The CG 20 10 07 04 Liability Endorsement form plays a crucial role in commercial general liability insurance by providing additional insured coverage to various entities, such as owners, lessees, and contractors. This endorsement modifies the original insurance policy to extend protection to specified individuals or organizations listed in a schedule associated with the policy. The key aspects of this form include defining the circumstances under which additional insureds are covered, particularly in relation to bodily injury, property damage, and personal injury. Coverage applies when these claims arise from the actions of the primary insured or those working on their behalf while conducting ongoing operations for the additional insured at designated locations. It’s important to note that the endorsement outlines specific limitations, ensuring that the insurance provided does not exceed what is required by contract. Furthermore, it details exclusions that can affect coverage duration, particularly regarding completed work or when the work has been put to its intended use. Ultimately, this endorsement helps both the primary insured and the additional insured define their liabilities and protect their interests in contractual relationships.

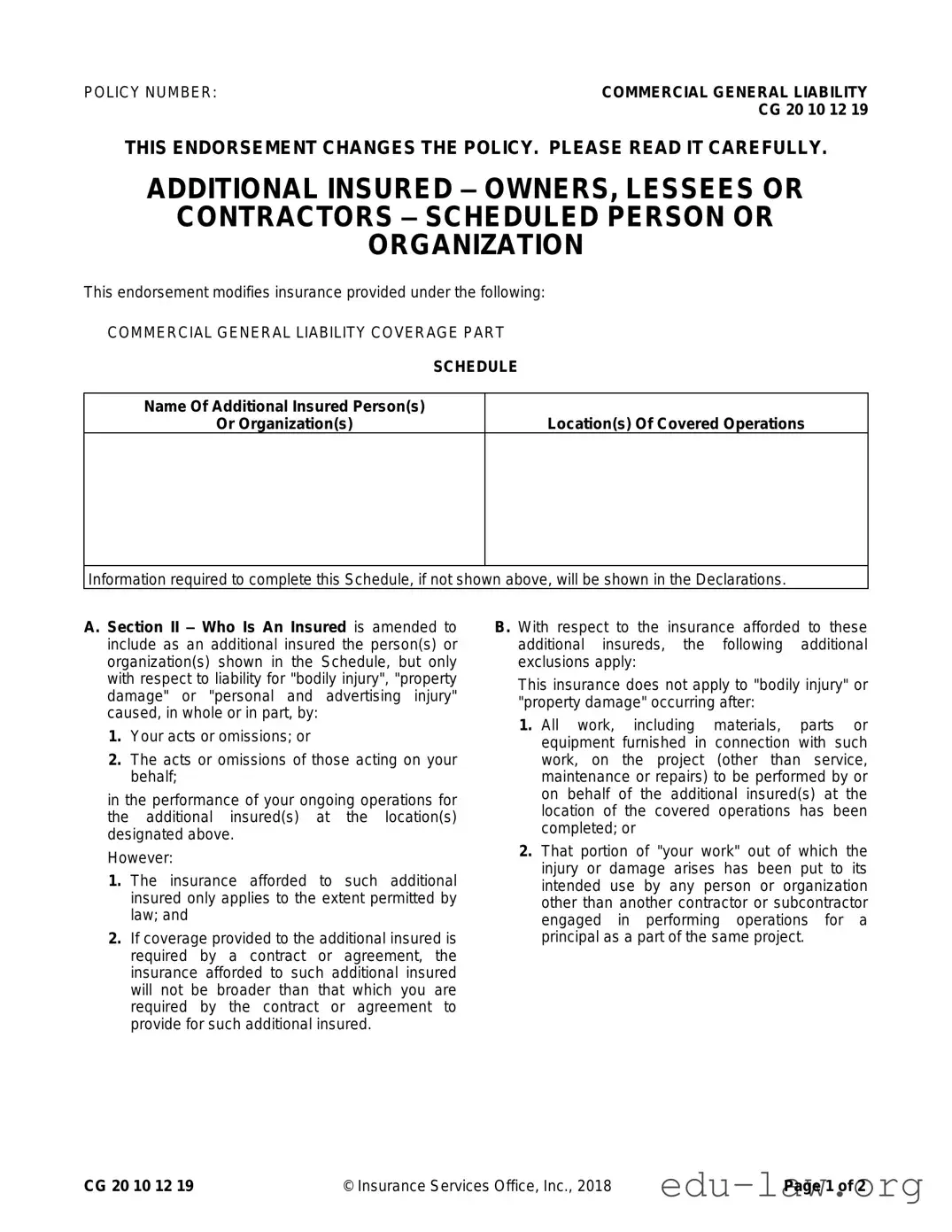

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

| Fact Name | Description |

|---|---|

| Policy Number | The policy number associated with this endorsement is CG 20 10 12 19. |

| Purpose | This endorsement is designed to add additional insureds, specifically owners, lessees, or contractors, to the general liability coverage. |

| Operation Coverage | Coverage applies only for liability related to ongoing operations at specified locations where additional insureds are involved. |

| Coverage Limitations | The endorsement does not increase the limits of insurance provided in the underlying policy. |

| Required by Contract | If coverage is required by contract, it cannot exceed what is stipulated in that contract or the policy limits, whichever is lower. |

| Exclusions | Liability coverage does not apply for work completed, unless it involves maintenance or repairs. |

| Applicable Laws | Governing law may vary by state, often following state-specific liability regulations. |

| Insurance Modifications | Section II of the policy is amended to include the individuals or organizations listed in the endorsement schedule. |

| Effective Date | The endorsement takes effect immediately upon endorsement as part of the ongoing policy. |

Filling out the CG 20 10 07 04 Liability Endorsement form is essential for designating additional insured parties under a commercial general liability policy. Ensure that you have all necessary information available as you proceed with the following steps.

Once all required information is entered and verified, ensure that you keep a copy for your records. After that, follow your insurance provider’s procedures for submitting the form to make the endorsement effective.

What is the CG 20 10 07 04 Liability Endorsement form?

The CG 20 10 07 04 Liability Endorsement is a document used to extend coverage under a Commercial General Liability (CGL) policy. It specifically adds additional insureds, such as owners, lessees, or contractors, to your insurance. This means that if someone else is harmed or has property damage as a result of your work, they may be covered under your policy as well, within the limits defined in the endorsement.

Who qualifies as an additional insured?

Additional insureds are usually specified individuals or organizations that you have a contractual obligation to cover. They can be owners, lessees, or contractors related to the work you are performing. Their names and details need to be included in the Schedule section of the endorsement for coverage to apply.

What types of incidents does this endorsement cover?

This endorsement covers claims related to bodily injury, property damage, or personal and advertising injury. However, it only applies if those incidents result from your actions or the actions of others working on your behalf while conducting operations for the additional insured at designated locations.

Are there any exclusions to this coverage?

Yes, there are specific exclusions. Coverage does not apply after all the work related to a project has been completed and no further service, maintenance, or repairs are being conducted. Additionally, if the injury or damage occurs after your work has been put to its intended use, the endorsement does not provide coverage.

How does the contract or agreement affect the additional insured coverage?

If coverage for the additional insured is required by a contract, the insurance will only extend to what is specified in that contract. This means that the protected amount cannot exceed what you’re obligated to provide through that agreement.

Will this endorsement increase my policy limits?

No, this endorsement does not increase the overall limits of your insurance policy. The coverage amounts still adhere to the original policy limits, and the most that will be paid on behalf of an additional insured will be the lesser of the required contract amount or the limits in your existing policy.

How do I fill out the Schedule on the endorsement?

The Schedule should include the names of all additional insured persons or organizations, as well as the locations where the insured operations will take place. If this information is not already specified, you will need to provide it in the Declarations section of your policy.

Can I modify who is listed as an additional insured?

Yes, you can modify the list of additional insureds by updating the Schedule in the endorsement. However, any changes should align with your insurance provider's guidelines and any applicable contracts to ensure that new parties are adequately covered.

Failing to clearly identify the names of additional insured persons or organizations. Accurate identification is crucial to ensuring that coverage applies correctly.

Omitting the locations of covered operations. This information helps determine where the coverage extends and is essential for compliance.

Providing incomplete or incorrect information in the declarations section. All relevant details must be filled in to avoid coverage disputes later.

Not understanding the limitations of the coverage offered. The endorsement only extends coverage to the extent required by law or by contract, and this must be clearly understood.

Ignoring the exclusions that apply to the additional insureds. Knowledge of these exclusions helps in assessing risk and coverage limitations.

Overlooking the requirements of the contract or agreement that necessitate the additional insured status. The coverage cannot exceed what is stipulated in the main agreement.

Not reviewing the limits of insurance carefully. When coverage is required by a contract, it will be limited to the lesser of the contract amount or the applicable policy limits.

In the realm of liability insurance, various forms and documents complement the CG 20 10 07 04 Liability Endorsement form to ensure clarity and coverage. These documents collectively help define the scope of insurance, outline obligations, and protect parties involved in contractual agreements. Each plays a pivotal role in managing risks associated with potential liabilities.

Understanding these documents can significantly enhance clarity in liability situations. Each form and endorsement serves to create a framework of protection that can help mitigate financial risks and provide peace of mind for businesses and individuals alike.

The CG 20 10 07 04 Liability Endorsement form is similar to the Additional Insured Endorsement (ISO form CG 20 33), which names an additional insured under a commercial general liability policy. Both forms extend coverage to specific persons or organizations but vary in their scope. The CG 20 33 typically covers liability arising from the named insured's operations, whereas the CG 20 10 07 04 specifically addresses ongoing operations of the additional insured, adding a layer of specificity regarding covered locations and types of injuries.

Another related document is the CG 20 10 11 85 Additional Insured – Owners, Lessees or Contractors form. This form also provides coverage to those listed as additional insureds but focuses on completed operations. In contrast, the CG 20 10 07 04 emphasizes ongoing operations, which could significantly change the exposure covered. Clients should choose based on the timing of the operations and the risks they aim to mitigate.

The CG 20 10 04 13 form similarly adds additional insureds but does so for specific contractual agreements rather than general operations. This document relies heavily on the language and requirements set out in the underlying contract. As such, it can often lead to stricter limitations on coverage compared to the CG 20 10 07 04, which provides more general coverage for ongoing activities.

Comparably, the CG 20 37 04 13 is an endorsement that covers additional insureds in connection to specific projects or venues. Unlike the CG 20 10 07 04, which focuses on specified operations, this form limits coverage to particular projects and tends to have clear geographical boundaries. It can be beneficial for businesses engaged in project-based work, where both the exact project and location can be defined in advance.

The CG 20 11 form, Often referred to as the "Designated Construction Project" endorsement, is another relevant document. It extends coverage in the context of construction projects and includes specific language about who is covered. This differs from the CG 20 10 07 04, which does not have to be project-specific but can cover broader ongoing operations regardless of the project type.

Similarly, the CG 20 10 06 85 endorsement focuses on additional insureds that are created through contract requirements. It applies a similar structure to the CG 20 10 07 04 but places greater emphasis on compliance with contractual obligations, ensuring that coverage aligns precisely with what's required by those contracts. This can lead to tighter restrictions and potentially less generous coverage compared to the CG 20 10 07 04.

Lastly, the CG 20 10 11 08 is designed for joint ventures and partnerships, providing additional insured status to parties involved in such arrangements. While the CG 20 10 07 04 deals primarily with liability linked to ongoing operations, the CG 20 10 11 08 focuses more on collective actions and liabilities within joint ventures, making it pertinent for businesses collaborating on specific projects.

Filling out the CG 20 10 07 04 Liability Endorsement form requires attention to detail. Below is a list of important do's and don'ts that can help ensure the process goes smoothly.

Understanding the CG 20 10 07 04 Liability Endorsement is crucial for policyholders. There are several misconceptions that can lead to confusion regarding coverage. Here’s a list of six common misconceptions:

Being aware of these misconceptions helps in making informed decisions about insurance coverage and understanding the limitations of the CG 20 10 07 04 Liability Endorsement.

Filling out and using the CG 20 10 07 04 Liability Endorsement form is an important task for businesses looking to secure their interests while working with other entities. Here are key points to keep in mind:

Following these takeaways will ensure effective use of the CG 20 10 07 04 Liability Endorsement form. Keeping everything clear and well-documented can help mitigate risks and protect against potential liabilities.

Pdf Puppy Health Guarantee Template - The Breeder guarantees a healthy puppy based on breeding practices.

Blank Invoice Template Word - Supports various currencies for international invoicing.