The Additional Insured form is a crucial document in the realm of commercial general liability insurance, specifically designed to extend coverage to third parties, such as owners, lessees, or contractors, involved in completed operations. This endorsement modifies the existing insurance policy, ensuring that certain individuals or organizations are protected against liability for bodily injury or property damage that may arise from the work done by the insured party. It's important to note that the coverage is limited to the specific operations listed in the form and only applies to the extent permitted by law. Additionally, if the coverage is stipulated in a contract, it cannot exceed what is required by that agreement. The form also clarifies that the insurance limits for additional insureds are capped at either the amount specified in the contract or the maximum available under the policy's existing limits, whichever is lower. This careful balance ensures that while additional parties receive necessary protection, the insured party's coverage limits remain intact. Understanding the nuances of this form is essential for anyone involved in contracts or agreements that require additional insured status, as it shapes the responsibilities and protections afforded to all parties involved.

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 37 04 13 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR CONTRACTORS – COMPLETED OPERATIONS

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

PRODUCTS/COMPLETED OPERATIONS LIABILITY COVERAGE PART

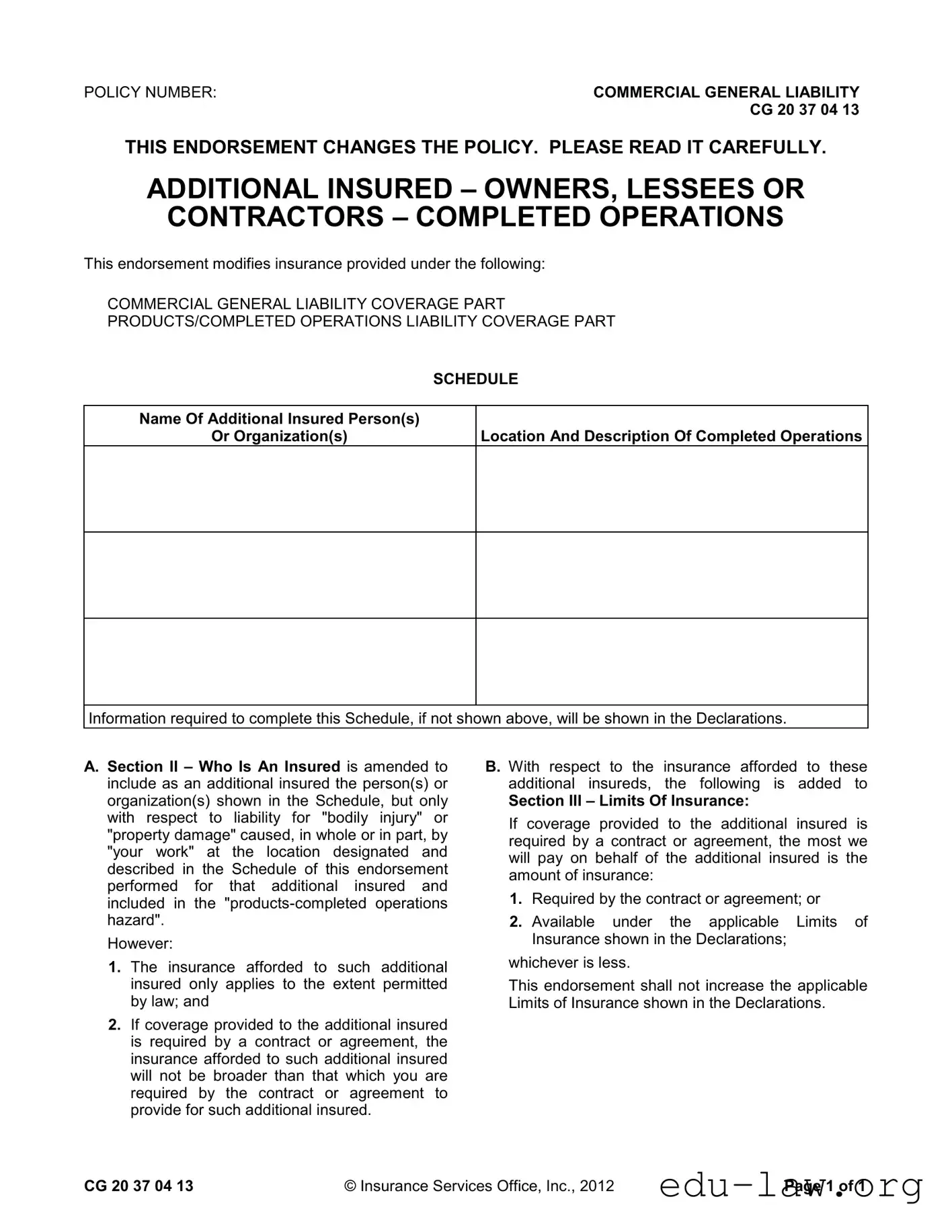

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location And Description Of Completed Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A.Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury" or "property damage" caused, in whole or in part, by "your work" at the location designated and described in the Schedule of this endorsement performed for that additional insured and included in the

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable Limits of Insurance shown in the Declarations;

whichever is less.

This endorsement shall not increase the applicable Limits of Insurance shown in the Declarations.

CG 20 37 04 13 |

© Insurance Services Office, Inc., 2012 |

Page 1 of 1 |

| Fact Name | Description |

|---|---|

| Policy Number | The form is identified by the policy number CG 20 37 04 13. |

| Purpose | This endorsement provides additional insured status to owners, lessees, or contractors for completed operations. |

| Coverage Modification | The endorsement modifies the coverage provided under the Commercial General Liability policy. |

| Liability Scope | It covers liability for bodily injury or property damage caused by the named insured's work. |

| Contractual Limitations | The coverage for additional insureds is limited to what is required by contract. |

| Insurance Limits | The maximum amount payable is the lesser of the contract requirement or the limits stated in the policy. |

| State-Specific Forms | Governing laws for additional insured forms vary by state; always check local regulations. |

Completing the Additional Insured form is a crucial step in ensuring that all parties are adequately covered under your insurance policy. This process requires careful attention to detail to avoid any issues later on. Follow these steps to fill out the form correctly.

Once the form is filled out, submit it to your insurance provider as soon as possible. This ensures that the additional insured status is recognized and that coverage is effective without delay. Prompt action will help safeguard all parties involved.

What is an Additional Insured form?

An Additional Insured form is a document that allows a third party, such as a property owner or contractor, to be covered under another party's insurance policy. This form is often used in situations where one party performs work for another and helps protect the additional insured from liability related to that work.

Who qualifies as an Additional Insured?

An Additional Insured can be any person or organization specified in the endorsement. Typically, this includes owners, lessees, or contractors who may be exposed to liability due to the work performed by the insured party. The specific names and details should be included in the form.

What does the Additional Insured coverage protect against?

This coverage protects against liability for bodily injury or property damage that occurs as a result of the work performed for the additional insured. It only applies if the injury or damage is related to the completed operations of the insured party at the specified location.

Does the Additional Insured coverage apply to all claims?

No, the coverage is limited. It applies only to claims that arise from the insured's work as described in the endorsement. Additionally, the coverage is subject to the laws of the state and any specific contractual agreements in place.

How does the contract affect the Additional Insured coverage?

If the coverage for the additional insured is required by a contract, the insurance provided cannot be broader than what the contract specifies. This means that the terms of the contract dictate the extent of the coverage offered.

What are the limits of insurance for Additional Insureds?

The limits of insurance for Additional Insureds are capped at either the amount specified in the contract or the limits shown in the policy's Declarations, whichever is less. This means that the additional insured will not receive more coverage than what is required or available under the policy.

Can the limits of insurance be increased for Additional Insureds?

No, the endorsement does not increase the overall limits of insurance provided in the policy. The limits remain as stated in the Declarations and are not affected by adding additional insureds.

What should be included in the Additional Insured form?

The form should include the names of the additional insured individuals or organizations, along with the location and description of the completed operations. Any additional information required should be clearly stated in the Declarations.

Is the Additional Insured coverage valid indefinitely?

The coverage is not indefinite. It is only valid for the duration of the policy and is specific to the work performed as described in the endorsement. Once the work is completed, the coverage may no longer apply unless otherwise specified in the contract.

How can I obtain an Additional Insured form?

Failing to include the correct policy number. Always double-check that the policy number matches the one on your insurance documents.

Not specifying the name of the additional insured accurately. Ensure that the names are spelled correctly and match the legal documents.

Leaving out the location and description of completed operations. This information is crucial for clarity and to avoid potential disputes.

Misunderstanding the scope of coverage. Make sure you know what liabilities are covered and that they align with your contract requirements.

Assuming that the coverage is automatic. Always confirm that the additional insured status is included in your policy.

Not reviewing the contract or agreement requirements thoroughly. The coverage provided cannot exceed what is stipulated in the contract.

Overlooking the limits of insurance section. Understand the maximum amount that will be paid out for claims related to the additional insured.

Using outdated forms. Always ensure you are using the most current version of the Additional Insured form to avoid compliance issues.

Failing to get signatures or approvals when necessary. Make sure all required parties sign off on the form to validate the coverage.

The Additional Insured form is an important document in the realm of liability insurance, particularly for those involved in construction and contracting. However, it is often accompanied by other forms and documents that serve various purposes in the insurance landscape. Below is a list of commonly used documents alongside the Additional Insured form.

Understanding these documents can help stakeholders navigate the complexities of insurance requirements and ensure adequate protection against potential liabilities. Each form plays a crucial role in establishing clear responsibilities and coverage, ultimately fostering a safer and more accountable working environment.

The Additional Insured form shares similarities with the Waiver of Subrogation document. Both documents are often included in contracts to protect parties from liability. The Waiver of Subrogation prevents an insurer from seeking recovery from a third party after a loss has been paid. Similarly, the Additional Insured form extends coverage to another party, ensuring they are protected against claims related to the insured's work. Both documents enhance risk management strategies in contractual relationships.

Another document comparable to the Additional Insured form is the Certificate of Insurance. This certificate provides proof of insurance coverage to third parties. While the Additional Insured form actually modifies the insurance policy to include additional parties, the Certificate of Insurance simply verifies that coverage exists. Both documents are essential in demonstrating compliance with contractual insurance requirements and ensuring that all parties are aware of the coverage in place.

The Indemnity Agreement also aligns closely with the Additional Insured form. Indemnity Agreements are designed to shift liability from one party to another. They often require one party to compensate the other for certain losses. In contrast, the Additional Insured form provides insurance coverage directly, but both serve to protect parties in a contractual relationship from potential claims arising from their interactions.

The Primary and Non-Contributory Endorsement is another document that bears resemblance to the Additional Insured form. This endorsement establishes that the insurance policy will respond first in the event of a claim, protecting the additional insured party. The Additional Insured form also ensures that coverage is available to third parties, which helps clarify the responsibilities of each party involved in a contract. Both documents are crucial for delineating insurance obligations and responsibilities.

Additionally, the Additional Insured form is similar to the Additional Coverage Endorsement. This document expands the coverage provided by an insurance policy. Like the Additional Insured form, it modifies the existing policy to include new protections. While the Additional Coverage Endorsement may add new risks or exposures, the Additional Insured form specifically adds protection for other parties, ensuring they are covered for claims related to the insured's operations.

The Contractual Liability Endorsement is also akin to the Additional Insured form. This endorsement provides coverage for liabilities assumed under a contract. It ensures that the insurer will cover certain liabilities that arise from contractual obligations. Similarly, the Additional Insured form extends coverage to third parties based on contractual agreements, thereby enhancing protection for all involved parties.

The Completed Operations Coverage is another document that parallels the Additional Insured form. This coverage protects against claims arising from work that has been completed. The Additional Insured form specifically addresses liability for completed operations performed for the additional insured. Both documents ensure that parties are protected against potential claims related to their work, reinforcing the importance of coverage in project completion.

Finally, the Professional Liability Insurance form shares similarities with the Additional Insured form. While Professional Liability Insurance focuses on claims arising from professional services, it can also include additional insured provisions. Both documents serve to protect parties from claims related to their professional activities or work, ensuring that all parties are adequately covered in the event of a dispute.

When filling out the Additional Insured form, there are several important considerations to keep in mind. Here is a list of things you should and shouldn't do:

Misconception 1: Additional insured status provides unlimited coverage.

This is false. The coverage for an additional insured is limited to what is specified in the contract or agreement. It does not extend beyond those limits.

Misconception 2: All types of liability are covered under the additional insured endorsement.

This is incorrect. The endorsement only covers liability for bodily injury or property damage arising from the named insured's work, as specified in the endorsement.

Misconception 3: The additional insured endorsement is automatically included in every policy.

This is not true. The endorsement must be specifically added to the policy. It is not a standard feature in all commercial general liability policies.

Misconception 4: Additional insureds have the same rights as the primary insured.

This is misleading. Additional insureds have limited rights and protections, primarily tied to the scope of coverage defined in the endorsement.

Misconception 5: The additional insured endorsement covers all operations, regardless of location.

This is false. Coverage is only applicable to the specific location and operations described in the endorsement. If not listed, there is no coverage.

Misconception 6: The endorsement increases the overall policy limits.

This is incorrect. The endorsement does not increase the limits of insurance stated in the policy declarations. Coverage is subject to existing limits.

Misconception 7: Additional insureds can claim for any incident, regardless of the cause.

This is misleading. Claims must arise from the work of the primary insured as outlined in the endorsement. Other incidents may not be covered.

Misconception 8: The additional insured status lasts indefinitely.

This is not true. The status typically lasts only for the duration of the project or as specified in the contract. Once the work is completed, coverage may cease.

Misconception 9: Additional insured endorsements are the same across all insurance companies.

This is incorrect. Different insurers may have varying terms and conditions for their additional insured endorsements. Always review the specific language in your policy.

When filling out and using the Additional Insured form, it’s important to keep several key points in mind. Here are ten takeaways to consider:

By following these guidelines, you can effectively navigate the process of filling out and using the Additional Insured form, ensuring that all parties are adequately protected under the insurance policy.