In California, a Promissory Note serves as a crucial financial document, primarily used to outline a borrower’s commitment to repay a loan under specified terms. This form captures essential details such as the principal amount, interest rate, payment schedule, and duration of repayment, creating a clear roadmap for both lenders and borrowers. A Promissory Note can be secured or unsecured, impacting how the lender may recover their funds in the event of default. The language used in the document is designed to protect the interests of both parties, establishing rights and obligations while also providing a legally binding framework for the transaction. Beyond the basics, additional clauses might cover late payment penalties, prepayment options, and governing law, ensuring that the agreement is tailored to the unique circumstances of the loan. Understanding this form and its implications is vital for anyone engaging in lending or borrowing money in California, as it lays the foundation for the financial relationship and clarifies expectations from the outset.

California Promissory Note Template

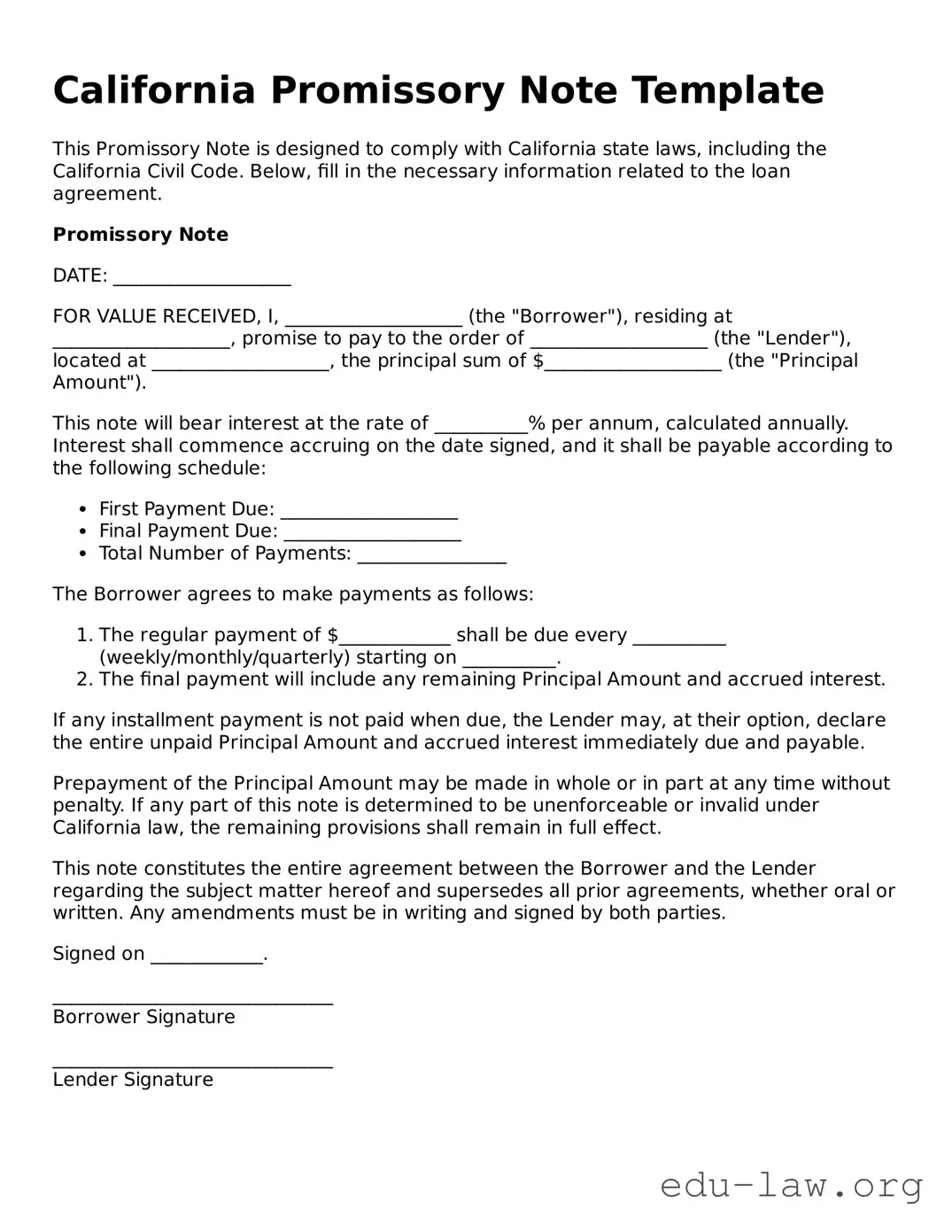

This Promissory Note is designed to comply with California state laws, including the California Civil Code. Below, fill in the necessary information related to the loan agreement.

Promissory Note

DATE: ___________________

FOR VALUE RECEIVED, I, ___________________ (the "Borrower"), residing at ___________________, promise to pay to the order of ___________________ (the "Lender"), located at ___________________, the principal sum of $___________________ (the "Principal Amount").

This note will bear interest at the rate of __________% per annum, calculated annually. Interest shall commence accruing on the date signed, and it shall be payable according to the following schedule:

The Borrower agrees to make payments as follows:

If any installment payment is not paid when due, the Lender may, at their option, declare the entire unpaid Principal Amount and accrued interest immediately due and payable.

Prepayment of the Principal Amount may be made in whole or in part at any time without penalty. If any part of this note is determined to be unenforceable or invalid under California law, the remaining provisions shall remain in full effect.

This note constitutes the entire agreement between the Borrower and the Lender regarding the subject matter hereof and supersedes all prior agreements, whether oral or written. Any amendments must be in writing and signed by both parties.

Signed on ____________.

______________________________

Borrower Signature

______________________________

Lender Signature

| Fact Name | Details |

|---|---|

| Definition | A California Promissory Note is a legal document where one person promises to pay a specific amount of money to another party under agreed terms. |

| Governing Law | This form is governed by the California Civil Code, particularly Sections 3300 and 3310, which outline rules for promissory notes. |

| Essential Elements | A valid promissory note must include the borrower’s name, lender’s name, the amount borrowed, interest rate, repayment terms, and signatures. |

| Interest Rates | California allows for various interest rates on promissory notes, but there are legal limits to the amount that can be charged. |

| Enforceability | To be enforceable, the note must be written, signed, and have clear repayment terms to avoid disputes. |

| Default Consequences | If the borrower fails to pay as agreed, the lender may take legal action to recover the owed amount. |

| Transferability | Promissory notes can be sold or transferred to another party, provided that the original terms remain unchanged. |

| Use Cases | They are commonly used for personal loans, business financing, and real estate transactions. |

Once you have the California Promissory Note form ready, it's time to fill it out with the necessary information. Completing this document requires attention to detail to ensure all requisite details are accurately captured.

After completing the form, both parties should retain a copy for their records. This ensures that each party has access to the agreed-upon terms in the future.

What is a California Promissory Note?

A California Promissory Note is a written agreement in which one party promises to pay a certain amount of money to another party at a specified time or on demand. It acts as a formal contract outlining the terms of the loan, including the principal amount, interest rate, repayment schedule, and any consequences for defaulting on the agreement.

Who can use a Promissory Note in California?

Anyone can use a Promissory Note in California, including individuals, businesses, and lenders. It is commonly used for personal loans, business transactions, and real estate financing. The parties involved must be legally capable of entering into a contract, which generally includes being of legal age and mentally competent.

What are the key elements that must be included in a California Promissory Note?

Essential elements of a Promissory Note include the names of the borrower and lender, the principal amount borrowed, the interest rate, repayment terms (including due dates), and any penalties for late payment. It may also specify the method of payment and whether the loan is secured by collateral.

Does a Promissory Note need to be notarized in California?

Notarization is not required for a Promissory Note to be legally binding in California. However, having the document notarized can lend credibility and provide a stronger evidentiary basis in case of disputes. It is advisable to consider notarization, especially for larger loans.

What happens if a borrower defaults on a Promissory Note?

If a borrower defaults, the lender has legal options to recover the owed amount. These options may include demanding immediate repayment, initiating collection efforts, or pursuing a lawsuit. The specific remedies available will depend on the terms outlined in the Promissory Note and applicable California laws.

Can a Promissory Note be modified after it has been signed?

Yes, a Promissory Note can be modified if both parties agree to the changes. This typically requires drafting an amendment or a new note to reflect the updated terms. Changes should be documented in writing to prevent future disagreements.

Is a Promissory Note legally enforceable in California?

Yes, a properly executed Promissory Note is legally enforceable in California. As long as it meets the necessary legal requirements, it can be used in court to pursue repayment. Both parties must adhere to the terms as outlined in the document to avoid legal complications.

Neglecting to include the borrower’s full legal name.

Forgetting to clearly state the loan amount, which can lead to confusion later on.

Failing to specify the interest rate, if applicable, can create misunderstandings about repayment terms.

Not including the repayment schedule, which is crucial for outlining how and when payments are due.

Leaving out details regarding late fees or penalties for missed payments can have financial implications.

Overlooking the date of the agreement can cause complications in tracking the duration of the loan.

Failing to sign and date the document properly may render it unenforceable.

Not including the lender’s information can lead to disputes about who is owed the money.

Using vague language in the repayment terms can cause misunderstandings and disputes.

Neglecting to have witnesses or a notary sign the document, if required, can impact its validity.

When engaging in lending or borrowing activities, especially in California, a Promissory Note is a key document that formalizes the terms of the loan. However, there are other important documents that often accompany a Promissory Note to ensure clarity and legal protection for all parties involved. Below is a brief overview of these common documents.

Understanding these documents can enhance both the borrower’s and lender’s experiences throughout the lending process. Each plays a vital role in ensuring transparency and protecting the rights and obligations of all parties involved, ultimately fostering a smoother financial interaction.

The California Promissory Note form shares similarities with a Mortgage. Both documents outline an agreement where one party borrows money while another party lends it. A mortgage serves as security for the promissory note, typically detailing the terms of the loan and the collateral involved (the property). While a promissory note is focused on the borrower’s commitment to repay, the mortgage provides a mechanism for the lender to reclaim the loaned amount through property if the borrower defaults.

A Loan Agreement is another document that bears resemblance to the California Promissory Note. While both serve as written records of a loan, a Loan Agreement generally offers a more comprehensive framework, detailing repayment schedules, interest rates, and specific borrower and lender obligations. It can encompass various types of loans, including business loans or personal loans, whereas the promissory note is more tailored to the straightforward promise to repay a set amount.

The Conditional Sale Agreement also aligns with the concept of a promissory note. This document pertains to an agreement for the sale of goods with a condition that allows the seller to reclaim ownership until the buyer fully pays for the item. Like a promissory note, it encapsulates a financial obligation. However, it differs in that it specifically connects to the sale of a tangible asset as opposed to a loan for cash.

A Secured Loan Agreement is similar in that it involves a borrower obtaining money backed by collateral. Both documents outline the borrower’s promise to repay a loan, yet a secured loan agreement usually identifies the asset pledged in case of default, making the lender's claim stronger. The promissory note, while indicating repayment responsibility, might not provide the same level of detail regarding collateralization.

An Installment Sale Agreement bears notable resemblance to a promissory note as well. In this arrangement, the seller allows the buyer to pay for a purchased item over time through scheduled payments. Like a promissory note, it formalizes the borrower’s commitment to repay. The distinction lies in the fact that the ownership of the purchased item may be retained by the seller until full payment is made, adding a layer of complexity not always present with a standard promissory note.

A Credit Agreement parallels the California Promissory Note in its establishment of terms for borrowed funds. This document usually involves lines of credit or revolving credit, providing more flexibility in how and when funds are accessed. While both require the borrower’s promise to repay, credit agreements tend to elaborate on specific repayment terms, fees, and interest calculations over time.

Finally, a Business Loan Agreement resembles the California Promissory Note in the context of financing. This document typically includes terms related to loans specifically provided for business purposes, detailing repayment terms, interest rates, consequences of default, and more. Both documents serve similar functions regarding the obligation to repay, but the business loan agreement often includes additional clauses tailored to business needs and the unique risks involved in commercial lending.

When filling out the California Promissory Note form, it is essential to follow specific guidelines to ensure accuracy and compliance. The following list outlines seven important dos and don'ts:

Here are ten common misconceptions about the California Promissory Note form. Understanding these can help clarify its purpose and functionality.

Create a Promissory Note - The lender may enforce the note through legal action if payments are missed.

Promissory Note Template Florida Pdf - Protects both parties by ensuring clarity in the repayment process.

Promissory Note Georgia - This document fosters trust between a borrower and lender by clearly stating expectations.

Texas Promissory Note Requirements - If a borrower defaults, the lender may have the right to take legal action to recover the funds.