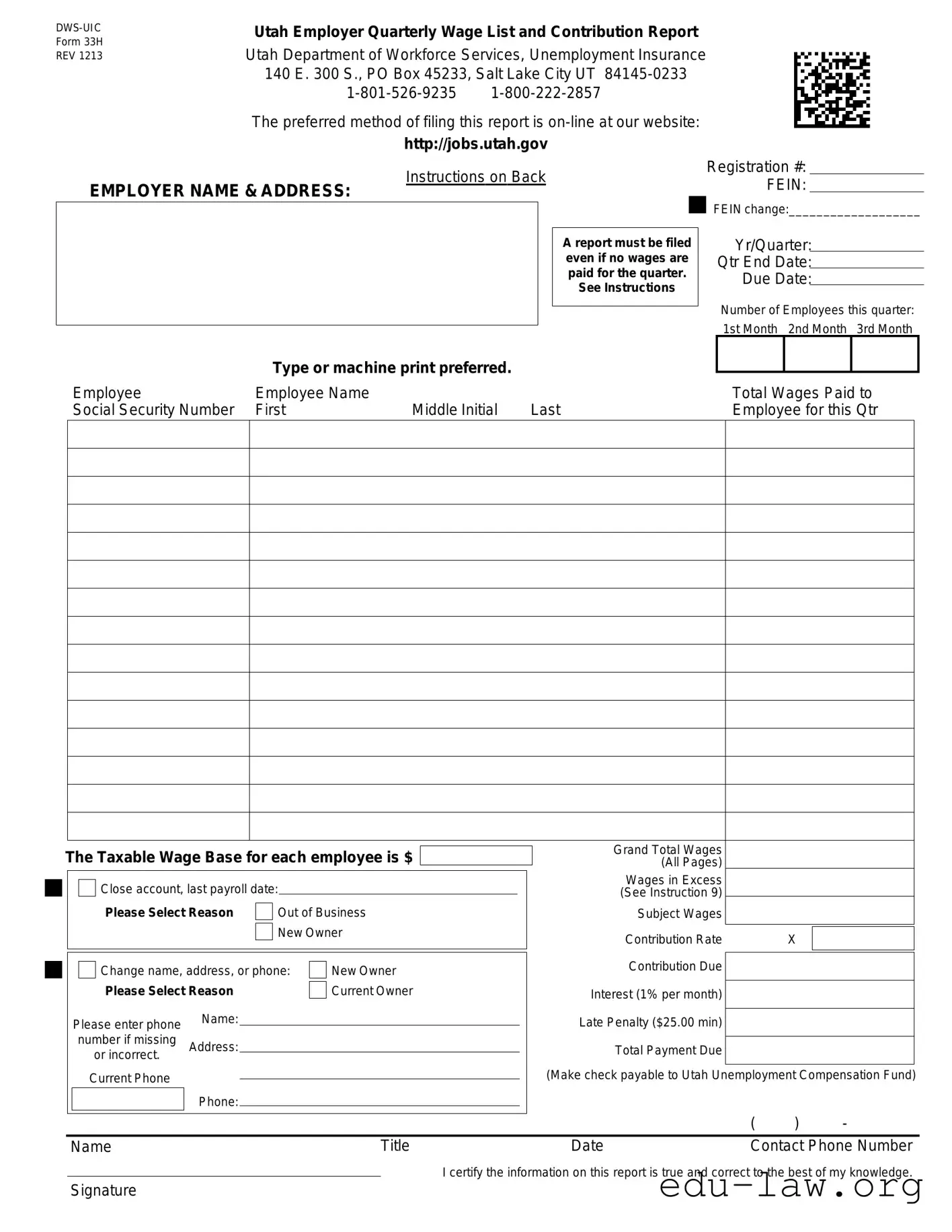

The 33H form is a crucial document for employers in Utah, serving as the Employer Quarterly Wage List and Contribution Report. This form is required by the Utah Department of Workforce Services and must be filed every quarter, even if no wages were paid during that period. Employers need to provide their name, address, and registration details, including the Federal Employer Identification Number (FEIN). The form captures essential information such as the total wages paid to each employee, their Social Security numbers, and the number of employees for the quarter. Additionally, employers must report taxable wages and calculate their contribution rate, which impacts their unemployment insurance obligations. If there are any changes, like a new owner or an address update, these must also be indicated. Filing can be done online, which is the preferred method, ensuring a streamlined process. Late submissions may incur penalties, so timely filing is important. Understanding the 33H form is key for employers to stay compliant and avoid potential fines.

Utah Employer Quarterly Wage List and Contribution Report

Form 33H |

Utah Department of Workforce Services, Unemployment Insurance |

||||||

REV 1213 |

|||||||

|

140 E. 300 S., PO Box 45233, Salt Lake City UT |

||||||

|

|

|

|||||

|

The preferred method of filing this report is |

||||||

|

http://jobs.utah.gov |

||||||

|

Instructions on Back |

||||||

EMPLOYER NAME & ADDRESS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A report must be filed |

|

|

|

|

|

|

|

even if no wages are |

|

|

|

|

|

|

|

paid for the quarter. |

|

|

|

|

|

|

|

See Instructions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Registration #:

FEIN:

FEIN change:___________________

Yr/Quarter:

Qtr End Date:

Due Date:

Number of Employees this quarter: 1st Month 2nd Month 3rd Month

Type or machine print preferred.

Employee |

Employee Name |

|

|

Total Wages Paid to |

Social Security Number |

First |

Middle Initial |

Last |

Employee for this Qtr |

|

|

|

|

|

|

|

|

|

|

The Taxable Wage Base for each employee is $

Close account, last payroll date:

|

|

Please Select Reason |

|

Out of Business |

||

|

|

|

|

New Owner |

||

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change name, address, or phone: |

|

New Owner |

||

|

|

|

||||

|

|

Please Select Reason |

|

|

|

Current Owner |

|

|

|

|

|

||

Please enter phone |

Name: |

|

|

||

number if missing |

Address: |

|

or incorrect. |

||

|

||

Current Phone |

|

|

|

Phone: |

Grand Total Wages

(All Pages)

Wages in Excess

(See Instruction 9)

Subject Wages

Contribution RateX

Contribution Due

Interest (1% per month)

Late Penalty ($25.00 min)

Total Payment Due (Make check payable to Utah Unemployment Compensation Fund)

|

|

|

( |

) |

- |

Name |

Title |

Date |

Contact Phone Number |

||

I certify the information on this report is true and correct to the best of my knowledge.

Signature

Form 33HA

REV 0813

Utah Employer Quarterly Wage List Continuation Sheet

Utah Department of Workforce Services, Unemployment Insurance

140 E. 300 S., PO Box 45233, Salt Lake City UT

The preferred method of filing this report is

http://jobs.utah.gov

Registration #:

EMPLOYER NAME & ADDRESS:

Yr/Quarter:

Qtr End Date:

Due Date:

|

|

Type or machine print this report. |

|

|

Employee |

Employee Name |

|

Total Wages Paid to |

|

Social Security Number |

First |

Middle Initial |

Last |

Employee for this Qtr |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fact Name | Description |

|---|---|

| Form Title | DWS-UIC Utah Employer Quarterly Wage List and Contribution Report Form 33H |

| Governing Law | Utah Unemployment Insurance Act |

| Filing Requirement | A report must be filed even if no wages are paid during the quarter. |

| Preferred Filing Method | Online submission is preferred via the Utah Department of Workforce Services website. |

| Contact Information | Utah Department of Workforce Services, 140 E. 300 S., PO Box 45233, Salt Lake City UT 84145-0233 |

| Due Date | The due date for the report is specified on the form based on the quarter end date. |

| Certification Requirement | The employer must certify that the information provided is true and correct. |

Filling out the 33H form is a straightforward process that ensures your employer contributions are reported accurately. After completing the form, you will need to submit it according to the instructions provided, ensuring compliance with state regulations.

What is the purpose of the Form 33H?

The Form 33H, also known as the Utah Employer Quarterly Wage List and Contribution Report, is designed for employers in Utah to report wages paid to employees during a specific quarter. This form is crucial for ensuring compliance with unemployment insurance requirements. Even if no wages were paid during the quarter, employers must still file this report. The information collected helps the Utah Department of Workforce Services monitor and manage unemployment benefits effectively.

How do I file the Form 33H?

The preferred method for filing the Form 33H is online through the Utah Department of Workforce Services website. This online submission simplifies the process and can help prevent errors. However, if you prefer to submit a paper form, you can download it, complete it, and mail it to the address provided on the form. Be sure to check the due date for your specific quarter to avoid any late penalties.

What information is required on the Form 33H?

When completing the Form 33H, you will need to provide several pieces of information. This includes your employer name and address, registration number, and Federal Employer Identification Number (FEIN). You must also list each employee's name, Social Security number, and total wages paid for the quarter. Additionally, you will need to calculate the total wages, contribution rates, and any penalties or interest if applicable. This comprehensive data ensures accurate reporting and compliance with state regulations.

What happens if I miss the filing deadline for the Form 33H?

Failing to file the Form 33H by the due date can lead to penalties. A late penalty of at least $25 may be assessed, and interest at a rate of 1% per month may accrue on any unpaid contributions. It's essential to stay informed about the due dates and file on time to avoid these additional costs. If you find yourself unable to file on time, consider contacting the Utah Department of Workforce Services for guidance on how to proceed.

Omitting Employer Information: Many people forget to fill out their employer name and address. This information is crucial for processing the form accurately.

Incorrect Registration Numbers: Entering the wrong registration number or Federal Employer Identification Number (FEIN) can lead to delays and complications. Double-check these numbers before submitting.

Not Reporting Zero Wages: Some employers mistakenly think they don’t need to file if no wages were paid during the quarter. However, a report must still be submitted even if there are no wages.

Missing Employee Details: Failing to provide complete information for each employee, such as their full name or Social Security number, can result in issues with your report. Ensure all details are accurate and complete.

Ignoring Payment Details: It’s important to calculate and report the total payment due, including any interest or penalties. Neglecting this step can lead to unexpected charges later on.

The 33H form, also known as the DWS-UIC Utah Employer Quarterly Wage List and Contribution Report, is essential for employers in Utah to report wages and contributions for unemployment insurance. Along with this form, there are several other documents that employers may need to complete to ensure compliance with state regulations.

Understanding these forms can help ensure that employers remain compliant with unemployment insurance requirements in Utah. Keeping accurate records and timely submissions is crucial for avoiding penalties and maintaining good standing with the state.

The IRS Form 941 is a quarterly tax form that employers use to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. Like the 33H form, it requires information about the employer, including the name, address, and Employer Identification Number (EIN). Both forms are mandatory for employers to file, even if there are no wages to report during a specific quarter. They help ensure compliance with tax obligations and provide necessary data for state and federal agencies.

The W-2 form, or Wage and Tax Statement, is another document similar to the 33H form. Employers must complete this form for each employee at the end of the year to report wages paid and taxes withheld. While the 33H focuses on quarterly reporting, the W-2 summarizes annual earnings. Both documents serve as essential records for employees and tax authorities, helping to track earnings and tax contributions over time.

The 1099-MISC form is used to report payments made to independent contractors or other non-employees. While the 33H form covers employee wages, the 1099-MISC addresses payments outside of regular employment. Both forms require detailed reporting of amounts paid, but they differ in their focus on employment status. Each serves to ensure transparency and compliance with tax regulations.

The Form 940 is an annual report that employers file to report their Federal Unemployment Tax Act (FUTA) liability. Similar to the 33H, it is concerned with unemployment contributions, but it covers a different aspect of unemployment insurance. Both forms are essential for employers to fulfill their obligations regarding unemployment taxes, although the 940 is filed annually while the 33H is filed quarterly.

The Utah State Tax Commission’s Form TC-40 is used by individuals and businesses to report state income tax. While this form is not directly related to employment wages, it shares the requirement for accurate reporting of financial information. Like the 33H, it is crucial for compliance with state tax laws, ensuring that all entities contribute appropriately based on their earnings.

The I-9 form, or Employment Eligibility Verification, is used to verify an employee's identity and eligibility to work in the United States. While the 33H form focuses on reporting wages, the I-9 is concerned with the legal aspects of employment. Both forms are essential for employers to maintain compliance with employment laws, although they serve different purposes in the employment process.

The Labor Department's Form WH-347 is used for reporting wages paid to employees on government contracts. This form is similar to the 33H in that it requires detailed wage information, but it specifically targets contractors and subcontractors. Both forms help ensure that employers are meeting their financial reporting obligations, particularly concerning employee compensation.

The Form 5500 is an annual report required for employee benefit plans. While it focuses on the financial condition of such plans, it shares a common goal with the 33H form: ensuring transparency and compliance in employer reporting. Both forms are crucial for maintaining the integrity of employee benefits and tax reporting, though they apply to different aspects of employment and compensation.

When filling out the 33H form, it's essential to follow specific guidelines to ensure accuracy and compliance. Below is a list of dos and don'ts to help you complete the form effectively.

Understanding the 33H form is crucial for employers in Utah. However, several misconceptions can lead to confusion and potential issues. Here are six common misconceptions about the 33H form, along with clarifications:

Addressing these misconceptions promptly can help ensure compliance and avoid unnecessary penalties. Make sure to review the form carefully and seek assistance if needed.

Here are some key takeaways regarding the completion and use of the 33H form: