form. This form is used to report issues with financial institutions, credit reporting agencies, or other businesses. Like the Credit Report Dispute form, it requires detailed information about the problem and your contact information. Both documents are designed to initiate a formal process for addressing grievances, ensuring that your concerns are documented and investigated by the appropriate parties.

The Request for Credit Report form is also akin to the Credit Report Dispute form. This document allows consumers to obtain their credit reports from reporting agencies. Both forms involve personal information and are crucial for maintaining accurate credit records. By requesting your credit report, you can identify errors that may need to be disputed, making the two documents interconnected in the journey toward financial accuracy.

The Fair Credit Reporting Act (FCRA) Complaint Form is another relevant document. This form is used to report violations of the Fair Credit Reporting Act, which governs how credit information is collected and shared. Similar to the Credit Report Dispute form, it addresses issues regarding the accuracy and completeness of credit reports. Both documents empower consumers to take action when their rights are violated, ensuring that they can seek justice and rectify any inaccuracies in their credit history.

The Debt Validation Letter is also comparable to the Credit Report Dispute form. This letter is sent to creditors to request validation of a debt, asserting your right to confirm its legitimacy. Both documents require clear communication of your concerns and provide a structured way to address inaccuracies. The Debt Validation Letter can serve as a precursor to filing a dispute if the debt is found to be erroneous, linking the two processes together.

Lastly, the Credit Freeze Request form shares a connection with the Credit Report Dispute form. A credit freeze restricts access to your credit report, making it harder for identity thieves to open accounts in your name. While the Credit Report Dispute form addresses existing inaccuracies, the Credit Freeze Request form proactively protects your credit from potential fraud. Both documents reflect a consumer's right to manage and safeguard their credit information effectively.

When filling out a Credit Report Dispute form, it is essential to approach the task with care. Below is a list of things you should and shouldn't do to ensure your dispute is processed effectively.

Things You Should Do:

Things You Shouldn't Do:

Many individuals have misunderstandings about the Credit Report Dispute form. Clearing up these misconceptions can empower consumers to take control of their credit reports. Here are eight common misconceptions:

Understanding these misconceptions can help individuals navigate the dispute process more effectively, ensuring their credit reports reflect their true financial history.

Filling out and using the Credit Report Dispute form can be straightforward if you keep a few key points in mind. Here are some essential takeaways:

By keeping these takeaways in mind, you can navigate the dispute process more effectively and ensure your credit report reflects accurate information.