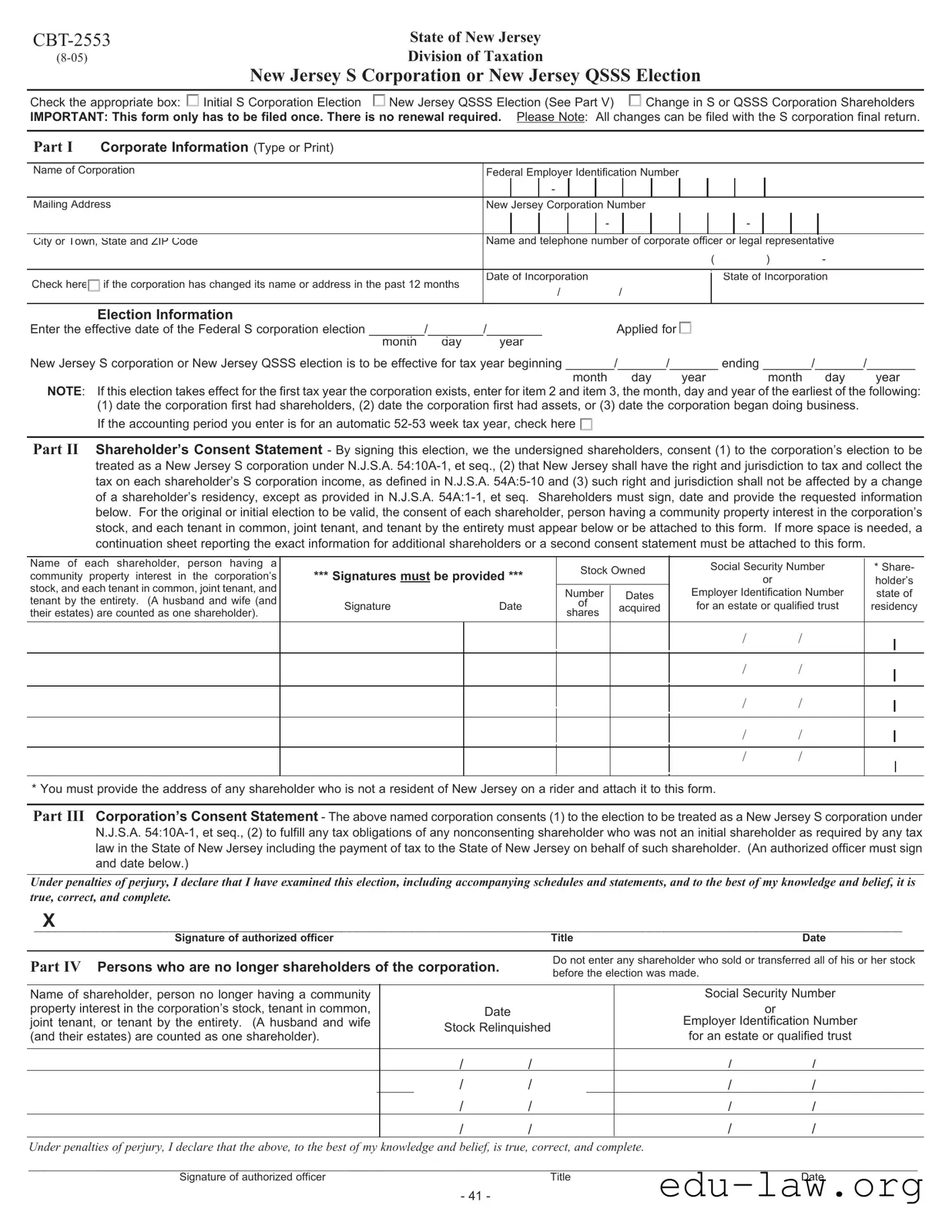

The CBT-2553 form is an essential document for corporations operating in New Jersey that wish to elect to be treated as S corporations or Qualified Subchapter S Subsidiaries (QSSS). This form must be completed accurately to ensure compliance with state tax regulations. It serves multiple purposes, including the initial election to become a New Jersey S corporation, reporting changes in shareholders, and electing QSSS status. Corporations must provide detailed corporate information, including their name, federal employer identification number, and the effective dates for the elections. Additionally, the form requires consent from all shareholders, ensuring that they agree to the corporation's tax obligations under New Jersey law. Importantly, the CBT-2553 only needs to be filed once, eliminating the need for annual renewals. The process also includes sections for corporate officers to affirm the accuracy of the information provided, as well as provisions for shareholders who are no longer part of the corporation. Understanding the nuances of this form is crucial for corporations aiming to navigate New Jersey's tax landscape effectively.

|

|

|

State of New Jersey |

|

|

|

|

|

|

Division of Taxation |

|

|

|

|

|

New Jersey S Corporation or New Jersey QSSS Election |

||||

|

|

|

|

|

|

|

Check the appropriate box: |

|

Initial S Corporation Election |

|

New Jersey QSSS Election (See Part V) |

|

Change in S or QSSS Corporation Shareholders |

|

|

|

||||

IMPORTANT: This form only has to be filed once. There is no renewal required. Please Note: All changes can be filed with the S corporation final return.

Part I |

Corporate Information (Type or Print) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Name of Corporation |

|

Federal Employer Identification Number |

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Address |

|

New Jersey Corporation Number |

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

- |

|

|

|

|

|

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

City or Town, State and ZIP Code |

|

Name and telephone number of corporate officer or legal representative |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

( |

) |

- |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Check here |

|

|

if the corporation has changed its name or address in the past 12 months |

Date of Incorporation |

|

|

|

|

|

|

State of Incorporation |

|||||||||

|

|

|

|

|

|

|

|

|||||||||||||

|

|

/ |

|

|

/ |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Election Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter the effective date of the Federal S corporation election ________/________/________ |

Applied for |

|

|

|

|

|

|

|

||||||||||||

|

|

|

month |

day |

year |

|

|

|

|

|

|

|

|

|

|

|

||||

New Jersey S corporation or New Jersey QSSS election is to be effective for tax year beginning _______/_______/_______ ending _______/_______/_______

month day year month day year

NOTE: If this election takes effect for the first tax year the corporation exists, enter for item 2 and item 3, the month, day and year of the earliest of the following:

(1)date the corporation first had shareholders, (2) date the corporation first had assets, or (3) date the corporation began doing business. If the accounting period you enter is for an automatic

Part II Shareholder’s Consent Statement - By signing this election, we the undersigned shareholders, consent (1) to the corporation’s election to be treated as a New Jersey S corporation under N.J.S.A.

Name of each shareholder, person having a |

|

|

Stock Owned |

Social Security Number |

* Share- |

||||

community property interest in the corporation’s |

*** Signatures must be provided *** |

||||||||

or |

|

holder’s |

|||||||

|

|

|

|||||||

stock, and each tenant in common, joint tenant, and |

|

|

Number |

Dates |

Employer Identification Number |

state of |

|||

tenant by the entirety. (A husband and wife (and |

|

|

|||||||

Signature |

Date |

of |

acquired |

for an estate or qualified trust |

residency |

||||

their estates) are counted as one shareholder). |

|||||||||

|

|

shares |

|

|

|

|

|

||

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* You must provide the address of any shareholder who is not a resident of New Jersey on a rider and attach it to this form.

Part III Corporation’s Consent Statement - The above named corporation consents (1) to the election to be treated as a New Jersey S corporation under N.J.S.A.

Under penalties of perjury, I declare that I have examined this election, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete.

____________________________________________________________________________________________________________________________X

Signature of authorized officer |

Title |

Date |

Part IV Persons who are no longer shareholders of the corporation.

Do not enter any shareholder who sold or transferred all of his or her stock before the election was made.

Name of shareholder, person no longer having a community |

|

|

Social Security Number |

||

property interest in the corporation’s stock, tenant in common, |

|

Date |

|

or |

|

joint tenant, or tenant by the entirety. (A husband and wife |

Stock Relinquished |

Employer Identification Number |

|||

(and their estates) are counted as one shareholder). |

for an estate or qualified trust |

||||

|

|

||||

|

|

|

|

|

|

|

/ |

/ |

/ |

/ |

|

|

/ |

/ |

/ |

/ |

|

|

/ |

/ |

/ |

/ |

|

|

/ |

/ |

/ |

/ |

|

Under penalties of perjury, I declare that the above, to the best of my knowledge and belief, is true, correct, and complete.

_______________________________________________________________________________________________________________________________

Signature of authorized officer |

Title |

Date |

- 41 -

PART V Qualified Subchapter S Subsidiary Election

Corporation’s Consent Statement - The above named corporation consents (1) to the election to be treated as a “New Jersey Qualified Subchapter S Subsidiary”, and (2) to file a

Under penalties of perjury, I declare that I have examined this election, and to the best of my knowledge and belief, it is true, correct, and complete.

__________________________________________________________________________________________________________________

Signature of authorized officer |

Title |

Date |

Corporate Parent Company’s Consent Statement - By signing this election, the undersigned corporation consents (1) to the subsidiary’s elec- tion to be treated as a “New Jersey Qualified Subchapter S Subsidiary” and (2) to taxation by New Jersey by filing a

Corporate Parent Name

Address

FID Number

Under penalties of perjury, I declare that I have examined this election, and to the best of my knowledge and belief, it is true, correct, and complete.

_______________________________________________________________________________________________________________________________________________

Signature of authorized officer |

Title |

Date |

INSTRUCTIONS FOR FORM

1.Purpose - A corporation must file form

2.Who may elect - A corporation may make the election to be treat- ed as a New Jersey S corporation only if it meets all of the follow- ing criteria:

a)The corporation is or will be an S corporation pursuant to section 1361 of the Federal Internal Revenue Code;

b)Each shareholder of the corporation consents to the election and the jurisdictional requirements as detailed in Part II of this form;

c)The corporation consents to the election and the assumption of any tax liabilities of any nonconsenting shareholder who was not an initial shareholder as indicated in Part III of this form.

3.Where to file - Mail form

4.When to make the election - The completed form

5.Acceptance or

ed within 30 days after the filing of the

6.End of election - Generally, once an election is made, a corpora- tion remains a New Jersey S corporation as long as it is a Federal S corporation. There is a limited opportunity to revoke an election only during the first tax year to which an election would otherwise apply. To revoke an election, a letter of revocation signed by

shareholders holding more than 50% of the outstanding shares of stock on the day of revocation should be mailed to the address in instruction 3 on or before the last day of the first tax year to which the election would otherwise apply. A copy of the original election should accompany the letter of revocation. Such a revocation will render the original election null and void from inception.

7.Initial election - Complete Parts I, II and III in their entirety for an initial New Jersey S Corporation election. Each shareholder who owns (or is deemed to own) stock at the time the election is made, must consent to the election. A list providing the social security number and the address of any shareholder who is not a New Jersey resident must be attached when filing this form.

8.Reporting shareholders who were not initial shareholders - Complete Parts I, II and III when filing this form to report any new shareholder. A new shareholder is a shareholder who, prior to the acquisition of stock, did not own any shares of stock in the S cor- poration, but who acquired stock (either existing shares or shares issued at a later date) subsequent to the initial New Jersey S cor- poration election. If a new shareholder fails to sign a consent statement, the corporation is obligated to fulfill the tax require- ments as stated in Part III on behalf of the nonconsenting share- holder. An existing shareholder whose percentage of stock own- ership changes is not considered a new shareholder. If the tax- payer previously had elected to be treated as a New Jersey QSSS, the new shareholder must also complete Part V.

9.Part IV should only be completed for any person who is no longer a shareholder of the corporation. You do not have to enter any shareholder who sold or transferred all of his or her stock before the election was made. All changes can be filed with the S corpo- ration final return.

10.Part V must be completed in order to permit a New Jersey S Corporation to be treated as a New Jersey Qualified Subchapter S Subsidiary and remit only a minimum tax. In addition, the parent company also must consent to filing and remitting New Jersey Corporation Business Tax which would include the assets, liabili- ties, income and expenses of its QSSS along with its own. Failure of the parent either to consent or file a

- 42 -

Mail to: |

|

PO Box 252 |

|

|

Trenton, NJ |

|

(609) |

State of New Jersey

Division of Taxation

New Jersey S Corporation Certification

This certification is for use by unauthorized foreign

Part I. Corporate Information (Type or Print)

Name of Corporation: ____________________________________________________

Federal Employer Identification Number: ______ - _____________________________

Part II. Corporate Attestation

By signing this statement, the corporation affirms that the corporation has not conducted any activi- ties within this state that would require the Corporation to file a Certificate of Authority in accordance with N.J.S.A.

Print the name and title of the person executing this document on behalf of the Corporation. This person must be a corporate officer.

Name: ________________________________ |

Title: ___________________________ |

Signature: _____________________________ |

Date: ___________________________ |

- 43 -

Instructions for Form

1.This form is to be used by

2.Name of Corporation: Type or print name exactly as it appears on form

3.Federal Employer Identification Number (FEIN): Please enter the Federal Identification Number assigned by the Internal Revenue Service.

4.Please read the Corporate Attestation and the cited statutes for compliance.

5.Print the name and title of the corporate officer signing this document and the

6.Mail the completed forms to: New Jersey Division of Revenue, PO Box 252 Trenton, NJ

(1)No foreign corporation shall have the right to transact business in this State until it shall have procured a certificate of authority so to do from the Secretary of State. A foreign corporation may be authorized to do in this State any business which may be done lawfully in this State

by a domestic corporation, to the extent that it is authorized to do such business in the jurisdiction of its incorporation, but no other business.

(2)Without excluding other activities which may not constitute transacting business in this State, a foreign corporation shall not be considered to be transacting business in this State, for the purposes of this act, by reason of carrying on in this State any one or more of the following activities

(a)maintaining, defending or otherwise participating in any action or proceeding, whether judicial, administrative, arbitrative or otherwise, or effecting the settlement thereof or the settlement of claims or disputes;

(b)holding meetings of its directors or shareholders;

(c)maintaining bank accounts or borrowing money, with or without security, even if such borrow- ings are repeated and continuous transactions and even if such security has a situs in this State;

(d)maintaining offices or agencies for the transfer, exchange and registration of its securities, or appointing and maintaining trustees or depositaries with relation to its securities.

(3)The specification in subsection

- 44 -

| Fact Name | Description |

|---|---|

| Purpose of Form | The CBT-2553 form is used by corporations in New Jersey to elect S corporation status or to report changes in shareholders. |

| Filing Frequency | This form only needs to be filed once. There is no renewal required after the initial submission. |

| Governing Law | The election is governed by N.J.S.A. 54:10A-1, et seq., which outlines the requirements and procedures for S corporations in New Jersey. |

| Filing Deadline | The completed form must be filed within one calendar month of the time a Federal S corporation election is required. |

| Shareholder Consent | All shareholders must consent to the election for it to be valid. Their signatures are required on the form. |

Filling out the CBT-2553 form is a crucial step for corporations in New Jersey looking to elect S corporation status. This form must be completed accurately to ensure compliance with state tax regulations. Once the form is filled out, it should be submitted to the New Jersey Division of Revenue for processing.

What is the purpose of the CBT-2553 form?

The CBT-2553 form is used by corporations in New Jersey to elect to be treated as a New Jersey S corporation or a New Jersey Qualified Subchapter S Subsidiary (QSSS). It is also utilized to report any changes in shareholders. This election is crucial for tax purposes, as it determines how the corporation will be taxed at both the state and federal levels.

Who is eligible to file the CBT-2553 form?

A corporation can file the CBT-2553 form if it meets specific criteria. It must be or will be an S corporation under federal law. Additionally, all shareholders must consent to the election, and the corporation must agree to assume tax liabilities for any nonconsenting shareholders who were not initial shareholders. These requirements ensure that all parties involved are aware and agree to the tax implications of the election.

When should the CBT-2553 form be filed?

The completed CBT-2553 form should be filed within one calendar month of the time a federal S corporation election would be required. Specifically, it must be submitted before the 16th day of the fourth month of the first tax year the election is to take effect. If the election is made after this deadline, it will apply to the following tax year.

What happens after the CBT-2553 form is submitted?

Once the CBT-2553 form is filed, the New Jersey Division of Revenue will notify the corporation within 30 days regarding the acceptance or non-acceptance of the election. If no notification is received within this timeframe, it is advisable to contact the Division of Revenue for clarification.

Can the election be revoked after it has been made?

Yes, the election can be revoked, but only during the first tax year it applies to. To revoke the election, a letter signed by shareholders holding more than 50% of the outstanding shares must be sent to the Division of Revenue. This letter should include a copy of the original election and must be mailed before the last day of the first tax year to which the election applies.

What additional information must be provided for non-resident shareholders?

If any shareholder is not a resident of New Jersey, their address must be included on a separate rider attached to the CBT-2553 form. This ensures that the state has accurate information for tax purposes and can appropriately manage any tax obligations related to non-resident shareholders.

Incomplete Information: Failing to fill out all required fields can lead to delays. Ensure that the corporation name, Federal Employer Identification Number (FEIN), and mailing address are complete and accurate.

Incorrect Effective Dates: Entering the wrong effective date for the S corporation election can cause significant tax implications. Double-check that the date aligns with the corporation's tax year.

Missing Shareholder Consent: Each shareholder must consent to the election. Omitting a signature or failing to provide the necessary information for each shareholder can invalidate the election.

Neglecting Non-Resident Shareholder Addresses: If any shareholders are not residents of New Jersey, their addresses must be attached as a rider. Failing to do so can lead to complications.

Improper Filing of Part IV: Part IV should only include shareholders who are no longer part of the corporation. Including current shareholders or those who sold their shares after the election can create confusion.

Ignoring Filing Deadlines: The form must be filed within specific timeframes. Missing the deadline can result in the election being treated as made for the next year.

Failure to Attach Required Documentation: Any additional sheets or documents, such as a continuation sheet for extra shareholders, must be included. Omitting these can lead to rejection of the application.

When completing the CBT-2553 form for New Jersey S Corporation status, several other documents may be necessary to ensure compliance and proper processing. Here is a list of important forms and documents often used alongside the CBT-2553:

Gathering these documents can streamline the process and help ensure that your application is processed without delays. Each form serves a specific purpose and is essential for compliance with New Jersey's tax regulations.

The CBT-2553 form is similar to the IRS Form 2553, which is used for federal tax purposes. Both forms allow a corporation to elect S corporation status, enabling it to be taxed as a pass-through entity. This means that the corporation's income is reported on the shareholders' personal tax returns, avoiding double taxation. Just like the CBT-2553, the IRS Form 2553 requires consent from all shareholders to validate the election. The timing for filing is also crucial; both forms must be submitted within specific deadlines to ensure the election is effective for the desired tax year.

Another document similar to the CBT-2553 is the New Jersey CBT-100 form, which is the corporate business tax return for corporations operating in New Jersey. While the CBT-2553 is focused on electing S corporation status, the CBT-100 is used to report income, deductions, and tax liabilities. Both forms require accurate corporate information and details about shareholders. The CBT-100 ultimately reflects the tax obligations that arise from the election made on the CBT-2553, highlighting the interconnectedness of these documents in the tax process.

The IRS Form 1120S is another related document, as it is the tax return filed by S corporations at the federal level. Similar to the CBT-2553, the Form 1120S is used by S corporations to report income, deductions, and credits. Both forms require detailed information about the corporation and its shareholders. While the CBT-2553 is about making the election, the Form 1120S is about reporting the financial results of that election. This shows how the election process leads to ongoing reporting requirements for S corporations.

Lastly, the New Jersey CBT-100S form is specifically designed for S corporations to report their business income and pay the minimum tax. Like the CBT-2553, the CBT-100S is tailored for S corporations and includes provisions for shareholder information. Both forms emphasize the importance of shareholder consent and compliance with New Jersey tax laws. The CBT-100S serves as a follow-up to the CBT-2553, allowing S corporations to fulfill their tax obligations after the election has been made.

When filling out the CBT-2553 form, there are important guidelines to follow. Adhering to these can help ensure that the process goes smoothly.

This is incorrect. The CBT-2553 form only needs to be filed once for the initial election. There is no renewal required.

In reality, any corporation that meets the requirements to be treated as an S corporation can file this form, regardless of its type.

This is not true. Non-resident shareholders can be included, but their addresses must be provided on a separate rider attached to the form.

This is misleading. The form must be filed within one calendar month of the time a Federal S corporation election would be required.

Acceptance is not guaranteed. The Division of Revenue will notify the corporation of acceptance or non-acceptance within 30 days after filing.

This is incorrect. A corporation can revoke its S corporation status during the first tax year by submitting a letter of revocation signed by shareholders holding more than 50% of the outstanding shares.

In addition to initial elections, this form is also used to report changes in shareholders. It serves multiple purposes related to S corporation status.

Filling out and using the CBT-2553 form is a crucial step for corporations in New Jersey wishing to elect S corporation status. Here are some key takeaways to consider: