The CP75A form is an important document issued by the Internal Revenue Service (IRS) when a taxpayer's return is selected for an audit. This notice specifically addresses the audit of the 2016 Form 1040 and requests supporting documentation for certain items claimed on the return. Taxpayers are required to respond within 30 days of the notice date, which is January 28, 2019, to avoid disallowance of the audited items. The form outlines specific steps to take, including submitting copies of the requested documentation and completing a response form. One key area often scrutinized is the Earned Income Credit, where taxpayers must provide evidence that their qualifying child meets the necessary tests. If the IRS does not receive the required information within the specified timeframe, it may propose changes to the tax return, potentially resulting in additional taxes owed. The CP75A also includes resources for taxpayers, such as contact information for the IRS, links to helpful publications, and options for assistance through the Taxpayer Advocate Service and Low Income Taxpayer Clinics. Understanding the requirements and responding promptly can significantly impact the outcome of the audit process.

Department of the Treasury |

Notice |

CP75A |

||

Tax year |

2016 |

|||

Internal Revenue Service |

||||

Notice date |

January 28, 2019 |

|||

Examination Operations Stop 22B |

||||

Social Security number |

||||

PO Box |

|

|||

|

To contact us |

Phone |

||

Doraville, GA |

||||

Your Caller ID |

|

|||

|

|

|

||

|

|

Page 1 of 3 |

|

|

TAXPAYER NAME ____________________ |

|

|

||

ADDRESS |

____________________ |

|

|

|

CITY, STATE ZIP |

____________________ |

|

|

|

|

|

|

||

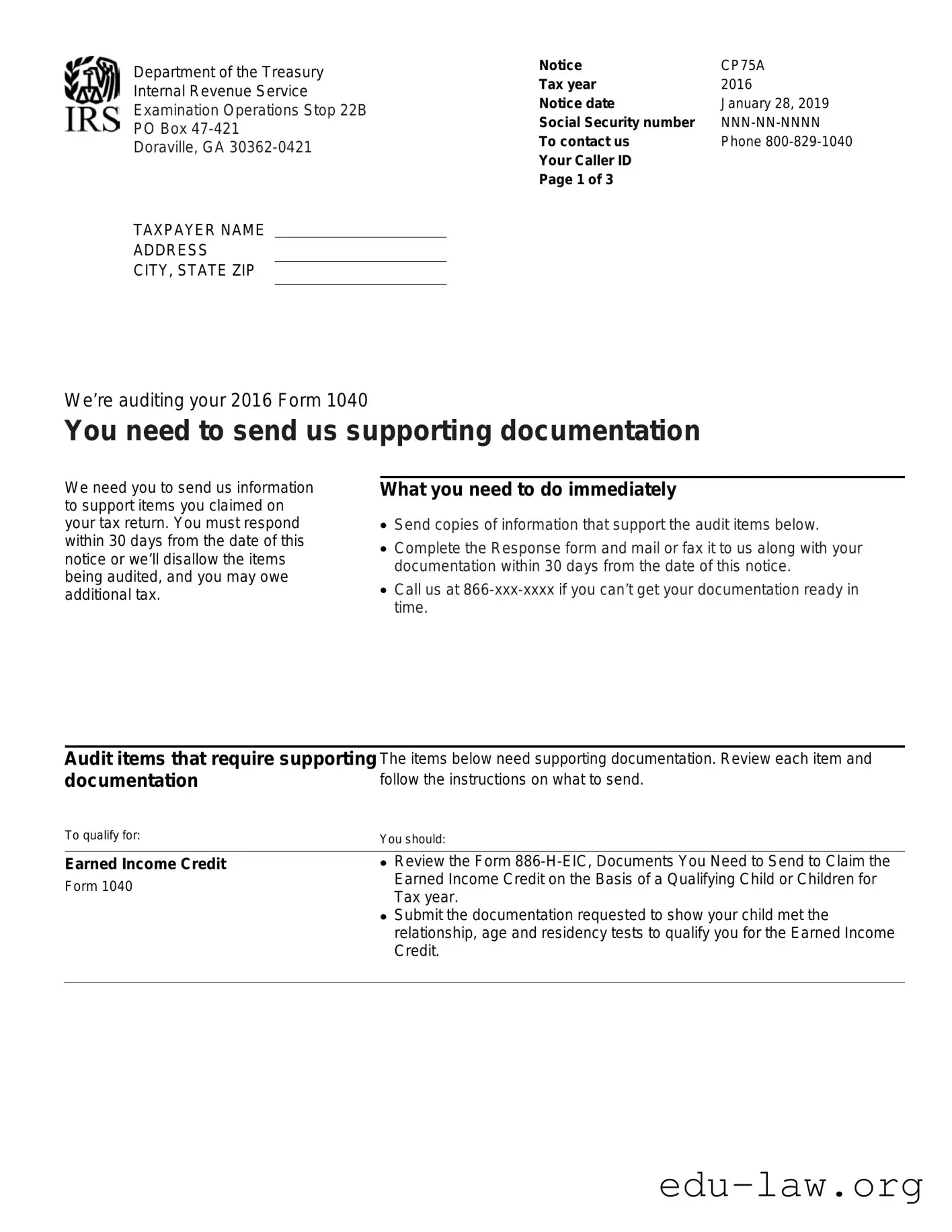

We’re auditing your 2016 Form 1040

You need to send us supporting documentation

We need you to send us information to support items you claimed on your tax return. You must respond within 30 days from the date of this notice or we’ll disallow the items being audited, and you may owe additional tax.

What you need to do immediately

•Send copies of information that support the audit items below.

•Complete the Response form and mail or fax it to us along with your documentation within 30 days from the date of this notice.

•Call us at

Audit items that require supporting The items below need supporting documentation. Review each item and

documentation |

follow the instructions on what to send. |

To qualify for: |

You should: |

Earned Income Credit

Form 1040

•Review the Form

•Submit the documentation requested to show your child met the relationship, age and residency tests to qualify you for the Earned Income Credit.

Notice |

CP75A |

Tax year |

2016 |

Notice date |

January 28, 2019 |

Social Security number |

|

Page 2 of 3 |

|

If we don’t hear from you |

If you don’t mail or fax your supporting documentation within 30 days from |

|

the date of this notice, we’ll disallow the items being audited and send you |

|

an audit report showing the proposed changes to your tax return. |

|

|

Next steps |

• We’ll review the information you provide (please allow us at least 30 |

|

days). |

|

• If the information supports your tax return, we’ll send your refund and a |

|

letter letting you know your audit is closed. |

|

• If the information doesn’t fully support your tax return, we’ll send you an |

|

audit report that explains the proposed changes, including any additional |

|

tax you may owe plus any penalties and interest that may apply. |

Additional information

•Visit www.irs.gov/cp75a

•Review the enclosed documents and The Examination Process (Publication

•For tax forms, instructions, and publications, visit

•Review the enclosed Publication 1, Your Rights as a Taxpayer.

•Keep this notice for your records.

If you need assistance, please don’t hesitate to contact us.

Taxpayer Advocate Service

The Taxpayer Advocate Service (TAS) is an independent organization within the IRS that can help protect your taxpayer rights. TAS can offer you help if your tax problem is causing a hardship, or you've tried but haven't been able to resolve your problem with the IRS. If you qualify for TAS assistance, which is always free, TAS will do everything possible to help you. Visit www.taxpayeradvocate.irs.gov or call

Low Income Taxpayer Clinics (LITC)

Assistance can be obtained from individuals and organizations that are independent from the IRS. The Directory of Federal Tax Return Preparers with credentials recognized by the IRS can be found at http://irs.treasury.gov/rpo/rpo.jsf. IRS Publication 4134 provides a listing of Low Income Taxpayer Clinics (LITCs) and is available at www.irs.gov. Also, see the LITC page at www.taxpayeradvocate.irs.gov/litcmap. Assistance may also be available from a referral system operated by a state bar association, a state or local society of accountants or enrolled agents or another nonprofit tax professional organization. The decision to obtain assistance from any of these individuals and organizations will not result in the IRS giving preferential treatment in the handling of the issue, dispute or problem. You don’t need to seek assistance to contact us. We will be pleased to deal with you directly and help you resolve your situation.

Department of the Treasury

Internal Revenue Service

Examination Operations Stop 22B

PO Box

Doraville, GA

INTERNAL REVENUE SERVICE

Examination Operations Stop 22B

PO Box

Doraville, GA

Response form

Complete this form, and mail or fax it to us within 30 days from the date of this notice. If you use the enclosed envelope, be sure our address shows through the window.

Notice |

CP75A |

Tax year |

2016 |

Notice date |

January 28, 2019 |

Social Security number |

|

Page 3 of 3 |

|

Provide your contact information

If your address has changed, please call

TAXPAYER NAME

ADDRESS

CITY, STATE ZIP

|

a.m. |

|

a.m. |

|

p.m. |

|

p.m. |

Primary phone |

Best time to call |

Secondary phone |

Best time to call |

1.Indicate which items you’re addressing with supporting documents

The enclosed documentation supports my 2016 tax return (check all that apply):

Earned Income Credit, Form 1040

2.Send this Response form to us

Mail or fax your Response form to us along with any documentation within 30 days from the date of this notice. If you’re using your own envelope, mail your package to the address on this form or, fax it to

| Fact Name | Fact Description |

|---|---|

| Purpose | The CP75A form is a notice from the IRS informing taxpayers that their 2016 Form 1040 is being audited. |

| Response Timeframe | Taxpayers must respond within 30 days of the notice date to avoid disallowance of the items being audited. |

| Documentation Required | Taxpayers are required to submit supporting documentation for items claimed on their tax return, specifically for the Earned Income Credit. |

| Contact Information | For assistance, taxpayers can contact the IRS at 800-829-1040 or the Taxpayer Advocate Service at 877-777-4778. |

| Audit Process | If the IRS does not receive documentation, they will disallow the items and send an audit report detailing proposed changes. |

| Additional Resources | Taxpayers can access further information at www.irs.gov/cp75a and review IRS Publication 1 for taxpayer rights. |

After receiving the CP75A form, it is important to respond promptly. This form indicates that the IRS is auditing your 2016 tax return, and they require supporting documentation for specific items. Failure to respond within 30 days may lead to disallowance of the items being audited, which could result in additional tax liability.

What is the purpose of the CP75A form?

The CP75A form serves as a notification from the Internal Revenue Service (IRS) regarding an audit of your 2016 tax return, specifically your Form 1040. It informs you that the IRS requires supporting documentation for certain items you claimed on your return. This notice is crucial because it outlines the steps you must take to avoid disallowance of those items, which could result in additional taxes owed.

What should I do if I receive a CP75A notice?

Upon receiving a CP75A notice, you must act promptly. You are required to gather and send copies of the documentation that supports the items under audit. This documentation must be submitted within 30 days from the date of the notice. Additionally, you should complete the Response form included with the notice and return it along with your supporting documents. If you cannot prepare your documentation in time, you should contact the IRS at the provided phone number to discuss your situation.

What happens if I do not respond to the CP75A notice?

If you fail to respond within the specified 30-day period, the IRS will disallow the items being audited. Consequently, you may receive an audit report that outlines proposed changes to your tax return, including any additional taxes you may owe, as well as potential penalties and interest. It is essential to adhere to the timeline to avoid these repercussions.

What types of documentation might I need to provide?

The documentation you need to submit will depend on the specific items being audited. For example, if you claimed the Earned Income Credit, you will need to provide proof that your child met the relationship, age, and residency tests. The IRS provides guidance on what documents are acceptable, and you should carefully review these requirements in the notice and any accompanying materials.

How can I get help if I am having trouble with the CP75A process?

If you encounter difficulties while navigating the CP75A process, assistance is available. You can contact the Taxpayer Advocate Service (TAS), which is an independent organization within the IRS dedicated to protecting taxpayer rights. They can help you if your tax issue is causing a hardship or if you have been unable to resolve your problem directly with the IRS. Additionally, you may seek help from Low Income Taxpayer Clinics (LITCs) or other tax professionals who can provide guidance and support.

Where can I find more information about the CP75A notice?

For further details regarding the CP75A notice, you can visit the IRS website at www.irs.gov/cp75a. The site contains valuable resources, including the Examination Process publication, which outlines your appeal rights. You can also find additional tax forms, instructions, and publications by visiting www.irs.gov/forms-pubs or calling 800-TAX-FORM. Keeping the CP75A notice for your records is advisable, as it contains important information relevant to your audit.

Missing Information: Failing to fill in the taxpayer name, address, and contact information can lead to delays. Ensure all fields are completed accurately.

Incorrect Social Security Number: Providing an incorrect Social Security number can cause significant issues. Double-check this number for accuracy.

Not Responding on Time: Ignoring the 30-day deadline can result in disallowed claims. It’s crucial to send your documentation promptly.

Inadequate Documentation: Submitting insufficient or irrelevant documents can hinder your case. Make sure to include all required supporting materials.

Failing to Check the Right Boxes: Not indicating which items you are addressing can create confusion. Carefully check all applicable items on the response form.

Using the Wrong Submission Method: Sending documents to the wrong address or using an incorrect fax number may delay your response. Verify the submission details before sending.

Not Keeping Copies: Failing to keep copies of submitted documents can be problematic. Always retain copies for your records.

Ignoring Follow-Up: Not following up after submitting your documents can lead to missed communications. Stay proactive in checking the status of your submission.

Overlooking Additional Resources: Not utilizing available resources, such as the Taxpayer Advocate Service or Low Income Taxpayer Clinics, can limit your support options. Explore these resources for assistance.

The CP75A form is a notice issued by the IRS during an audit process. When responding to this notice, several other forms and documents may be necessary to support your claims. Below is a list of common documents that are often used alongside the CP75A form.

Gathering the appropriate forms and documents is crucial when responding to the CP75A notice. Doing so will help ensure that your case is properly reviewed and that you have the best chance of resolving any issues with the IRS efficiently.

The CP75A form is similar to the CP2000 notice. The CP2000 informs taxpayers of proposed changes to their tax returns based on discrepancies between the information the IRS has and what the taxpayer reported. Like the CP75A, it requires a response within a specified timeframe. Taxpayers must provide documentation to support their claims or face potential adjustments to their tax liabilities. The emphasis is on communication and supporting evidence, making both forms critical for resolving tax discrepancies.

Another document akin to the CP75A is the IRS Notice of Deficiency, also known as a 90-day letter. This notice indicates that the IRS believes a taxpayer owes additional tax. It provides a detailed explanation of the proposed changes and gives the taxpayer 90 days to respond. Similar to the CP75A, the Notice of Deficiency requires the taxpayer to gather and submit supporting documentation to contest the IRS's findings. Both documents underscore the importance of timely responses to avoid further complications.

The CP14 notice is another document that shares similarities with the CP75A. The CP14 serves as a reminder of unpaid taxes, detailing the amount owed and the due date. It prompts taxpayers to act quickly to resolve their tax obligations. Like the CP75A, it emphasizes the need for timely communication with the IRS to prevent additional penalties or interest from accruing. Both notices highlight the IRS's proactive approach to tax collection and compliance.

The CP21B notice is also comparable to the CP75A. This notice is issued when the IRS makes an adjustment to a taxpayer's return, often resulting in a refund. It provides a summary of the changes made and the refund amount. While the CP75A requests supporting documentation, the CP21B confirms adjustments already made by the IRS. Both documents reflect the IRS's commitment to transparency and accuracy in tax administration.

The 1040X form, which is used to amend a tax return, is similar to the CP75A in that both involve corrections to previously filed returns. Taxpayers use the 1040X to report changes and provide explanations for those changes. Like the CP75A, it requires supporting documentation to substantiate the amendments. Both forms highlight the necessity of accurate information in tax filings and the importance of addressing discrepancies promptly.

The IRS Form 886-H-EIC is also relevant to the CP75A. This form is specifically used to provide documentation for claiming the Earned Income Credit. Similar to the CP75A, it outlines the necessary documentation needed to support eligibility for the credit. Both forms emphasize the importance of proving eligibility and ensuring compliance with tax regulations, particularly concerning credits and deductions.

The CP15 notice, which informs taxpayers of a balance due, is another document akin to the CP75A. The CP15 provides details about the amount owed and the payment options available. It serves as a reminder to taxpayers to take action to avoid further penalties. Like the CP75A, it stresses the importance of timely responses to avoid escalation of tax issues.

Lastly, the IRS Form 4506-T, which is used to request a transcript of a tax return, is similar to the CP75A in that both involve the retrieval of tax information. Taxpayers may need to request a transcript to support their claims or respond to an audit notice like the CP75A. Both documents reflect the IRS's emphasis on maintaining accurate records and providing taxpayers with the necessary tools to address their tax situations effectively.

When filling out the CP75A form, it's essential to approach the task with care. Here’s a list of things to do and avoid to ensure a smooth process.

Following these guidelines can help streamline your experience with the IRS and ensure that you provide the necessary information effectively.

Understanding the CP75A form is essential for taxpayers who receive it. Unfortunately, several misconceptions can lead to confusion. Here are ten common misunderstandings about the CP75A form:

Addressing these misconceptions can help taxpayers navigate the audit process more effectively. Staying informed and proactive is key to resolving any issues related to the CP75A form.

When dealing with the CP75A form, it is crucial to understand the steps you need to take. Here are six key takeaways to keep in mind:

Taking these steps seriously can help you navigate the audit process more effectively and ensure that you meet all necessary requirements.