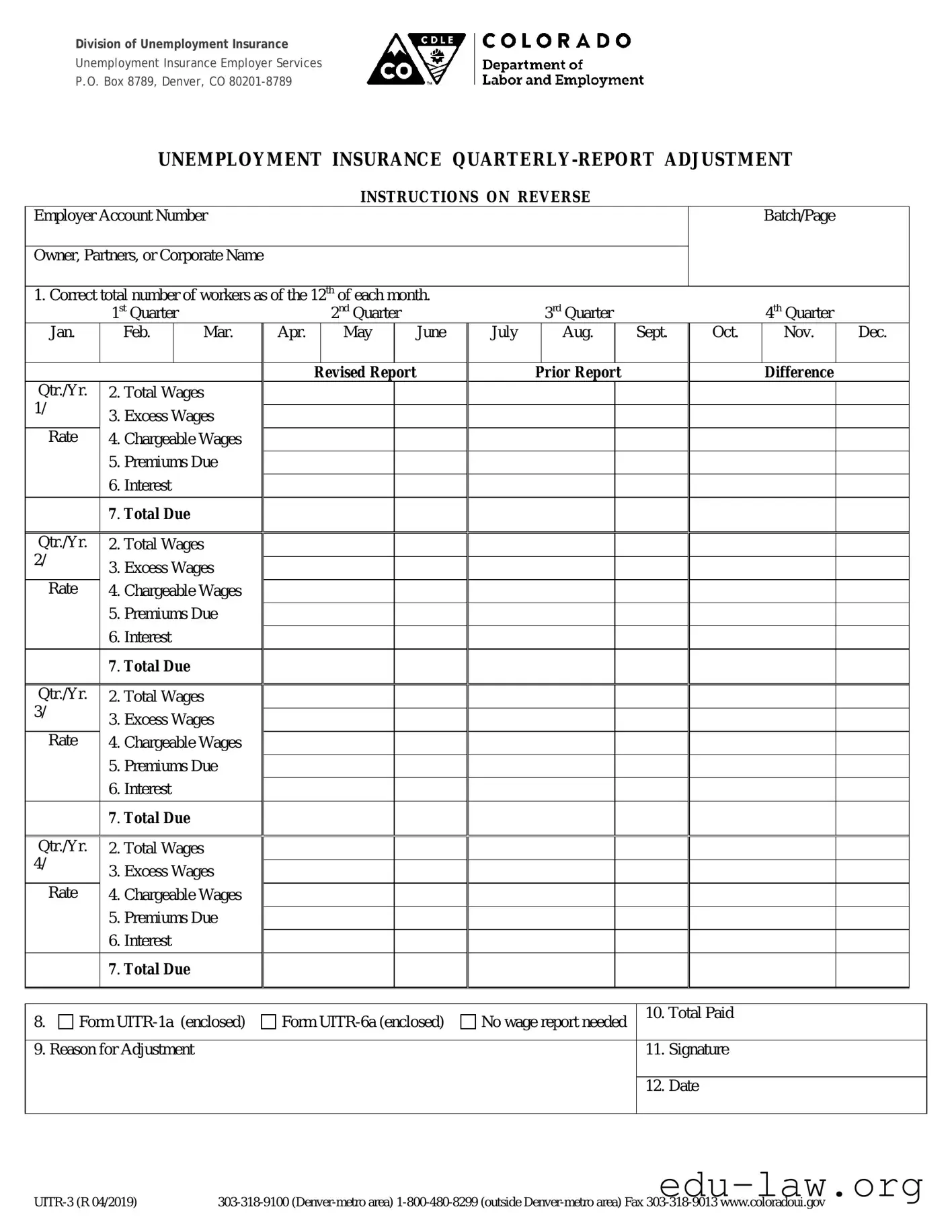

The Co Uitr 1 form is an essential document for employers in Colorado who need to report adjustments to their unemployment insurance quarterly reports. This form allows employers to correct previously submitted data regarding the number of workers, total wages, and other related figures. It includes sections for reporting the correct total number of workers as of the 12th of each month, as well as the total wages paid during the quarter. Employers must also account for excess wages, which are defined as wages exceeding the chargeable wage limit. This form requires the calculation of premiums due based on the chargeable wages, and it includes a section for reporting any interest owed on late payments. Additionally, employers are instructed to provide reasons for any adjustments made, ensuring clarity and transparency in the reporting process. The Co Uitr 1 form is a vital tool for maintaining compliance with unemployment insurance regulations and ensuring that all wage information is accurate and up to date.

Division of Unemployment Insurance

Unemployment Insurance Employer Services

P.O. Box 8789, Denver, CO

UNEMPLOYMENT INSURANCE

|

|

|

|

INSTRUCTIONS ON REVERSE |

|

|

|

|

|||

Employer Account Number |

|

|

|

|

|

|

|

Batch/Page |

|

||

|

|

|

|

|

|

|

|

|

|

||

Owner, Partners, or Corporate Name |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||||

1. Correct total number of workers as of the 12th of each month. |

|

|

|

|

|

|

|||||

|

1st Quarter |

|

|

2nd Quarter |

|

|

3rd Quarter |

|

|

4th Quarter |

|

Jan. |

Feb. |

Mar. |

Apr. |

May |

June |

July |

Aug. |

Sept. |

Oct. |

Nov. |

Dec. |

|

|

|

|

Revised Report |

|

Prior Report |

|

Difference |

Qtr./Yr. |

2. Total Wages |

|

|

|

|

|||

1/ |

|

|

|

|

|

|

|

|

3. |

Excess Wages |

|

|

|

|

|

||

|

|

|

|

|

||||

Rate |

4. |

Chargeable Wages |

|

|

|

|

||

5.Premiums Due

6.Interest

|

7. Total Due |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Qtr./Yr. |

2. Total Wages |

|

|

|

|

|

|

2/ |

3. |

Excess Wages |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

||

Rate |

4. Chargeable Wages |

|

|

|

|

|

|

|

5. |

Premiums Due |

|

|

|

|

|

|

6. |

Interest |

|

|

|

|

|

|

7. Total Due |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Qtr./Yr. |

2. Total Wages |

|

|

|

|

|

|

3/ |

3. |

Excess Wages |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Rate |

4. Chargeable Wages |

|

|

|

|

|

|

|

5. |

Premiums Due |

|

|

|

|

|

|

6. |

Interest |

|

|

|

|

|

|

7. Total Due |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Qtr./Yr. |

2. Total Wages |

|

|

|

|

|

|

4/ |

3. |

Excess Wages |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

||

Rate |

4. Chargeable Wages |

|

|

|

|

|

|

|

5. |

Premiums Due |

|

|

|

|

|

|

6. |

Interest |

|

|

|

|

|

|

7. Total Due |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. |

Form |

Form |

No wage report needed |

10. Total Paid |

|

|

|

||||

|

|

|

|

|

|

9. Reason for Adjustment |

|

|

11. |

Signature |

|

|

|

|

|

|

|

|

|

|

|

12. |

Date |

|

|

|

|

|

|

INSTRUCTIONS FOR THE UNEMPLOYMENT INSURANCE

1.Number of

2.Total

NOTE: Form

3.Excess

Chargeable wage limits: 2019: |

$13,100 |

2017: |

$12,500 |

2015: |

$11,800 |

2018: |

$12,600 |

2016: |

$12,200 |

2014: |

$11,700 |

4. Chargeable

EXAMPLE OF COMPUTING CHARGEABLE WAGES FOR 2019

|

1st Quarter |

2nd Quarter |

3rd Quarter |

4th Quarter |

Gross Wages |

$6,000 |

$6,000 |

$4,000 |

$6,000 |

Excess of $13,100 |

$4,900 |

$6,000 |

||

Chargeable Wages |

$6,000 |

$6,000 |

$1,100 |

5.Premiums

6.Interest

7.Check the appropriate box as described below:

Form

Form

No Wage Report

8.Reason for

If you have any questions, please call Unemployment Insurance Employer Services at

www.coloradoui.gov |

|

| Fact Name | Description |

|---|---|

| Purpose | The Co Uitr 1 form is used to adjust quarterly unemployment insurance reports in Colorado. |

| Governing Law | This form is governed by the Colorado Employment Security Act. |

| Reporting Periods | Employers must report for four quarters: January-March, April-June, July-September, and October-December. |

| Workers Count | Employers must provide the correct total number of workers as of the 12th of each month. |

| Wages Reporting | Total wages must reflect only those actually paid during the quarter, minus allowable deductions. |

| Adjustment Reasons | Employers must specify reasons for adjustments to the original report, ensuring transparency. |

| Contact Information | For assistance, employers can call 303-318-9100 or 1-800-480-8299, depending on their location. |

Filling out the Co Uitr 1 form is an essential step for employers looking to adjust their unemployment insurance quarterly reports. After completing the form, you will need to submit it to the appropriate state department for processing. Follow the steps below to ensure accuracy and completeness.

What is the purpose of the Co Uitr 1 form?

The Co Uitr 1 form is used for making adjustments to previously reported unemployment insurance quarterly reports. Employers can correct errors related to the number of workers, total wages, and other relevant details that impact unemployment insurance premiums and charges.

How do I report the number of workers on the form?

To report the number of workers, enter the correct total number of employees as of the 12th of each month for the quarter in question. This information is crucial if the original report contained inaccuracies.

What should I include in the total wages section?

In the total wages section, report the wages paid during the quarter that are subject to unemployment insurance premiums. This means you should include only the wages you actually paid, minus any allowable deductions. If you have made adjustments to wages in previous quarters, you must complete and attach Form UITR-6a.

What are chargeable wages and how are they calculated?

Chargeable wages refer to the first $13,100 of wages paid to a worker during the calendar year. For example, if an employee earns $6,000 in the first quarter, that amount is fully chargeable. If the total wages exceed the chargeable limit, only the portion up to that limit counts toward unemployment insurance premiums.

How do I calculate premiums due?

To calculate premiums due, multiply the employer’s rate by the chargeable wages. For instance, if your rate is 0.0170 and your chargeable wages are $6,000, the premium would be $102.00.

What happens if I submit the form late?

If the form is submitted after the due date, interest will be charged at a rate of 1.5 percent per month or any portion of a month. This interest is calculated on the premiums due and must be included in your total payment.

How do I indicate the reason for the adjustment?

In the designated section of the form, clearly list the reasons for making the adjustment. This helps clarify why the original report is being changed and ensures proper processing of your submission.

Incorrect Worker Count: Many people fail to update the number of workers correctly. This is crucial, as the total number of workers reported on the original form must match the actual count as of the 12th of each month.

Misreporting Total Wages: Another common mistake is entering incorrect total wages. Ensure that only the wages actually paid during the quarter are reported. Deductions should not be included in this figure.

Ignoring Excess Wages: Some individuals overlook the excess wages section. It's important to report any wages paid over the chargeable wage limit. This can lead to errors in calculating premiums owed.

Missing Reason for Adjustment: Failing to provide a reason for the adjustment can lead to confusion. Always list the reasons for changes made to the original report. This helps clarify your intentions and can expedite processing.

When dealing with the Co Uitr 1 form, several other documents often come into play. Each of these forms serves a specific purpose, helping to ensure accurate reporting and compliance with unemployment insurance regulations. Below is a brief overview of these related forms.

Each of these forms and documents plays a critical role in the unemployment insurance reporting process. By understanding their purposes and how they relate to the Co Uitr 1 form, employers can ensure that they remain compliant and avoid potential issues with their unemployment insurance obligations.

The Form UITR-1 is similar to the W-2 form, which employers use to report wages paid to employees and the taxes withheld from those wages. Both documents serve the purpose of providing a summary of employee earnings for a specific period. While the W-2 focuses on individual employee earnings and tax withholdings, the UITR-1 summarizes the total wages and number of workers for the employer's overall unemployment insurance reporting. This makes both forms essential for accurate tax reporting and compliance with state and federal regulations.

Another document comparable to the UITR-1 is the 1099 form, which is used to report income received by independent contractors and freelancers. Like the UITR-1, the 1099 form captures earnings within a specified time frame. However, the UITR-1 is specifically tailored for reporting unemployment insurance contributions, while the 1099 is more general, covering various types of income. Both forms require accurate reporting to ensure compliance with tax obligations.

The Form UITR-3 is also similar to the UITR-1, as it is used for reporting unemployment insurance information but focuses on adjustments. The UITR-3 is utilized when an employer needs to correct previously reported data, while the UITR-1 is for initial quarterly reporting. Both forms share the goal of ensuring accurate wage reporting for unemployment insurance purposes, but they serve different stages in the reporting process.

The Form UITR-6a, which is used for multiple quarter adjustments, parallels the UITR-1 in that it addresses wage reporting but is specifically designed for making corrections across multiple quarters. This form allows employers to amend previous reports, similar to how the UITR-1 serves as the primary report for a single quarter. Both forms require accurate wage calculations to maintain compliance with unemployment insurance regulations.

Another document that resembles the UITR-1 is the IRS Form 941, which is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Both forms require employers to report on wages paid, but the UITR-1 focuses on unemployment insurance while Form 941 addresses federal tax obligations. Accurate completion of both forms is crucial for maintaining compliance with tax laws.

The State Unemployment Tax Act (SUTA) form is also similar to the UITR-1, as it relates to state unemployment tax reporting. Both documents require employers to report wages and employee counts to determine tax liabilities. The UITR-1 is specific to Colorado’s unemployment insurance program, while SUTA forms vary by state. Nonetheless, both aim to ensure that employers fulfill their obligations regarding unemployment insurance contributions.

The Form UITR-1 shares similarities with the Form 1094-C, which is used by employers to report information about health coverage offered to employees. Both forms require detailed reporting of employee data, but the UITR-1 is focused on unemployment insurance, while the 1094-C pertains to health care compliance under the Affordable Care Act. Despite their different focuses, both forms are essential for compliance with federal and state regulations.

Additionally, the Form 5500 is comparable to the UITR-1 in that it is used to report information about employee benefit plans. Both forms require detailed reporting of employee-related data, but the UITR-1 is specific to unemployment insurance reporting, while the 5500 focuses on retirement and welfare benefit plans. Both documents are critical for ensuring compliance with regulations governing employee benefits.

Finally, the Form I-9, which verifies the employment eligibility of individuals, shares a connection with the UITR-1 in that both require accurate reporting of employee information. While the UITR-1 focuses on wages and unemployment contributions, the I-9 is concerned with the legal eligibility of employees to work in the United States. Both forms play vital roles in maintaining compliance with employment laws and regulations.

When filling out the Co Uitr 1 form, following the right steps can make the process smoother. Here are ten essential do's and don'ts to keep in mind:

By adhering to these guidelines, you can avoid common pitfalls and ensure that your form is filled out correctly.

Understanding the Co Uitr 1 form is crucial for employers navigating unemployment insurance adjustments. However, several misconceptions can lead to confusion. Here are some common misunderstandings:

By clarifying these misconceptions, employers can better navigate the requirements of the Co Uitr 1 form and ensure compliance with unemployment insurance regulations.

When filling out and using the Co Uitr 1 form, it is important to keep several key points in mind:

Following these guidelines will help ensure the Co Uitr 1 form is completed accurately and efficiently, minimizing potential issues with unemployment insurance reporting.